EUR/USD is stable on Tuesday, following gains a day earlier. In the European session, the pair is trading in the mid-1.35 range. On the release front, German ZEW Economic Sentiment continued to lose ground and fell short of the estimate. Eurozone ZEW Economic Sentiment improved in May but also fell short of the forecast. Over in the US, we’ll get a look at two key releases – Building Permits and Core CPI. Here is a quick update on what’s moving the pair.

- EUR/USD was steady in the Asian session, trading around the 1.3560 line. The pair is unchanged in the European session.

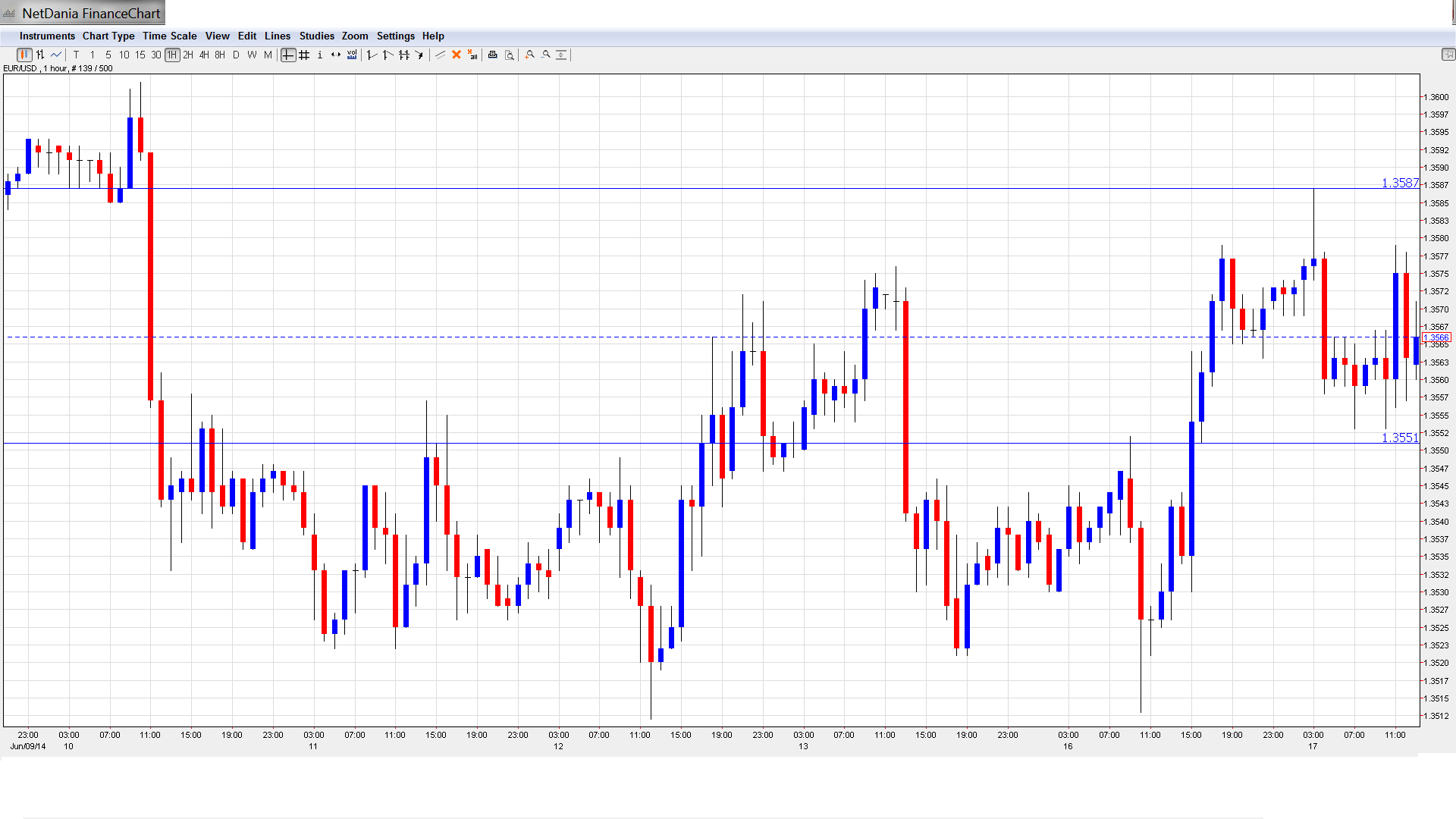

- Current range: 1.3550 to 1.3585.

Further levels in both directions:

- Below: 1.3550, 1.35, 1.3450, and 1.34

- Above: 1.3585, 1.3650, 1.3677, 1.37, 1.3740, 1.3785, 1.3830, 1.3865 and 1.3905.

- 1.3550 is a weak support line which could break during the day. The round number of 1.35 is next.

- 1.3585 is an immediate resistance line. 1.3650 is stronger.

EUR/USD Fundamentals

- 8:00 Eurozone Italian Trade Balance. Estimate 4.27B, actual 3.51B.

- 9:00 German ZEW Economic Sentiment. Estimate 35.2, actual 29.8 points. See how to trade this event with EUR/USD.

- 9:00 Eurozone ZEW Economic Sentiment. Estimate 59.6 points, actual 58.4 points.

- 12:30 US Building Permits. Estimate 1.07M.

- 12:30 US Core CPI. Estimate 0.2%.

- 13:00 US CPI. Estimate 0.2%.

- 13:15 US Housing Starts. Estimate 1.04M.

*All times are GMT For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- German Economic Sentiment slips: German ZEW Economic Sentiment, a well-respected indicator, continues to lose ground throughout 2014. The index weakened to 29.8 points, well off the estimate of 35.2 points. This was the worst reading we’ve seen since November 2012. Eurozone ZEW Economic Sentiment improved in May, climbing to 58.4 points. However, this fell short of the estimate of 59.6. Despite the dismal German release, the euro is holding its own against the US dollar.

- Fed expected to hold course: The US Federal Reserve will issue a policy statement on Wednesday, with the markets expecting another $10 trim to QE, which would reduce the asset purchase program to $35 billion/month. Fed chair Janet Yellen is not expected to provide any time guidelines about a rate hike, so traders shouldn’t expect a repeat of the fireworks we saw with the British pound, which soared following comments by BOE Governor Mark Carney.

- Eurozone inflation remains weak: Even though the ECB has already made its decision, inflation data remains of importance for the next moves. French and Spanish inflation numbers remain weak, and Eurozone CPI remains well below the ECB’s target of 2.0%. A dip below these levels could add pressure on the euro and force the ECB to take further monetary measures at the July policy meeting.

- US consumers buying less: The American consumer is not as active as expected in the second full month of the spring. With the US economy reliant on consumption, this isn’t encouraging. As well, UoM Consumer Sentiment softened in May and fell short of the estimate. This points to a decrease in consumer confidence, which doesn’t bode well for economic growth.

- Euro weighed by yield differential: The impact of Draghi is still felt on markets: yields in the euro-zone are low and they are beginning to be in contradiction with other regions: the BOE’s Mark Carney said that UK rates will rise sooner than current expectations and this boosted the pound. EUR/GBP fell below 0.80. In New Zealand, the hawkish central bank hints at more hikes. On this background, the easing ECB could push the euro even lower. We will get the US rate decision next Wednesday.