EUR/USD is trading quietly on Monday, as the pair starts the new trading week in the mid-1.37 range. In economic news, Eurozone Retail PMI came in at 47.7 points, indicating continuing contraction in the retail sector. We’ll get a look at the yield on Italian 10-year bonds later today. In the US, today’s sole event is Pending Home Sales. The markets are expecting a solid gain after a string of declines.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

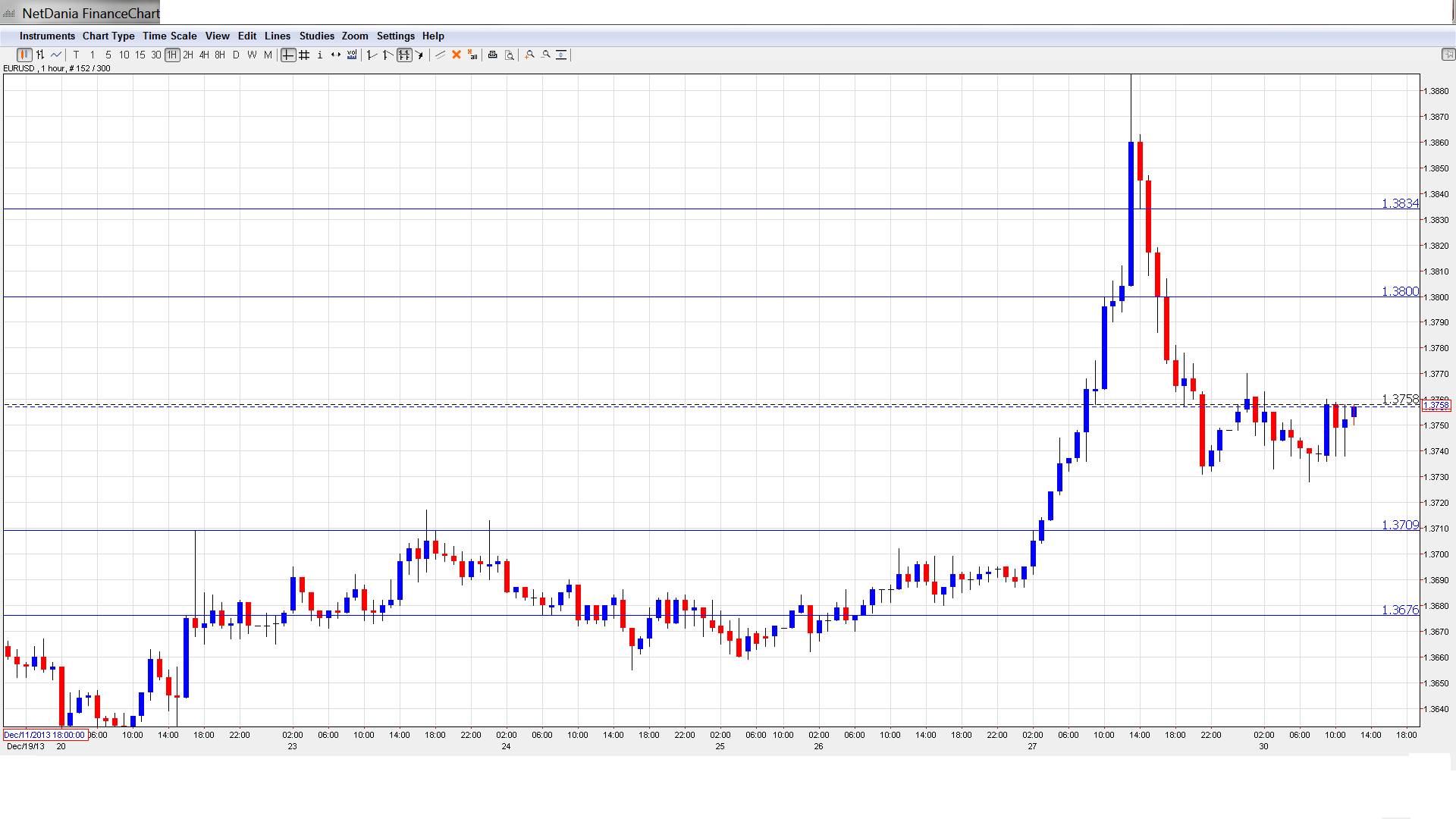

EUR/USD Technical

- EUR/USD lost ground in the Asian session, dropping to a low of 1.3727. The pair consolidated at 1.3758. In the European session the pair has edged lower.

- Current range: 1.3710 to 1.3800.

Further levels in both directions:

- Below: 1.3710, 1.3675, 1.3615, 1.3525, 1.3440, 1.34, 1.3320, 1.3240, 1.3175 and 1.31.

- Above: 1.3800, 1.3832, 1.3940 and 1.4036.

- 1.3800 is the next line of resistance. 1.3832 follows.

- On the downside, 1.3710 is providing support. 1.3675 is stronger.

EUR/USD Fundamentals

- 9:10 Eurozone Retail PMI. Actual 47.7 points.

- Tentative – Italian 10-year Bond Auction.

- 15:00 US Pending Home Sales. Exp. 1.1%.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Euro shows volatility: Low liquidity over a holiday period can lead to strong currency movements, and we got a taste of that on Friday. The euro shot up about 200 points as it hit a high of 1.3896. However, it then retracted and closed in the mid-1.37 range. With thin trade likely this week as well due to the holidays, we could see further volatility from EUR/USD.

- Unemployment Claims Shine: US Unemployment Claims bounced back nicely on Thursday, following two disappointing releases. The key employment indicator fell to 338 thousand, compared to 379 thousand in the previous release. The estimate stood at 346 thousand. With the Federal Reserve poised to begin its long-awaited QE taper next month, employment releases have taken on added significance. If the US labor market continues to improve, the Fed could decide on another taper as early as January, which would give a boost to the US dollar against its major rivals.

- US manufacturing, housing numbers point up: There was some holiday cheer from US releases last week as manufacturing and housing data pointed upwards. Core Durable Goods Orders posted a strong gain of 1.2%, its best showing since April. The key manufacturing indicator had posted four consecutive declines, so the sharp gain was welcome news. Durable Goods Orders bounced back from a sharp decline in October with a gain of 3.5%, well above the estimate of 1.7%. New Homes Sales also impressed with a five-month high, climbing to 464 thousand. The estimate stood at 449 thousand. We’ll get another look at housing data on Monday with the release Pending Home Sales, and the markets are expecting a strong reading from the key housing indicator.

- Ireland exits bailout program: With all the news about Eurozone bailouts for struggling countries, there was a happier episode as Ireland recently exited the bailout program it had received from the EU and the IMF. Ireland had been party to the bailout for three years, and will now be able to borrow money on the international markets. Key sectors such as tourism and agriculture are improving and unemployment is down to about 12.5%. However, economic growth is expected to be limited, as the country was forced to undergo drastic budget cuts and tax increases as part of the bailout. Finance Minister Michael Noonan has said the exit from the bailout is a step in the right direction, but admits that the road to recovery will be a long one.