EUR/USD continues to show little movement so far this week as the pair is trading in the high-1.35 range in Tuesday’s European session. Today’s highlights are two German releases. Trade Balance showed a strong improvement in September, and the markets are hoping that Factory Orders, which will be released later, will follow suit. There are only two minor releases out of the US, so the markets will be paying more attention to the FOMC minutes, which will be released on Wednesday. It’s Day 8 of the shutdown, with no end in sight to the crisis.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

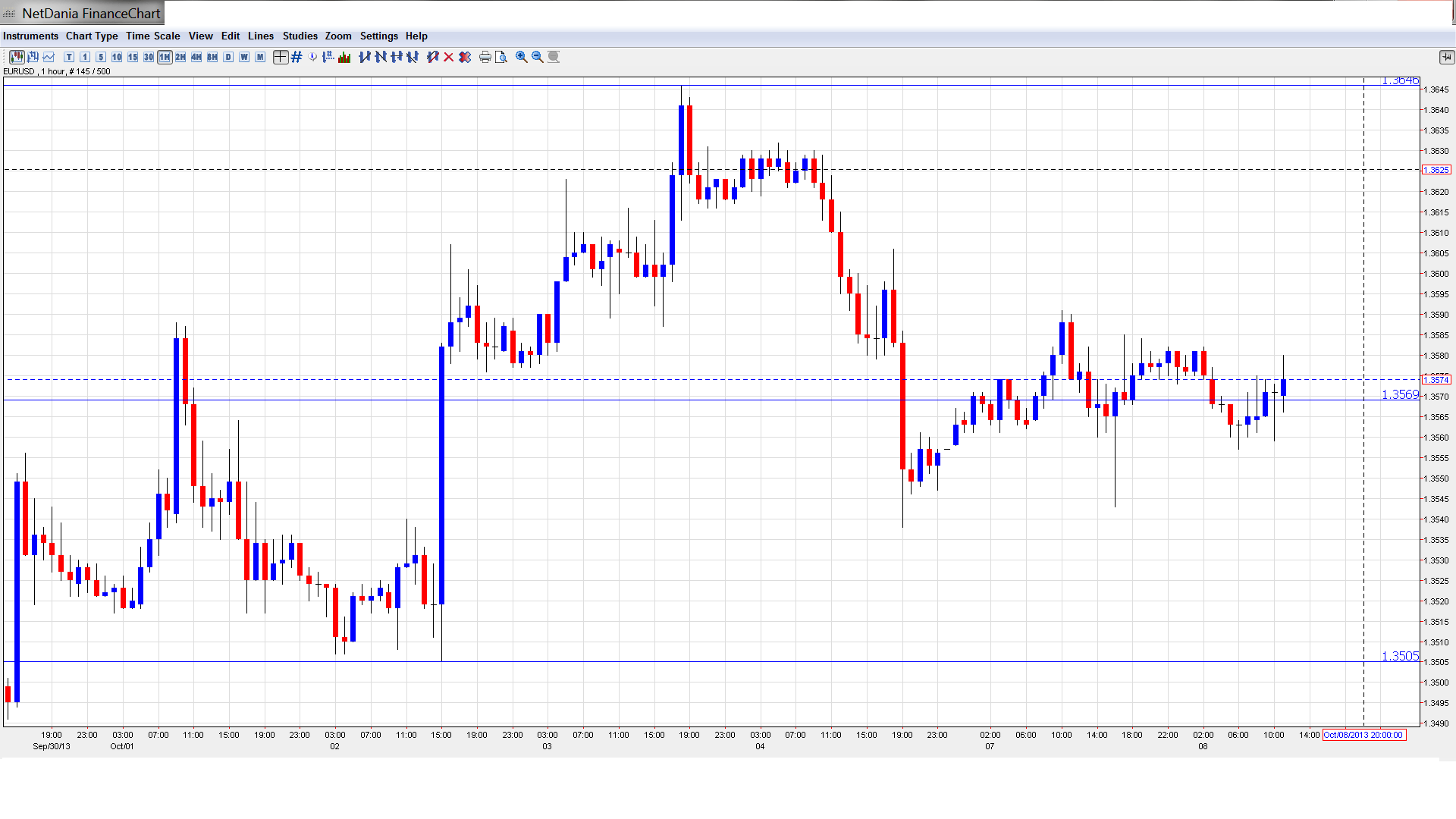

EUR/USD Technical

- In the Asian session, EUR/USD moved slightly lower late in the session, touching a low of 1.3558. The pair has edged higher in the European session.

- Current range: 1.3570 to 1.3650.

Further levels in both directions:

- Below: 1.3570, 1.3500, 1.3460, 1.3415, 1.3325, 1.3240, 1.3175, 1.31, 1.3050 and 1.3000.

- Above: 1.3650, 1.3710, 1.3800, 1.3870 and 1.3940.

- On the downside, 1.3570 is under strong pressure. 1.3500 follows.

- 1.3650 continues to provide resistance.

EUR/USD Fundamentals

- 6:00 German Trade Balance. Exp. 15.1B, Actual 15.6B.

- 6:45 French Government Budget Balance. Exp. -93.6B.

- 6:45 French Trade Balance. Exp. -4.8B. Actual -4.9B.

- 10:00 German Factory Orders. Exp. 1.2%.

- 11:30 US NFIB Small Business Index. Exp. 95.2 points.

- 14:00 US IBD/TIPP Economic Optimism. Exp. 46.2 points.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- German trade surplus widens: There was good news out of Germany, as the trade surplus widened to 15.6 billion euros, compared to 14.5 billion the previous month. This easily beat the estimate of 15.1 billion. We’ll get a look at German Factory Orders later today, and German Industrial Production on Wednesday. Strong readings would point to an improving German economy, which help boost the euro.

- US shutdown drags on: The US government shutdown is entering its second week, with no end in sight. Democrats and Republicans have dug their trenches, and each side is blaming the other for the impasse. Republicans want to reopen discussion about the national health care act, known as Obamacare, before approving the budget. The Democrats have refused, saying the budget must first be passed before any discussions can be held. There are growing concerns that a prolonged shutdown will hurt the fragile US recovery. If the shutdown does continue, we could see some instability in the markets this week, and the US dollar, which is already under strong pressure, could lose ground.

- Debt ceiling looms: As political squabbling has held up the US budget, a far more serious crisis is lying just around the corner – the debt ceiling. The US has a debt worth $16.7 trillion, and will run out of funds to service the debt by October 17, unless Congress authorizes raising the debt ceiling. Otherwise, the US could potentially default on its obligations, which could cause chaos in the domestic and international markets. Republican House Speaker John Boehner seems to have hardened his position, saying on the weekend that the Republicans would not raise the debt ceiling without a “serious conversation” about what is driving the debt to such high levels. With less than 10 days until the ceiling is reached, the markets could get volatile if the politicians in Washington don’t get their act together quickly.

- QE tapering unlikely in 2013: There was a lot of expectation that the Federal Reserve would taper QE in September, and most analysts were caught by surprise when the Fed opted not to reduce the bond-buying program. However, things have changed dramatically in the past few weeks, with the budget deadlock in Washington and fears about a debt ceiling crisis. Even if both of these issues are resolved tomorrow, the distortions and delays in key economic data will make it difficult for the Fed to have an accurate, up-to-date picture of the US economy. This was underscored on Friday, as Non-Farm Payrolls and the Unemployment Rate releases were cancelled on Friday. So in all likelihood, we won’t see a tapering of QE in the next few months. The FOMC minutes will be released on Wednesday, and this event can be a market-mover for EUR/USD.

- Low growth, low inflation, low rates for Eurozone: As expected, the ECB maintained its key interest rate at 0.50% last week. ECB President Draghi downplayed risks to the fragile Eurozone economy, and repeated that interest rates would remain at current or lower levels for an “extended period of time” given the low growth levels and weak inflation in the Eurozone. Friday’s PPI releases underscored the lack of inflation in the Eurozone, as German PPI declined by 0.1%, while Eurozone PPI dropped to a flat 0.0%. With little growth and low inflation, there’s little room for interest rates to go anywhere but down.