We’re not sure whether to chalk it up to a loss on the football pitch or disappointing economic fundamentals, but US markets are positioned for a lower open this morning. Investors are in a subdued mood after yesterday’s surprisingly weak consumer spending numbers, but are also concerned at the prospect of an earlier-than-expected rate hike from the Federal Reserve.

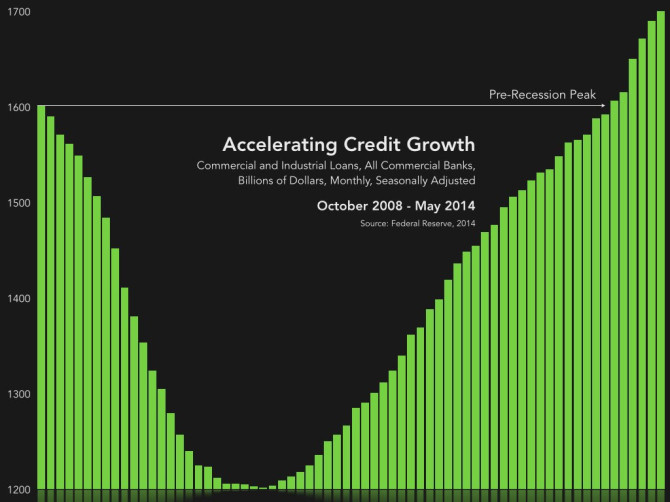

Many observers are cutting second-quarter growth forecasts in reaction to the Commerce Department results, which showed spending rising more slowly than inflation – but we suspect this to be a short-lived phenomena. As illustrated in the chart enclosed below, loan volumes have now surpassed pre-crisis levels, and apיש ×pear to be accelerating. Durable goods purchases are growing, and jobless claims are dropping.

Of course, that doesn’t mean that investors can have their cake and eat it too. Asian and European markets moved down overnight after St. Louis Fed President James Bullard said that interest rates could rise much sooner than markets currently expect. Coming on the heels of a slew of hawkish comments from officials over the last week, markets took his threat seriously and bid the dollar up through the trading session.

The pound is still basking in the afterglow of yesterday’s announcement from Bank of England Governor Mark Carney. The Canadian transplant unveiled a raft of measures aimed at limiting the flow of borrowed cash into the country’s overheated housing market – but stopped short of the draconian measures that had been mooted previously.

Euros are trading sideways, with investors shifting assets into safe havens like German bunds, while equities slip slightly.

The loonie is flying at a rarefied altitude trading near a six month high as the North American session begins. The currency is benefitting from something akin to a perfect storm in the financial markets, with accommodative global monetary conditions, rising asset prices, accelerating growth, and geopolitical turmoil combining to drive portfolio flows into the oil market and toward Canadian assets.

These flows have still not found an echo in trade balances however, where crude oil’s relatively small contribution to net exports has yet to fully offset the losses suffered in manufacturing and other industries. Unit labor costs in Canada remain at historical highs relative to the United States, while outbound consumer spending continues to outpace shipments to other countries. Simply put, there are few long-term fundamentals to justify the case for currency appreciation.

As such, we see today’s valuations as stretched. In the event that the conflict in the Middle East subsides into a stalemate, or major central banks begin to pull stimulus back, it is likely that the currency will lose momentum once again.

The episode does serve as a good reminder though – while debt and equity markets tend to be more volatile during times of panic, the currency markets are not wired in the same way. Some of the largest volatility spikes in history have been associated with rapid bursts of optimism.

Could we see the same again? Absolutely. A ‘melt-up’ is one of the most significant tail risks that hedgers need to think about in the months to come – so watch your tails, and have a great weekend!

US Credit Growth: