EUR/USD continues to lose ground, as markets jitters increase over a likely strike by the US against Syria. The pair crashed through the 1.33 line early on Thursday, and is trading in the mid-1.32 range in the European session. Looking at economic releases, Thursday will be busy. German Unemployment Change was surprisingly weak, posting a three-month high. German Preliminary CPI will be released later in the day. Over in the US, there are two market-movers being released – Preliminary GDP and Unemployment Claims.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

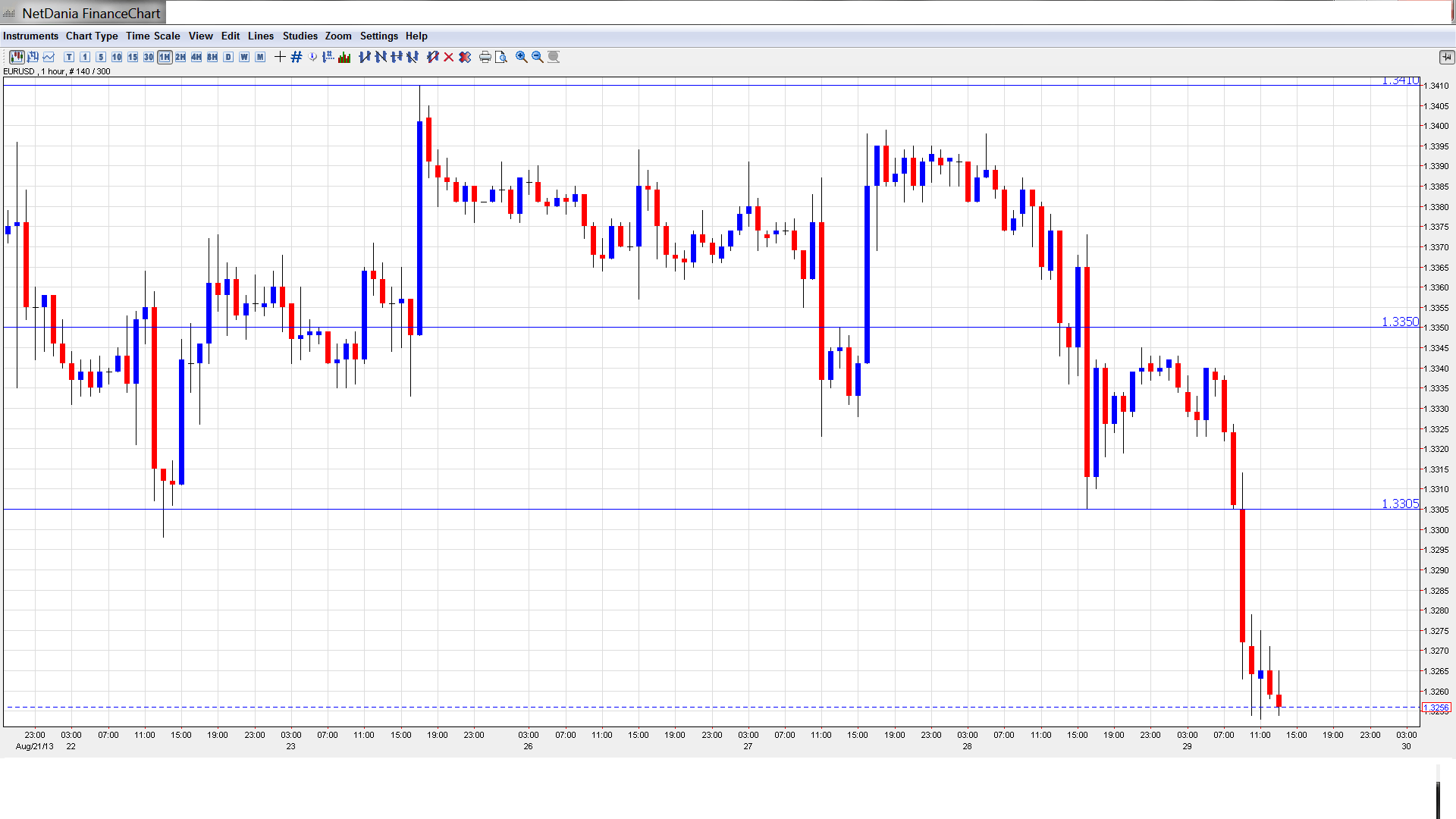

EUR/USD Technical

- In the Asian session, EUR/USD dropped sharply, falling below the 1.33 line and touching a low of of 1.3284. The pair consolidated at 1.3288. EUR/USD continues to lose ground in the European session.

Current range: 1.3240 to 1.33.

Further levels in both directions:

- Below: 1.3240, 1.3175, 1.31, 1.3050, 1.30 and 1.2940.

- Above: 1.33, 1.3350, 1.3415, 1.3450, 1.3520, 1.3590 and 1.37.

- 1.3240 is providing weak support and could be tested as the euro continues to weaken. 1.3175 is next.

- 1.3300 has reverted to a resistance line. 1.3350 follows.

EUR/USD Fundamentals

- All Day: German Preliminary CPI. Exp. 0.2%.

- 7:55 German Unemployment Change. Exp. 7K, actual -5K.

- 8:10 Eurozone Retail PMI. Exp. 50.3 points.

- Tentative: Italian 10-year Bond Auction.

- 12:30 US Preliminary GDP. Exp. 2.2%.

- 12:30 US Unemployment Claims. Exp. 330K.

- 12:30 US Preliminary GDP Price Index. Exp. 0.7%.

- 12:50 US FOMC Member James Bullard Speaks.

- 14:30 US Natural Gas Storage. Exp. 65B.

- 16:00 German Buba President Jens Weidmann Speaks.

- 23:45 US FOMC Member James Bullard Speaks.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Euro slides as Mid-East tensions rise: The markets are reacting nervously over a likely US strike against Syria, after a chemical attack in the war-torn country killed hundreds of civilians. There are fears that a US attack could elicit a response from Syria or even Iran, so we could continue to see volatility in the markets. There is a report that the US could strike on the weekend, which would reduce market instability. Meanwhile, the euro has taken a hit and has lost close to a cent since early Wednesday, as nervous investors move over to the safe-haven US dollar.

- US housing data falters, but dollar stays strong: US releases continue to zigzag this week, as Pending Home Sales looked weak. The key housing indicator posted its second straight decline, dropping 1.3% in August. This was well short of the market estimate of 0.2%. US manufacturing releases started off the week with sharp declines, although consumer confidence looked good. The dollar has remained strong despite the mixed data, thanks to the crisis over Syria and market speculation over QE tapering.

- Mixed numbers out of Germany: German data continues to be a mixed bag. On Thursday, Unemployment Change jumped from -7 thousand in July to 7 thousand in August. The markets had expected another decline of -5K. German Ifo Business Climate started the week on a positive note, posting its fourth consecutive gain and climbing to its highest level in over a year. However, GfK German Consumer Climate could not keep up, as it dropped slightly from 7.0 to 6.9 points, missing the estimate of 7.1 points. Last month’s reading of 7.0 was a multi-year high, so the slight drop is unlikely to be of great concern to the markets. German consumers continue to spend, but are worried about inflation. National elections are just a few weeks away, and the economy promises to be the central issue of the campaign as Chancellor Angela Merkel seeks a third straight term in office.

- Fed split over QE tapering timing: The Federal Reserve has kept mum about when it might taper QE, but the recent Jackson Hole summit provided a glimpse of the divisions in the Fed as to when it might act. Fed chair Bernard Bernanke was a no-show at the summit, giving other policymakers an opportunity to express their views on QE. Dennis Lockhart, head of the Atlanta Fed, said that tapering could start in September, but only if US data justified such a move. There was a more hawkish statement from James Bullard, head of the St. Louis Fed. Bullard said that there was no need for the Fed to rush into QE tapering. Bullard will make two appearances on Thursday, so we could see some reaction from the markets to his remarks. Meanwhile, the uncertainty over QE tapering has boosted the US dollar, raised the yields on US treasury bonds and led nervous investors to pull billions of dollars out of emerging markets. With September just around the corner, we could see strong volatility in the markets as speculation over QE heats up.

- Greece wants more aid, but no strings attached, please: Greece has already received two bailouts from the troika, amounting to some 240 billion euros. Despite this massive infusion of funds, the country’s economy is still in difficult straits, and there is talk of a third bailout. On Sunday, Greek finance minister Yannis Stournaras said that Greece was looking for another 11 billion euros in aid, but would not adopt any austerity measures in return. German Finance Minister Wolfgang Schaeuble said that the estimate of 11 billion euros was “not completely unrealistic”. However, the German government is unlikely to rubber-stamp the request, given that elections in Germany are only a few weeks away, and bailout packages to struggling European countries will not win the government any votes.