EUR/USD started the year with a drop while USD/PY played around familiar ranges. Wha’s next? Here is the view from SocGen:

Here is their view, courtesy of eFXnews:

Look forwards. The yen’s nearly fallen too far/too fast to sell, the dollar’s getting closer to its peak and the Euro is cheap but unbuyable before the French elections.

My favorite currencies are Scandinavian, and after an stellar 2016, long SEK/KRW is a trade we’ve been pushing for a week or two. A more mundane G10 version is short EUR/SEK. A second trade is to be short NZD/NOK. Long current account surplus, short deficit. Finally, with all this positive growth, oil isn’t done yet. Short GBP/CAD for a final flurry.

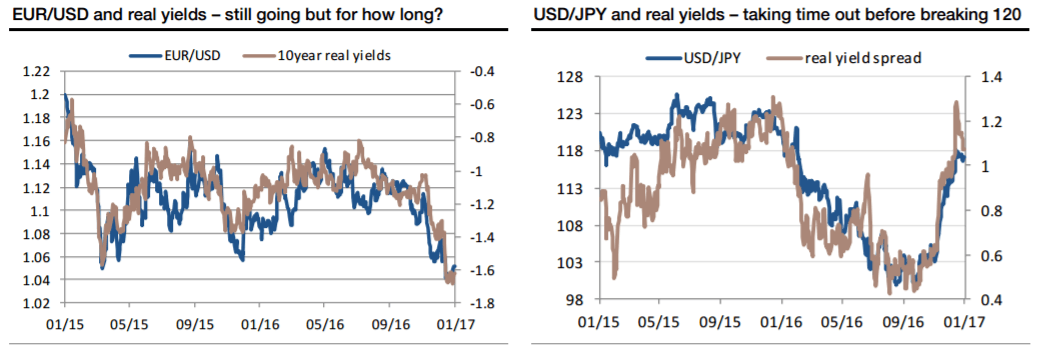

There is no Eurodollar recommendation on the list, though we do expect to see parity before the French presidential elections. In nominal terms, the Treasury/Bund yields spread, at around 225bp, is wider than any point since April 1989, the time of the Hillsborough disaster and just over six months before the Berlin Wall came down. More recently, we’ve seen a 100bp widening in the real yield differential between Germany and the US since the start of 2015, which has taken EUR/USD down by 15 figures. Another 30bp real yield widening isn’t impossible but this morning’s release of the strongest Eurozone manufacturing PMI since 2011 is surely a reminder that a softer currency and stronger US data aren’t compatible with never-ending doom pessimism about the European economic outlook. Getting EUR/USD down is like pushing Sisyphus’ rock uphill.

USD/JPY doesn’t look like an exciting buy on real yield differentials now, but they should be supportive again going forwards. Tread carefully, yen bears!

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.