EUR/USD has been relatively stable after the initial Brexit shock. What’s next for the common currency? The team at Morgan Stanley describe the next steps for the currency:

Here is their view, courtesy of eFXnews:

The Case For Higher EUR:

We believe that the EUR can remain well supported even in times of political uncertainty.

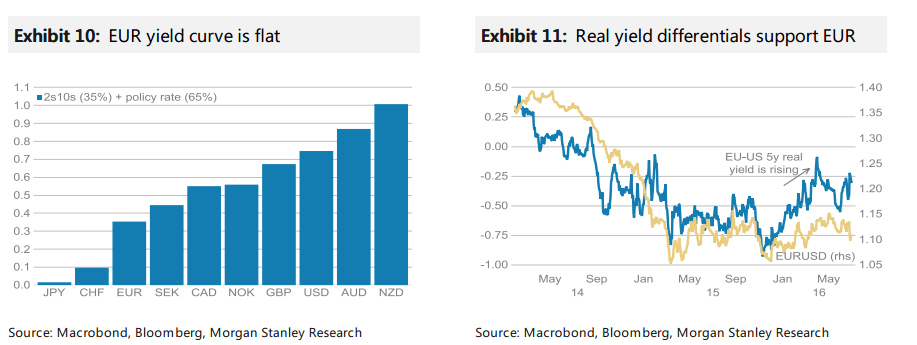

The dynamics for the EUR have changed now that Bund yields are trading below zero, limiting the ability of nominal yields to fall aggressively in response to growth worries. At the same time inflation expectations have fallen, putting upward pressure on real yields, supporting the currency.

EMU based investors are finding few investment returns outside of EMU, limiting the outflows needed to counterbalance EUR inflows from the current account surplus. Banks are reducing foreign lending as they have to keep balance sheets constrained.

We don’t see who would be a EUR seller given that corporate EUR long positioning is relatively low, despite the rising current account surplus.

We are positioned via long EURGBP* and would look to add further EUR longs in coming months. Market expectations for deeper rate cuts by the ECB or serious market concerns about a breakup of the currency union would make us bearish on the EUR again.

What would make the EUR fall?

The ECB’s interest rate policy has a larger impact on the currency than its QE programme. It was the expectation of future rate cuts into negative territory that pushed EURUSD from 1.40 to 1.05. The market has already priced another 10bp cut by year end, suggesting that the ECB would need to go even deeper into negative territory for the EUR to weaken and of course this is a risk to our currency view.

Expectations for expansion of the QE programme, which is a probable next step for the ECB, are now unable to weaken the EUR as the movement towards corporate bond purchases is not effective at bringing down long term government bond yields, which the currency responds to most. Pushing the first ECB hike further out had little effect on the EUR over the past year. The second reason for EUR weakness would be the market expecting a breakup of the currency union. There are upcoming political risk events for the region but for now we don’t expect an escalation of these risks.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.