EUR/USD rocked and rolled on Draghi’s press conference in a turbulent week and ended it lower. The last week of April features another key German survey as well preliminary inflation figures. Here is an outlook for the highlights of this week and an updated technical analysis for EUR/USD.

Draghi tried not to rock the boat by leaving the door open for more but also showing satisfaction and asking for patience. With absolutely no discussion about helicopter money, EUR/USD returned not normal. The pair did make attempts to move higher but paused. The ZEW economic sentiment came out better than expected, with the improvement in China cited as the main reason for the better business sentiment. In the US, there are somewhat higher expectations for rate hikes this year and this gave some much needed support for the dollar.

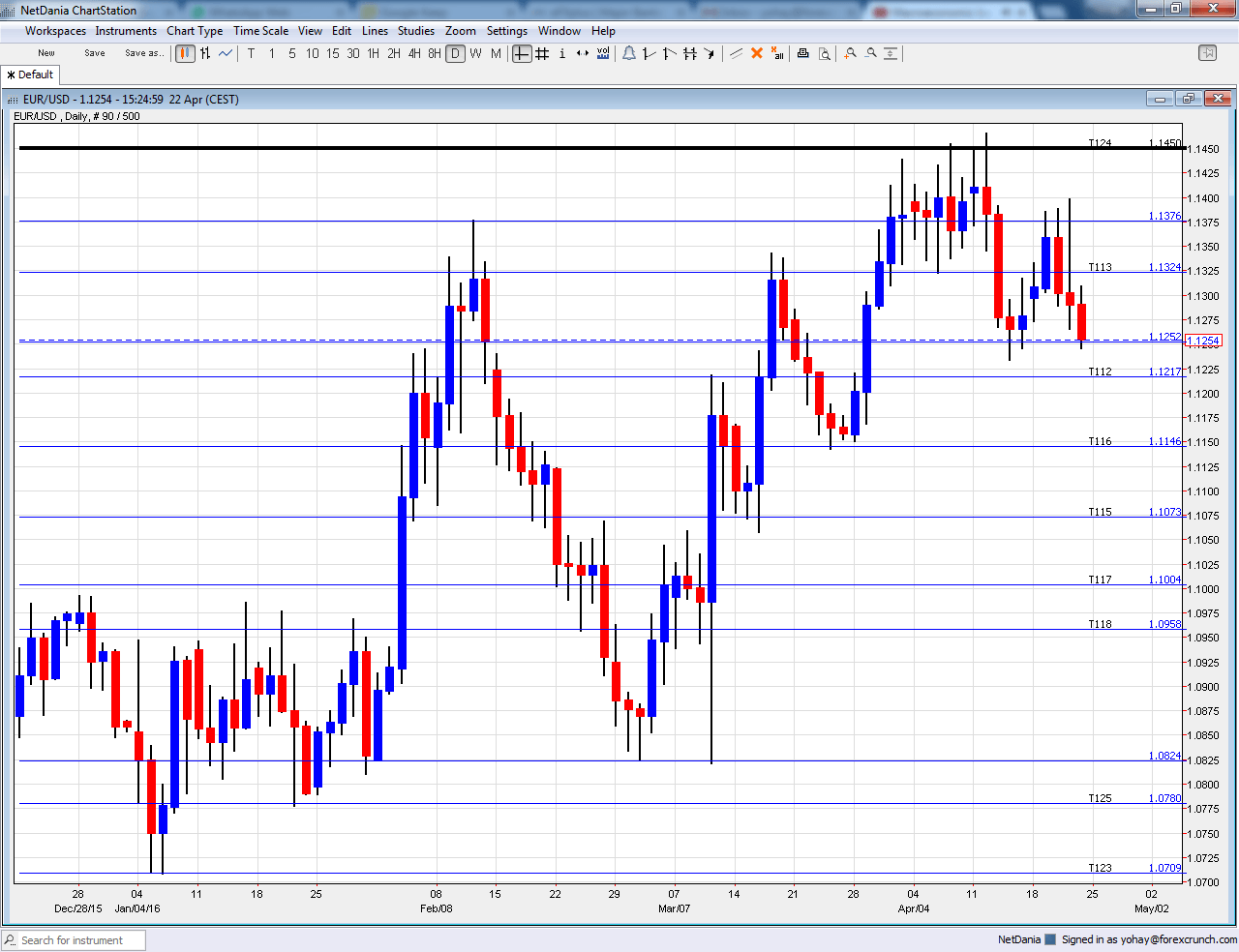

[do action=”autoupdate” tag=”EURUSDUpdate”/]EUR/USD daily graph with support and resistance lines on it. Click to enlarge:

- German Ifo Business Climate: Monday, 8:00. IFO is Germany’s No. 1 Think Tank and the publication has a significant impact even though the ZEW figure is already out. A score of 106.7 points was seen in March and a similar one could come out now: 107.1 is predicted.

- Belgian NBB Business Climate: Monday, 13:00. Despite coming from a small country, this is a good barometer for the whole continent. The improvement to -4.2 points still leaves this 6000 strong survey at pessimistic territory. We now get the data for April which is expected to stand at -4 points.

- German Import Prices: Tuesday, 6:00. Prices of imported goods have fallen below predictions for long months, with a drop of 0.6% seen in March. Another fall cannot be ruled out but +0.3% is expected.

- German GfK Consumer Climate: Wednesday, 6:00. This survey of 2000 consumers slid back to 9.4 points from 9,5 seen beforehand. All in all, German consumers are relatively confident and a tick back up to 9.5 is expected.

- Monetary data: Wednesday, 8:00. The European Central Bank’s efforts to get money going have had some success with the M3 Money Supply accelerating to a pace of 5% y/y. Also Private Loans are out of the woods of a negative spiral seen not that long ago, and they are now on the rise, with 1.6% y/y seen in February. Similar figures are on the cards for March. 5% in M3 Money Supply and private loans are expected to accelerate to 1.7%.

- German CPI: Thursday: state data during the morning with the all-German number at 12:00. After disappointing in February, Germany’s inflation data beat in March with +0.8% m/m, indicating some improvement. The German figure has the lion’s share in shaping the all-European number. A drop of 0.2% is predicted.

- Spanish CPI: Thursday, 7:00. The fourth largest economy is suffering from both high unemployment and a drop in prices. In the past four months, the data disappointed on the inflation front. A drop of 0.8% y/y was seen in March. The number is expected to remain negative with a drop of 0.7% y/y.

- Spanish unemployment rate: Thursday, 7:00. The unemployment rate fell at a faster clip than expected in the past 3 quarters, but it is still hovering above 20%. No change from Q4’s 20.9% is expected as the economy lost some momentum.

- German unemployment change: Thursday, 7:55. The German labor market seems quite robust, with drops in the numbers of the unemployed in recent months. The flat read seen in February was a disappointment and the release for March will tell us if it was a one-off or not. Expectations are for +1K.

- French GDP: Friday, 5:30. The French economy saw two consecutive quarters of 0.3% growth according to the latest figures. A slightly slower growth rate is on the cards in the preliminary release for Q1 2016 which is expected to show an acceleration with +0.4% q/q.

- German retail sales: Friday, 6:00. Consumer have been relatively cautious in Germany in the past two months, with the volume of sales dropping. After a slide of 0.4% in February, a bounce could be seen now. German spending is certainly needed for the euro-zone economy, whether private or public. +0.3% is expected.

- French CPI: Friday, 6:45. Prices advanced 0.7% in the continent’s second largest economy during February. This also feeds into the all-European number. +0.1% is expected m/m.

- Spanish GDP: Friday, 7:00. While employment and inflation are poor, GDP growth has been robust in Spain. A solid quarterly growth rate of 0.8% was seen in Q4, closing the year with a bang. Slower growth is on the cards now, partially a result of the political stalemate.

- CPI: Friday, 9:00. While data from key countries is already out, the preliminary inflation read certainly moves markets. According to the final data, prices were flat year over year in March. Will they cheer the ECB with a return to positive territory? Expectations are for -0.1%. Core CPI stood on 1% and it is expected to drop to +0.9%. Expectations are certainly low.

- Unemployment rate: Friday, 9:00. The unemployment rate in the euro-zone had a winning streak of positive surprises, falling to 10.3%. However, it stalled last month at this level. No change is expected.

* All times are GMT

EUR/USD Technical Analysis

Euro/dollar remained with the ranges described last week.

Technical lines from top to bottom:

1.1712 was the high point in August 2015 and remains high in the sky. It is followed by the very round level of 1.15.

1.1460 was a key resistance line in 2015 and 1000 above the multi-year lows. 1.1410 is weak resistance on the way up after working as such in the Spring of 2016.

1.1335 separated ranges in April 2016 and now works as resistance. It is followed by the swing low of 1.1220 in September which is minor resistance now.

1.1140 cushioned the pair in October. 1.1070 served as a clear separator of ranges during February and also beforehand.

1.10 is a round number and significant resistance. 1.0960, which worked in the past as resistance, provided a cushion for the pair in February. 1.0825 worked as support in early March 2015 and should also be watched. This is now a triple bottom.

The post-Draghi low 1.0780 replaces 1.08 as support. 1.0710 is the next support line on the chart after temporarily capping the pair in April 2015.

I remain bearish on EUR/USD

Even if the ECB is not adding any new stimulus immediately, Draghi reiterated his commitment to push inflation higher and stands firm on the ECB’s independence. And even if the Fed is no rush either, the US dollar gets more love than beforehand and we could see the pair slip a bit lower.

In our latest podcast we ask: is China out of the woods?