EUR/USD began the new week with a small recovery, pushing above the 1.35 line on Monday. We’re not seeing much movement from the pair in Tuesday’s European session, as the markets keep an eye on Wednesday’s PMI releases. In economic news, US ISM Manufacturing PMI slumped badly, dropping to a ten-month low. In the Eurozone, Italian and Eurozone inflation numbers were very weak. Spanish Unemployment Change had a dismal January, posting a huge jump in unemployment claims. It’s a quiet day in the US, with only two releases scheduled.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

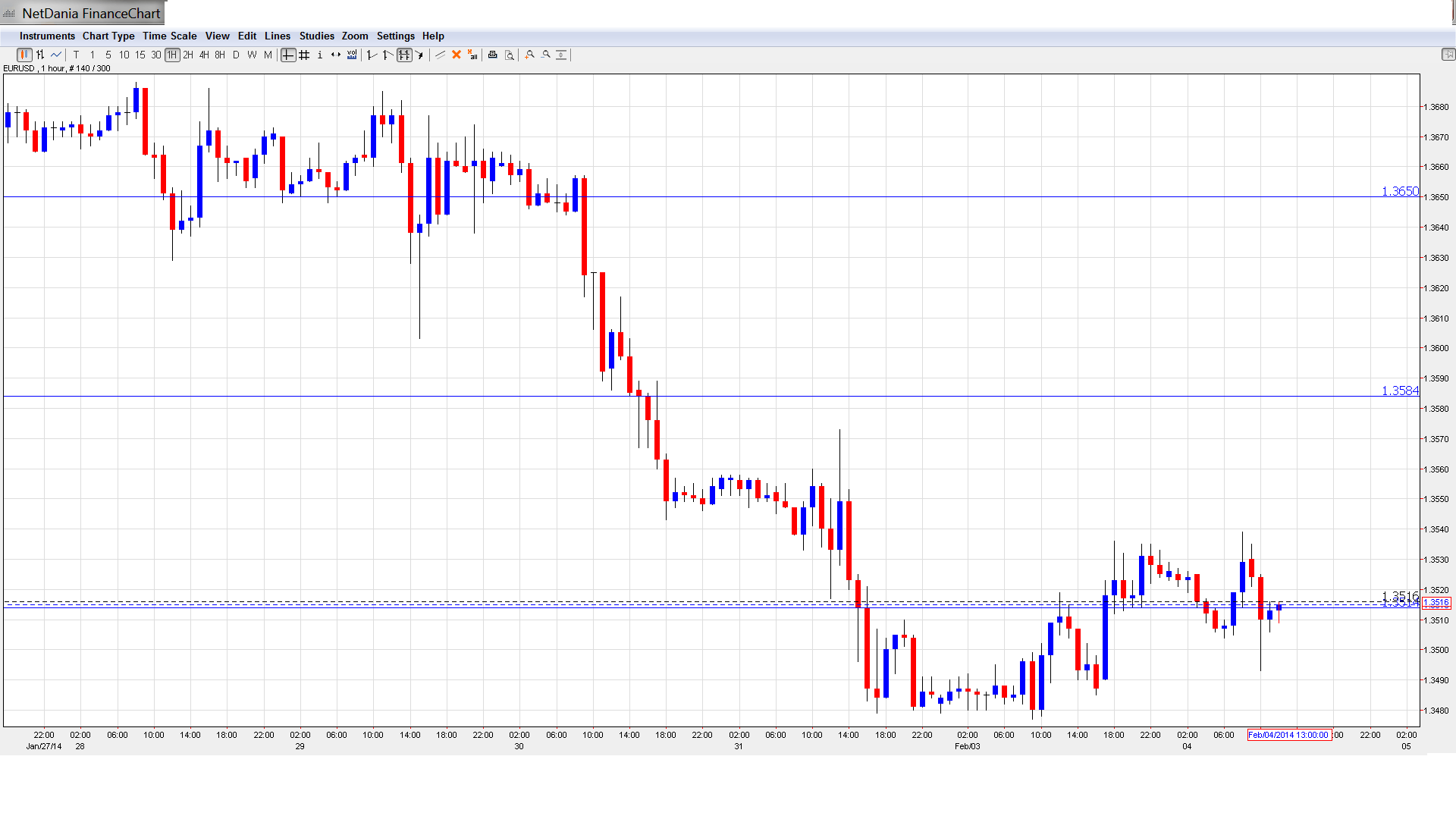

EUR/USD Technical

- EUR/USD showed some movement late in the Asian session, touching a high of 1.3539. The pair has edged lower in European trading and tested the 1.35 line early in the session.

Current range: 1.3450 to 1.3515

Further levels in both directions:

- Below: 1.3450, 1.34, 1.3320, 1.3240, 1.3175 and 1.31.

- Above: 1.3515, 1.3580, 1.3650, 1.37 and 1.3800.

- On the upside, 1.3515 is under pressure. 1.3580 is stronger.

- 1.3450 is important support. The round number of 1.34 follows.

EUR/USD Fundamentals

- 8:00 Spanish Unemployment Change. Exp. -21.3K, Actual 113.1K.

- 10:00 Italian Preliminary CPI. Exp. 0.3%.

- 10:00 Eurozone PPI. Exp. 0.3%.

- 15:00 US Factory Orders. Exp. -1.9%.

- 15:00 US IBD/TIPP Economic Optimism. Exp. 46.1 points.

*All times are GMT For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Spanish employment data falters: Spanish Unemployment Change jumped to 113 thousand, shocking the markets which had expected a decrease. The Spanish employment minister tried to put a positive spin on the data, noting that January typically jumps higher, and this figure was the lowest January increase since 2007. Recent Spanish data has looked strong, but clearly the staggering unemployment levels will continue to weigh on the economy.

- Will the ECB react to lower inflation?: Eurozone inflation indicators continue to point to low levels of inflation, with the headline figure at the lows of October: 0.7%. Core inflation is at 0.8%, well below the ECB target of 2.0% but still higher than the lowest level of 0.7% seen in December. Nevertheless, the euro is weaker on expectations for a move from the ECB. Will the central bank act now or hold the course? ECB Preview: 5 scenarios – negative deposit rate now, or later?.

- US GDP rises, but with a caveat: US GDP growth came out at 3.2% in Q4, as expected. This was a nice gain from the Q3 reading of 2.6%. However, the big contribution of inventory buildup is not a good sign: inventories could be depleted later on. This week we have top tier events building up towards the Non-Farm Payrolls on Friday.

- Yellen takes over the Fed: In his last decision as Fed Chairman, Bernanke cut its stimulus program by another $10 billion, lowering QE to $65 billion each month. The Fed still plans to wind up QE by the end of the year, so we can expect further tapers, barring any surprise downturns in the US economy. Janet Yellen is the new head of the Federal Reserve, and she is likely to continue the same policy.

- Emerging markets hit by taper: The taper, as well as issues in local economies, is taking its toll on the emerging markets such as Brazil, India, China, Turkey, South Africa and Indonesia. The efforts to strengthen the local currencies has had limited success, and some estimate that the outflow of money from these nations has only just begun. Flows out of these countries and into Europe could keep the euro bid. In the meantime, the situation seems to be contained, but this may not last for too long.

- German releases point to growth: The German locomotive continues to pick up speed, much to the delight of the markets. Unemployment Change sparkled in December with a drop of 28 thousand, crushing the estimate of a drop of 5 thousand. This was the indicator’s best showing since March 2011. The Unemployment Rate stayed pegged at 6.8%. Consumer Climate and Ifo Business Climate both rose, indicating that German businesses and consumers are optimistic about the economy as we begin 2014. Germany is the Eurozone’s largest economy, and the region will need Germany to lead the way to an economic recovery. However, not all is rosy, especially with the big fall in retail sales.

More: Bidding up the dollar