EUR/USD has edged upwards on Wednesday. The pair is trading in the mid-1.37 range in the European session. US releases continue to raise concerns, as Retail Sales, PPI and Consumer Confidence all lost ground in September. The markets are keeping a close eye on the Federal Reserve, which will wrap up a policy meeting with a statement on Wednesday. As well, two key events will be released later in the day – ADP Non-Farm Payrolls and Core CPI. In the Eurozone, Spanish GDP and German Unemployment Change met market expectations.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

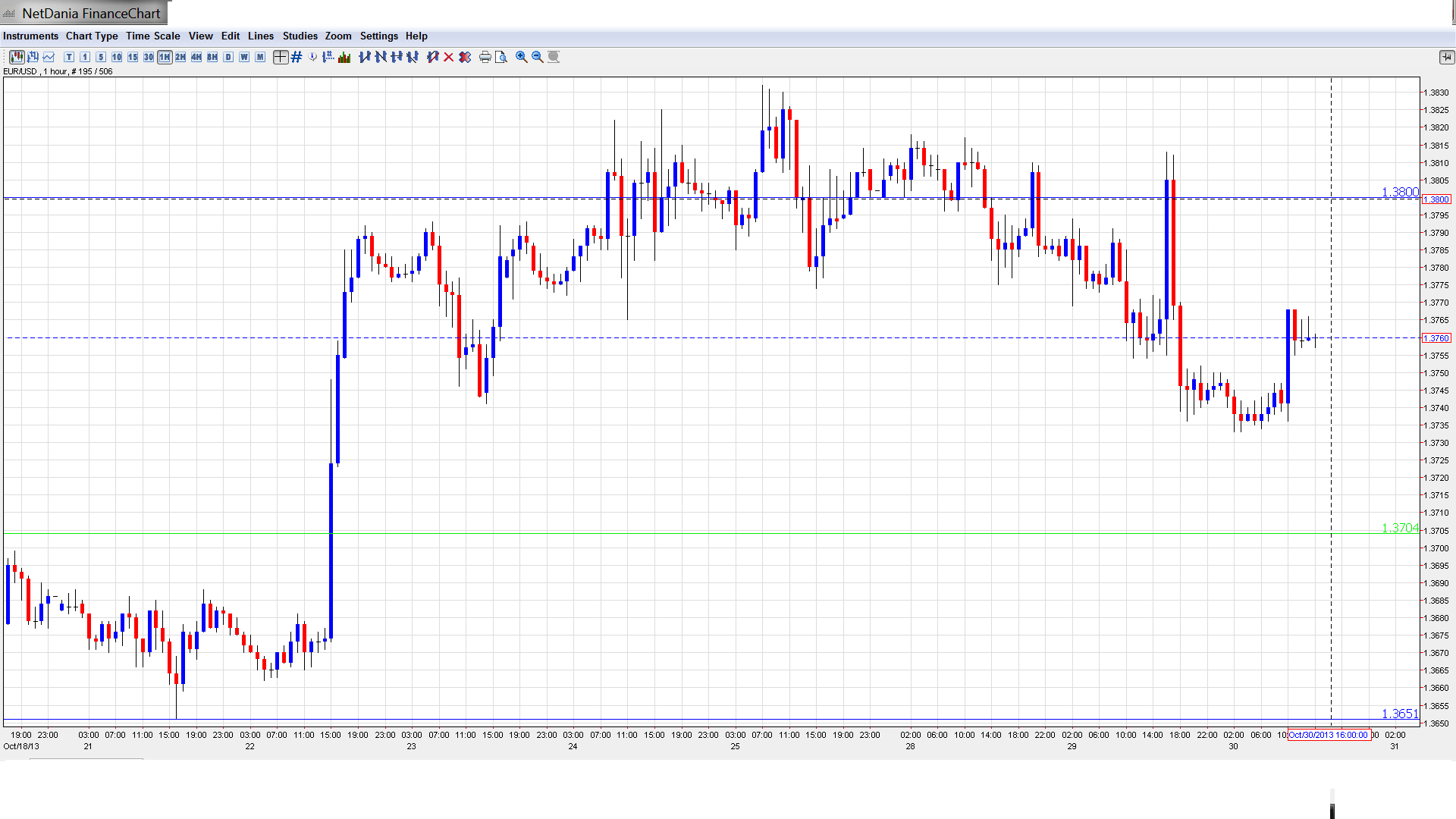

EUR/USD Technical

- In the Asian session, EUR/USD was quiet, consolidating at 1.3746. EUR/USD has edged higher in the European session.

- Current range: 1.3710 to 1.3800.

Further levels in both directions:

- Below: 1.3710, 1.3650, 1.3570, 1.3500, 1.3460, 1.3415, 1.3325 and 1.3240.

- Above: 1.3800, 1.3870, 1.3940, 1.4036, 1.41 and 1.4250.

- 1.3800 is a weak resistance line. 1.3870 is stronger.

- 1.3710 is providing weak support. It is followed by 1.3650.

EUR/USD Fundamentals

- All Day – German Preliminary CPI. Exp. 0.0%.

- 8:00 Spanish Flash GDP. Exp. 0.1%, Actual 0.1%.

- 8:55 German Unemployment Change. Exp. 1K, Actual 2K.

- 9:10 Eurozone Retail PMI. Actual 47.7 points.

- 10:12 Italian 10-year Bond Auction. Actual 4.11%.

- 10:34 German 10-year Bond Auction. Actual 1.71%.

- 12:15 US ADP Non-Farm Employment Change. Exp. 151K.

- 12:30 US Core CPI. Exp. 0.2%.

- 12:30 US CPI. Exp. 0.2%.

- 14300 US Crude Oil Inventories. Exp. 1.9M.

- 18:00 US FOMC Statement.

- 18:00 US Federal Funds Rate. Exp. <0.25%.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Fed back in spotlight: The Federal Reserve wraps up a policy meeting on Wednesday, the first meeting since Congress hammered out an agreement on the debt ceiling and reopened the government. However, the agreement is little more than a band-aid solution which puts off the debt ceiling and budget deadlock for a few months. Meanwhile, recent US data, notably employment numbers, have been sluggish. In this situation, the Fed is unlikely to push the taper trigger before next year. The markets will be waiting for the Fed policy statement later today, and we could see some volatility in the currency markets afterwards.

- US numbers continue to struggle: US releases continue to have a rough week. On Tuesday, PPI and Retail Sales both declined by 0.1%, missing the estimate of 0.2%. CB Consumer Confidence dropped sharply, from 79.7 to 71.2 points, a six-month low. This was well short of the estimate of 75.7 points. Core Retail Sales managed to match the forecast, rising to 0.4%. The mostly weak figures come on the heels of dismal housing numbers on Monday. If confidence in the US economy starts to weaken, we could see the US dollar, which is already under pressure from the major currencies, lose ground.

- Markets hope for good news from ADP Non-Farm Payrolls: After last week’s disappointing employment numbers, we’ll get a look at ADP Non-Farm Payrolls on Wednesday. Although this is not an official release, it is a key employment release which can move the markets. Last week, Unemployment Claims came in above the estimate and Non-Farm Payrolls tumbled to a six-month low. The US unemployment rate dipped to 7.2%, a five-year low, but this does not point to increased employment, as the participation rate remained at 63.8%, its lowest level since 1978. These figures indicate that the US labor market continues to have difficulty creating new jobs. The weak readings are weighing on the US dollar, which finds itself close to two-year lows against the euro.

- German unemployment numbers point to slowdown: German Unemployment Change came in at 2 thousand in September, just above the estimate of 1 thousand. Although this is a decent reading, this is the indicator’s third consecutive increase, raising concerns that the German economy is slowing down. The jobless rate was unchanged at 6.9 percent. If the Eurozone is to remain out of recession, it can ill afford for Germany, the region’s number one economy, to slow down. We’ll get a look at other key German releases on Thursday.