EUR/USD started off the week in fine fashion, posting gains of close to one cent on Monday. The pair has settled down on Tuesday, trading in the mid-1.32 range in European trading. Taking a look at economic releases, it’s another quiet day, with just a handful of events on Tuesday. French Industrial Production slumped, posting its third consecutive decline. Today’s highlight is the US JOLTS Job Openings, with the markets are not expecting much change.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

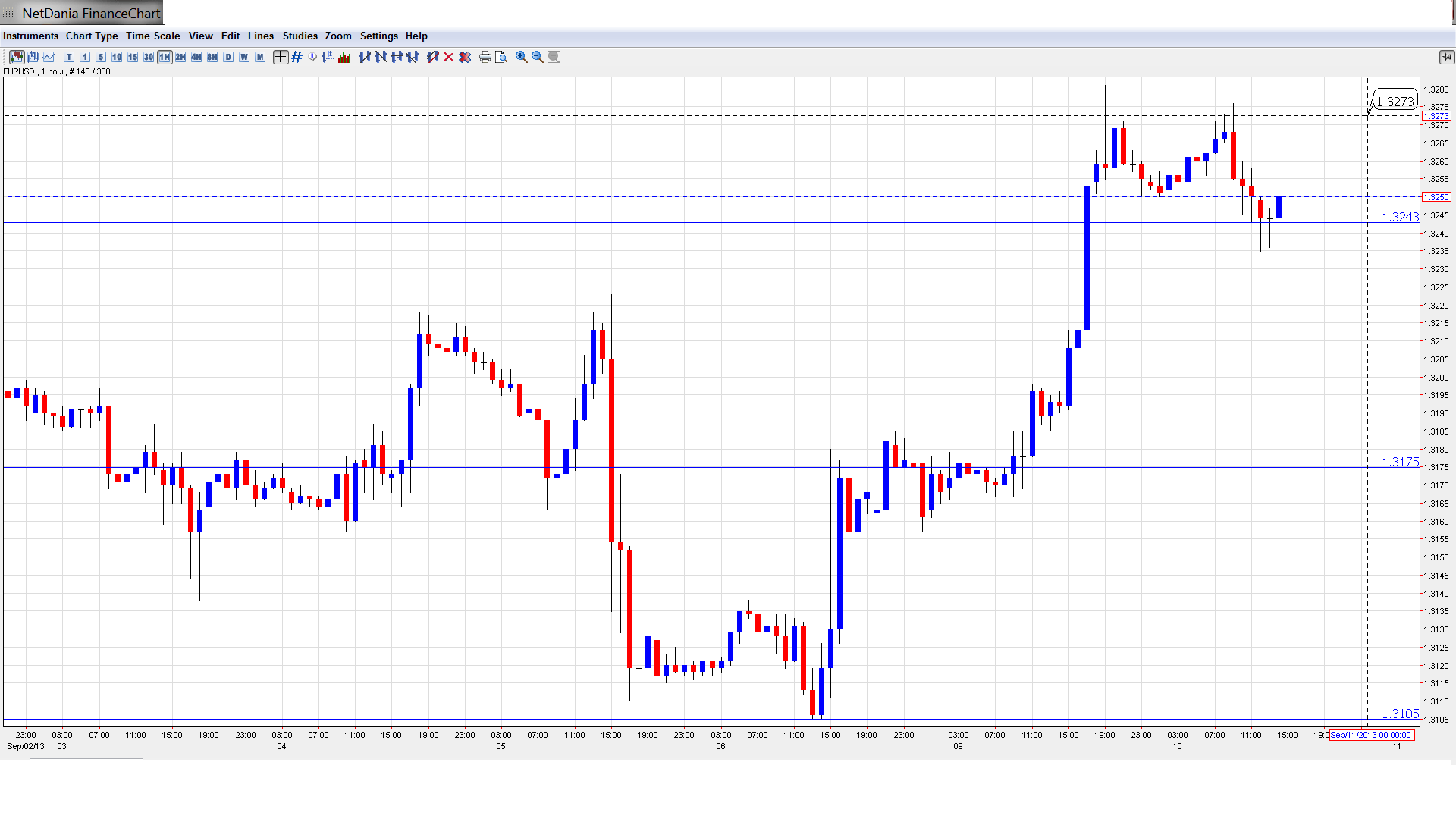

EUR/USD Technical

- In the Asian session, EUR/USD remained stable and touched a high of 1.3276 before consolidating at 1.3268. The pair has edged lower in the European session.

Current range: 1.3240 to 1.33.

Further levels in both directions:

- Below: 1.3240, 1.3175, 1.31, 1.3050 and 1.30.

- Above: 1.33, 1.3350, 1.3415, 1.3450, 1.3520, 1.3590 and 1.37.

- 1.3240 continues to provide support.

- 1.33 is providing weak resistance. 1.3350 is next.

EUR/USD Fundamentals

- 6:45 French Industrial Production. Exp. 0.7%, actual -0.6%.

- 11:30 US NFIB Small Business Index. Exp. 94.8 points.

- 14:00 US JOLTS Jobs Openings. Exp. 3.96M.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Confidence on the rise in Eurozone: Confidence indicators out of the Eurozone have been looking up and the Eurozone Sentix Investor Confidence continued the positive trend on Monday. The indicator shot up from -4.9 points in July to a solid +6.5 points in August. Remarkably, this was the first reading above zero since August 2011, indicative of entrenched pessimism among investors over the past two years. The markets will be hoping that other confidence indicators follow suit with strong readings.

- Weak US NFP may delay QE: The markets continue to speculate about QE tapering, but a weak Non-Farm Payrolls release may delay the time frame. NFP came in at 169 thousand, missing the estimate of 178 thousand. The Unemployment Rate dropped from 7.4% to 7.3%, but this improvement is not all that significant, given the low participation rate in the labor force. The Fed continues to keep its cards away from prying market eyes, but we’re unlikely to see QE tapering without stronger employment numbers. Chicago Fed President Charles Evans hinted that we could see some action on this front from the Fed before the end of the year. Septapering still, however, remains a credible possibility.

- Only a green recovery in Europe: ECB president Mario Draghi said he is “not enthusiastic” about the return to growth and warned about money markets. In addition, the ECB lowered its growth forecast for 2014. A rate cut is still on the cards, and forward guidance is here to stay. On this background, the euro remains weak, and not only against the dollar.

- Syrian tensions are on the rise: A US military strike seems closer, as the military makes preparations and there are higher chances for an approval from Congress. The story is expected to unfold next week, as Congress gears up for a vote on whether to approve military action against Syria. We can expect some volatility in the markets as tensions continue. Only an extreme escalation in Syria can prevent QE tapering.

Further reading:

- EURUSD Could Be Forming A Major Turning Point For The Year-Elliott Wave Analysis

- Forex Analysis: EUR/JPY Continues Consolidation within Clear Triangle Pattern