EUR/USD has posted modest losses on Wednesday, as the pair trades in the low-1.37 range in the European session. In economic news, Eurozone Retail Sales posted a sharp gain and easily beat expectations. Spanish and Eurozone PMI Services beat the estimates, but the Italian numbers weakened. In the US, we’ll get a look at key employment data, with the release of ADP Non-Farm Employment Change. The markets are bracing for a weak reading. Today’s other major event out of the US is ISM Non-Manufacturing PMI.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

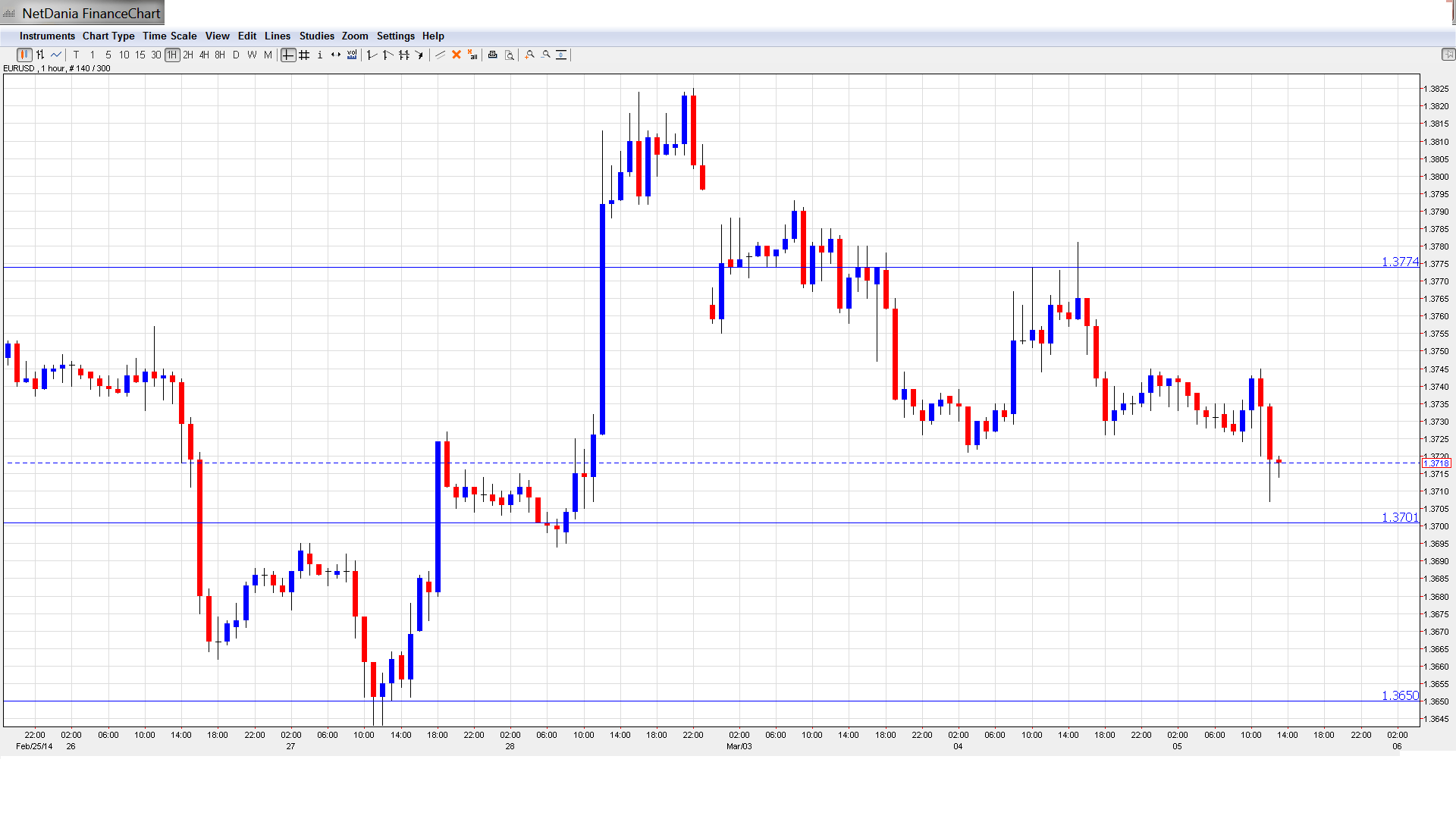

EUR/USD Technical

- EUR/USD edged lower in the Asian session, closing at 1.3742. The pair continues to lose ground in the European session and is putting pressure on the 1.37 level.

Current range: 1.37 to 1.3773.

Further levels in both directions:

- Below: 1.37, 1.3650, 1.3580, 1.3515, 1.3450 and 1.34

- Above: 1.3773, 1.3830, 1.3895, 13915, 1.40 and 1.4214.

- 1.3773 is providing resistance.

- On the downside, 1.37 is under strong pressure. 1.3650 is next.

EUR/USD Fundamentals

- 8:15 Spanish Services PMI. Exp. 55.3, actual 53.7 points.

- 8:45 Italian Services PMI. Exp. 50.6, actual 52.9 points.

- 9:00 Eurozone Final Services PMI. Exp. 51.7, actual 52.6 points.

- 10:00 Eurozone Retail Sales. Exp. 0.9%, actual 1.6%.

- 10:00 Eurozone Revised GDP. Exp. 0.3%, actual 0.3%.

- 13:15 US ADP Non-Farm Employment Change. Exp. 159K.

- 14:00 US Final Services PMI. Exp. 52.7 points.

- 15:00 US ISM Non-Manufacturing PMI. Exp. 53.8 points.

- 15:30 US Crude Oil Inventories. Exp. 0.9M.

- 19:00 US Beige Book.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Eurozone data a mix: There was good news from Eurozone Retail Sales, as the key consumer spending indicator jumped 1.6%, easily beating the estimate of 0.9%. Eurozone Services PMIs painted a mixed picture of the services sector. Spain’s numbers dropped to 53.7 in February, well below the estimate of 55.3. There was better news from Italian Services PMI, which pushed above the 50-point line for the first time since September. The index rose to 52.9 points, beating the estimate of 50.6. Eurozone Final Services PMI climbed to 52.6 points, above the estimate of 51.7. With recent Eurozone numbers looking respectable, ECB head Mario Draghi may opt to hold the course and not make any monetary moves this week.

- Spanish Unemployment Change shocker: If there was an academy award for the most unpredictable economic release in the Eurozone, Spanish Unemployment Change would have to be considered one of the favorites to win. The indicator has fluctuated wildly in recent readings, posting huge moves and leaving markets estimates in tatters. In the February release, the indicator posted a small loss of -1.9 thousand, shocking the markets which had braced for a gain of 74.2 thousand. Spanish indicators have looked solid so far in 2014, and on Monday, Manufacturing PMI posted a respectable reading of 52.5 points, pointing to slight expansion.

- Ukraine drama continues: All eyes remain on the Ukraine, as Russia has effectively taken over Crimea following the ousting of the Ukrainian president, who has fled to Russia. The US and Russia continue to talk tough and this has caused plenty of movement in the markets. If the tension continues and turns into a full scale war and/or a division of the Ukraine, the outstanding debt may never be repaid and Europe could suffer a blow. In the meantime, the big winner is the Swiss franc.

- Breathing room for the ECB: The big surprise out of Brussels seems to have shelved plans for a negative deposit rate. With core inflation at 1%, Draghi can fend off criticism. ECB Governing Council member Ignazio Visco said that a negative deposit rate is on the agenda in the upcoming March meeting (currently the rate is at 0%). While the ECB may not take action, this comment certainly weighed on the euro. It joins similar sentiments out of the ECB and some complaints about the euro’s strength from the head of the Eurogroup.

- Markets brace for weak NFP: US employment numbers have not looked good, and the markets are not expecting good news from ADP Non-Farm Payrolls later on Wednesday. At the moment, the assumption is that the Fed will continue its QE tapering moves also in March, despite recent hiccups in key economic numbers. Speaking before the US Senate last week, Janet Yellen acknowledged the slowdown in the US economy but did not hint about any change in QE tapering. However, forward guidance could certainly be adjusted if the unemployment rate continues falling. The meeting minutes indicated that interest rates are unlikely to rise, even if unemployment drops to 6.5%.

- German numbers impress: German retail sales rose by 2.5%, calming fears seen in the previous months. The number of unemployed in the euro-zone’s locomotive also fell more than expected and this joins the strong German GfK Consumer Confidence that reached 8.5 points, its highest level since January 2007. and the upbeat German Ifo Business Climate, which also posted a multi-year high. Germany is certainly doing well, but others are lagging behind, notably Italy and France.

More: Euro-zone inflation: a look to February 2013 can explain the surprise