EUR/USD continues to trade quietly, as the pair trades just above the 1.36 line early in Friday’s European session. In economic news, it was a busy Thursday in the US, with three key events. Unemployment Claims met expectations with another strong release, while the Philly Fed Manufacturing Index hit a three-month high. Core CPI looked weak, posted a gain of 0.1%. In the Eurozone, CPI and Core CPI met expectations. On Friday, the US releases more key data, with Building Permits, Preliminary UoM Consumer Sentiment and JOLT Job Openings wrapping up the week. In the Eurozone, today’s sole event, the French Government Budget Balance, showed little change.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

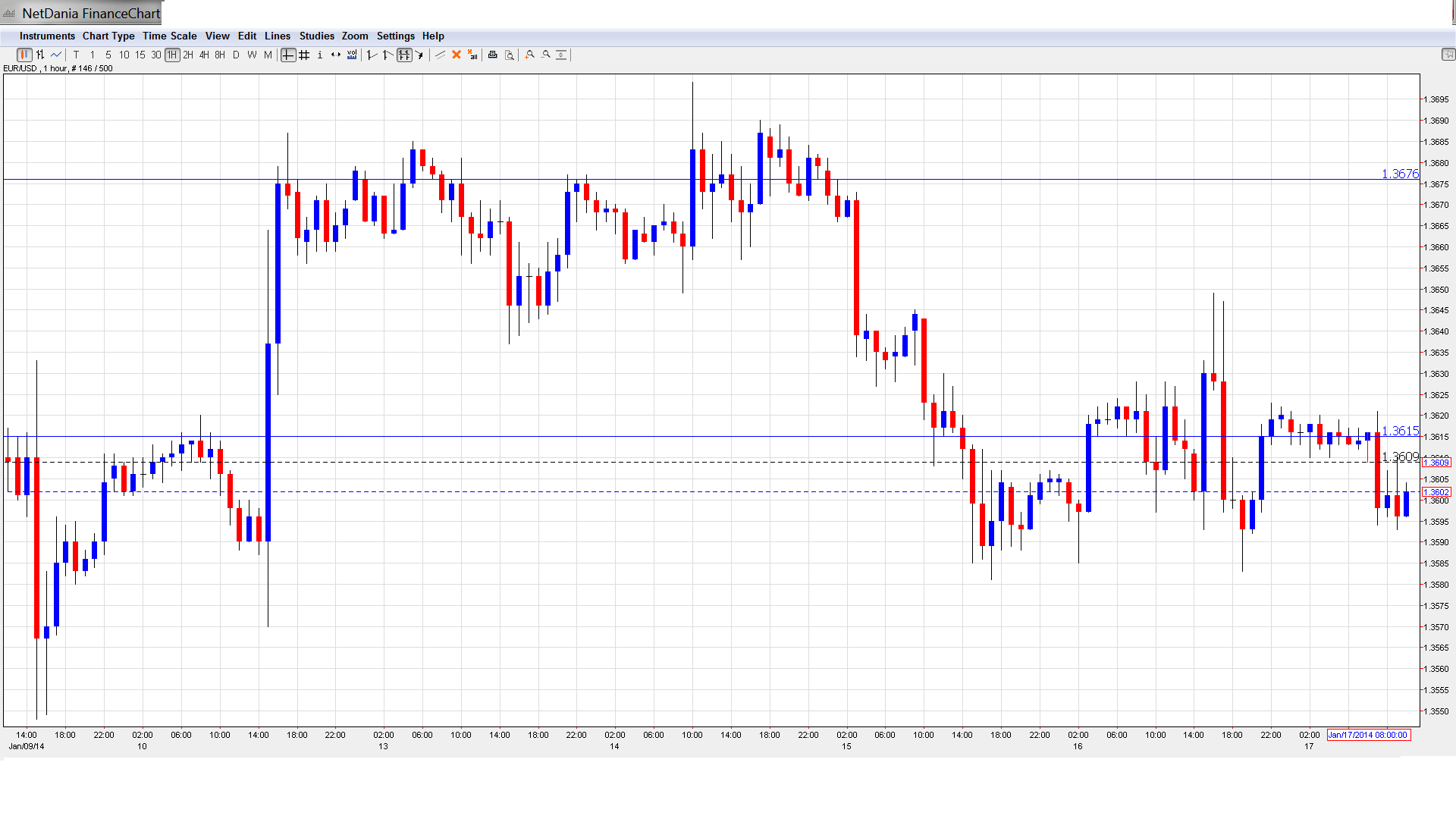

EUR/USD Technical

- EUR/USD traded slightly above the 1.36 line for most of the Asian session, consolidating at 1.3601. The pair has edged lower early in the European session.

Current range: 1.3550 to 1.3615.

Further levels in both directions:

- Below: 1.3550, 1.3450, 1.34, 1.3320, 1.3240 and 1.3175.

- Above: 1.3615, 1.3675, 1.3710, 1.3800, 1.3832, 1.3940 and 1.4036.

- 1.3615 has reverted to a resistance line. 1.3675 is stronger.

- 1.3550 is the first line of support. 1.3450 is next.

EUR/USD Fundamentals

- 7:45 French Government Budget Balance. Actual -87.0B.

- 13:30 US Building Permits. Exp. 1.01M.

- 13:30 US Housing Starts. Exp. 0.99M.

- 14:15 US Capacity Utilization Rate. Exp. 69.2%.

- 14:15 US Industrial Production. Exp. 0.4%.

- 14:55 US Preliminary UoM Consumer Sentiment. Exp. 83.4 points.

- 14:55 US Preliminary UoM Inflation Expectations.

- 15:00 US Jolts Openings. Exp. 3.97M.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Unemployment Claims remains solid: US Unemployment Claims looked sharp, dropping slightly to 327 thousand, very close to the estimate of 326 thousand. This was welcome news after last week’s shocking Non-Farm Payrolls. With the Fed finally starting its taper of QE, every employment release will be under the market microscope. Meanwhile, the Philly Fed Manufacturing Index continues to move higher. The indicator jumped to 9.4 points, up from 7.0 points a month earlier. This strong reading beat the estimate of 8.8 points.

- Low inflation levels continue: Weak inflation levels in the US remain a concern, as this is an indication of an underperforming economy. This was underscored by Core CPI, which posted a weak gain of just 0.1%. On Tuesday, the Producer Price Index posted a gain of 0.4%, reversing directions after three consecutive declines. Earlier this week, Chicago Fed President Charles Evans said that the low rate of U.S. inflation is “both puzzling and worrisome,” and enough reason to maintain low interest rates, even if the employment picture continues to brighten.

- US retail numbers in all directions: US retail sales numbers painted a mixed picture on Tuesday. Retail Sales dropped sharply to 0.2%, down from 0.7% in November. However, this figure matched the forecast. Core Retail Sales took the opposite route, jumping to 0.7%, compared to 0.4% the month before. This easily beat the estimate of 0.4%. Retail sales are an important gauge of consumer spending, and these numbers will have to improve if the recovery is to pick up speed.

- Another taper in January?: Last week’s dismal Non-Farm Payrolls report may have created some concern about the US employment picture, but it’s unlikely to change the Federal Reserve’s path of tapering QE, which it started just this month. In December, outgoing Fed chair Bernard Bernanke strong hinted that the Fed planned to wind up QE by the end of 2014, reducing the asset-purchase program by increments of $10 billion at each meeting. The Fed next meets for a policy meeting on January 28, and the question is will the Fed reduce QE by another $10 billion, down to $65 billion each month. Most analysts feel that one bad employment report will not affect the taper schedule and we will see another reduction in QE at the next meeting.