The euro has resumed its losing ways, as EUR/USD has fallen below the 1.37 level in Thursday’s European session. The euro has coughed up over 350 points since climbing within a whisker of 1.40 late last week. In Thursday action, German Preliminary GDP looked sharp, posting its highest gain in a year. However, Eurozone Flash GDP dipped in Q1. On the inflation front, Eurozone Core CPI improved in April and matched the forecast. In the US, there are a host of events on the schedule, highlighted by three key releases – Core CPI, Unemployment Claims and the Philly Fed Manufacturing Index. Also, Federal Reserve chair Janet Yellen will speak at an event in Washington.

- EUR/USD was very quiet in the Asian session, as it has been for most of the week, trading around 1.3720. The euro has weakened in the European session and dropped below 1.37, its lowest level since late February.

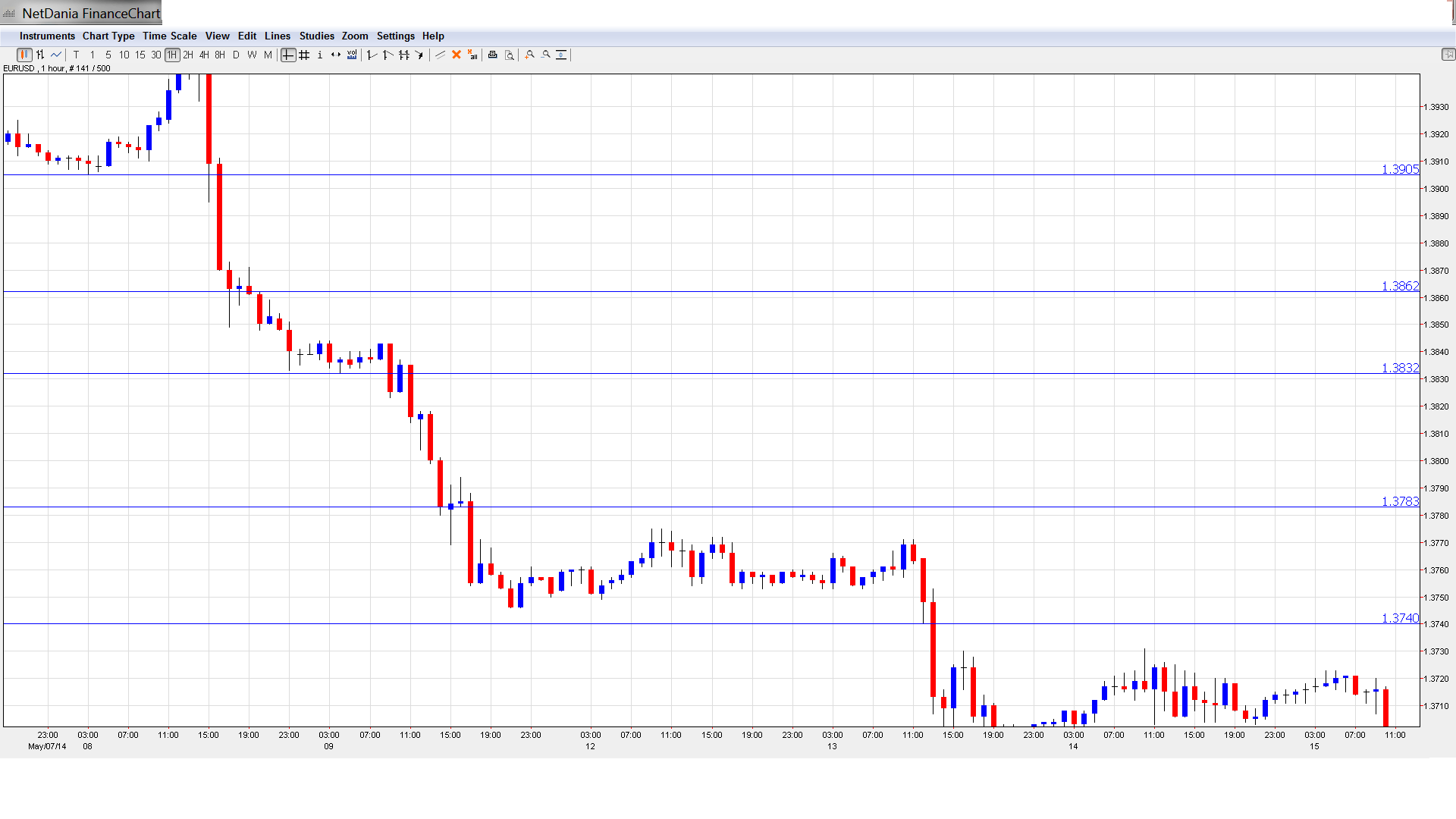

Current range: 1.37 to 1.3740.

Further levels in both directions:

- Below: 1.3650, 1.3560, 1.3515 and 1.3450

- Above: 1.37, 1.3740, 1.3785, 1.3830, 1.3865, 1.3905, 1.3964, 1.40, 1.4055 and 1.4105

- On the downside, 1.3650 is under strong pressure. 1.3560 is a strong support level.

- 1.37 has switched to a resistance role. 1.3750 follows.

EUR/USD Fundamentals

- 5:30 French Preliminary GDP. Exp. 0.4%. Actual 0.0%.

- 6:00 German Preliminary GDP. Exp. 0.7%. Actual 0.8%.

- 8:00 ECB Monthly Bulletin.

- 8:00 Italian Preliminary GDP. Exp. 0.2%. Actual -0.1%.

- 9:00 Eurozone CPI. Exp. 0.7%.

- 9:00 Eurozone Core CPI. Exp. 1.0%.

- 9:00 Eurozone Flash GDP. Exp. 0.4%.

- 12:30 US Core CPI. Exp. 0.1%.

- 12:30 US Unemployment Claims. Exp. 321K.

- 12:30 US CPI. Exp. 0.3%.

- 12:30 US Empire State Manufacturing Index. Exp. 5.5 points.

- 13:00 US TIC Long-Term Purchases. Exp. 32.3B.

- 13:15 US Capacity Utilization Rate. Exp. 79.2%.

- 13:15 US Industrial Production. Exp. 0.4%.

- 14:00 US Philly Fed Manufacturing Index. Exp. 13.9 points. See how to trade this event with USD/JPY.

- 14:00 US Mortgage Delinquencies.

- 14:00 US NAHB Housing Market Index. Exp. 49 points.

- 14:30 US Natural Gas Storage. Exp. 99B.

- 23:00 Federal Reserve Chair Janet Yellen Speaks.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Draghi says ECB poised to act: At last week’s policy meeting, Mario Draghi, the ECB said it would be comfortable taking monetary action in June, the markets jumped, and the euro has been in a tailspin ever since. However, Draghi gave himself plenty of wiggle room, saying the ECB would take into account growth and inflation forecasts before making any moves. Eurozone Core CPI improved to 1.0% in April, up from 0.7% a month earlier. Eurozone CPI followed suit, as it improved to 0.7%, up from 05%. With both inflation indicators matching their estimates and pointing upwards, the ECB has some breathing room before having to take action. If upcoming inflation numbers meet expectations, we could see the ECB play it safe in June and remain on the sidelines yet again.

- US inflation numbers concern: Low inflation levels are not limited to the Eurozone. Weak inflation has been a persistent problem in the US, and Fed chair Yellen highlighted this issue when speaking before Congress last week. There was good news on Wednesday as PPI, a key inflation indicator, edged higher in April, coming in at 0.6%. This easily beat the estimate of 0.2%. Core PPI also beat the estimate, posting a gain of 0.5%.

- Eurozone GDP numbers disappoint: GDP is the primary gauge of economic activity, and the April numbers pointed to trouble for the Eurozone. Eurozone Flash GDP dipped to 0.2% in Q1, short of the estimate of 0.3%. French and Italian GDP releases also disappointed, as both weakened in April and missed expectations. On a bright note, German Preliminary GDP jumped 0.8% in Q1, its best showing since Q1 in 2013. This edged above the estimate of 0.7%. GDP data is doubly important now that ECB head Mario Draghi has said that the Bank could take action in June, depending on inflation and growth forecasts.

- US retail sales weaken: Retail Sales and Core Retail Sales are key gauges of consumer spending, and are carefully tracked by the markets. Both indicators were weak in April. Core Retail Sales dropped to 0.0%, well off the estimate of 0.6%. Retail Sales followed suit, with a paltry gain of just 0.1%, compared to an estimate of 0.5%.