- Bitcoin’s daily confluence detector lacks substantial resistance upfront.

- The MACD shows increasing bullish momentum.

Over the last six days, Bitcoin bulls have been in full control of the market as the price rose from $11,340 to $12,835. This Wednesday, the premier cryptocurrency had the largest single-day gain since July 27. The MACD shows increasing bullish momentum, so further price growth is anticipated.

BTC/USD daily chart

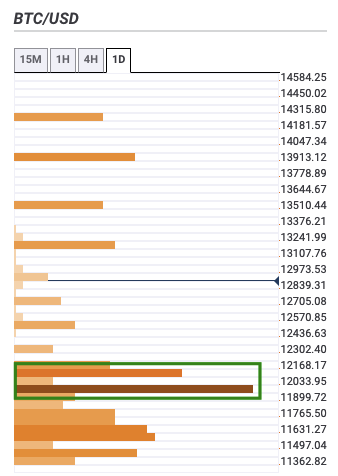

The confluence detector is a handy little tool that helps us visualize strong resistance and support levels. As per the daily confluence detector, there is a lack of strong resistance levels on the upside. This should be encouraging news for the buyers as they aim to take BTC into the $13,000-zone.

BTC daily confluence detector

The Flipside: Can the bears spoil the party?

Even if the bears take control, their downside is limited by the strong support zone between $12,000-$12,100. Even if they manage to break below this stretch, there is another robust support at $11,000, which benefits from both the 50-day and 100-day SMAs. Adding further credence to this bearish outlook is the way the whales have been behaving.

BTC holders distribution

%20%5B05.47.07,%2022%20Oct,%202020%5D-637389253955871217.png)

Santiment’s holders distribution graph shows you the number of addresses belonging to a particular token bracket. As per the chart, the number of addresses holding 10,000-100,000 tokens fell from 111 on October 8 to 104 on October 20. This is a heavily bearish sign as it shows that the whales are selling off their holdings.

Key price levels to watch

Bitcoin buyers have the freedom to take the price into the $13,000 and even the $14,000 obstacle. The daily confluence detector shows a complete lack of strong resistance barriers upfront.

For the bears, the downside is capped off at the $12,000-$12,100 support wall. A break below that zone will take the price down to $11,000, which has both the 50-day and 100-day SMAs.