EUR/USD continues to point downward on Friday, as the pair trades in the low-1.36 range in the European session. The pair has now lost about 150 points since the Federal Reserve announced on Wednesday that it will taper QE by $10 billion. US releases were a major disappointment, as Unemployment Claims rose last week. As well, Existing Home Sales and the Philly Manufacturing Index fell short of their estimates. On Friday, German PPI posted another decline, but German Consumer Climate posted its best reading in six years. Today’s US highlight is Final GDP.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

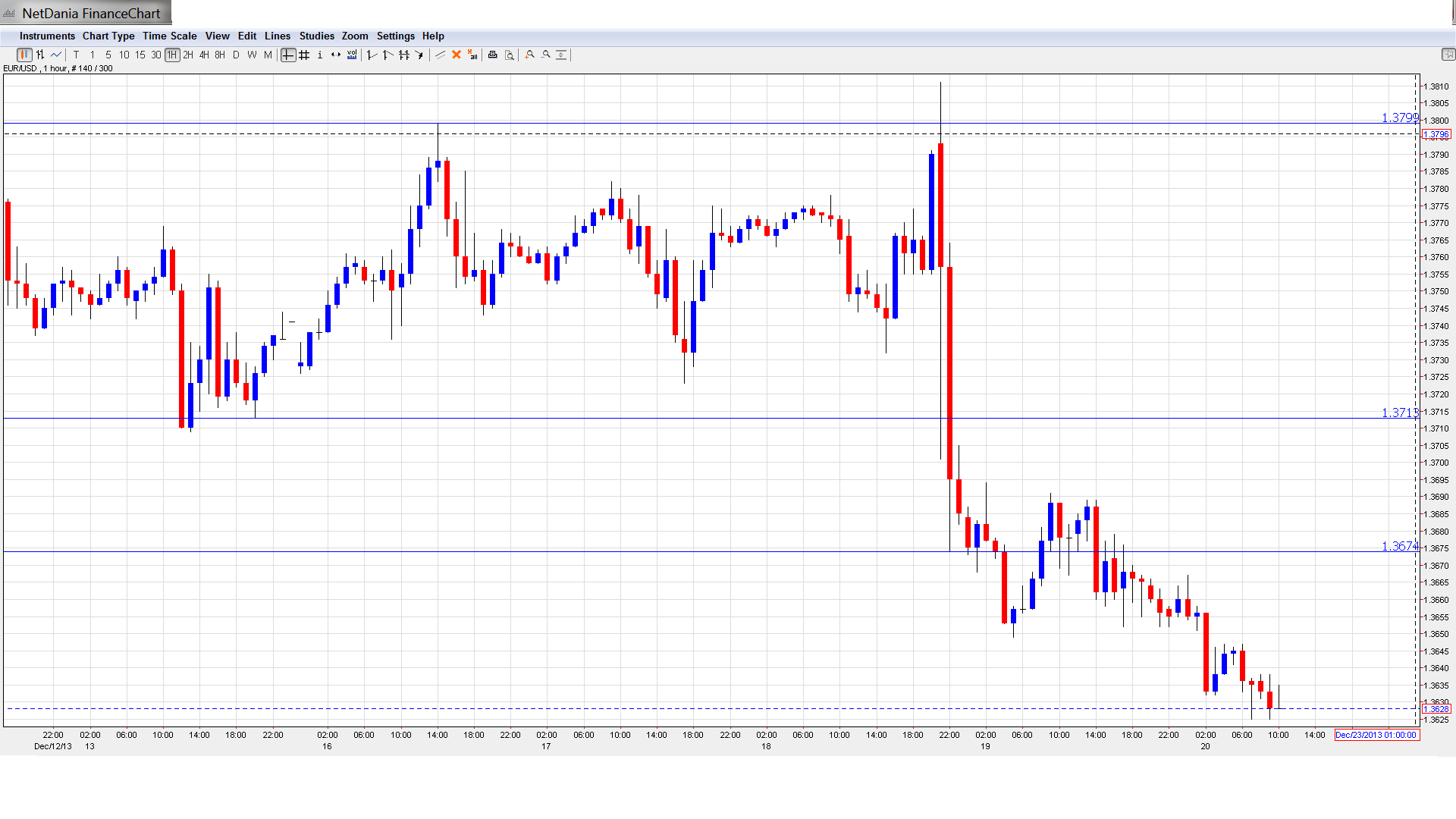

EUR/USD Technical

- EUR/USD lost ground in the Asian session and consolidated at 1.3627. The pair is unchanged in the European session.

- Current range: 1.3615 to 1.3675.

Further levels in both directions:

- Below: 1.3615, 1.3525, 1.3440, 1.34, 1.3320, 1.3240, 1.3175 and 1.31.

- Above: 1.3675, 1.3710, 1.3800, 1.3832, 1.3940 and 1.4036.

- 1.3675 is the next resistance line. 1.3710 follows.

- 1.3615 is providing weak support. 1.3525 is stronger.

EUR/USD Fundamentals

- 7:00 German PPI. Exp. 0.0%, Actual -0.1%.

- 7:00 GfK German Consumer Climate. Exp. 7.4, Actual 7.6 points.

- Day 2 – EU Economic Summit.

- 10:00 Italian Retail Sales. Exp. 0.2%.

- 13:30 US Final GDP. Exp. 3.6%.

- 13:30 US Final GDP Price Index. Exp. 2.0%.

- 15:00 Eurozone Consumer Confidence. Exp. -15 points.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- German Consumer Climate jumps: German Consume Climate climbed from 7.4 to 7.6 points, its best reading since August 2007. On the inflation front, German PPI posted another decline, its fourth in five releases, as inflation indicators in Germany and the Eurozone continue to point to weak inflation, despite record low interest rate levels in the Eurozone. Germany is the Eurozone’s largest economy, and if the region is to shake off weak economic growth and high unemployment, it will need the German locomotive to lead the way.

- US numbers disappoint: US releases on Thursday were dismal. Unemployment Claims jumped to 379 thousand claims last week, up from 368 thousand the week before. This was well above the estimate of 336 thousand. The previous release’s weak numbers were attributed to the holiday season, but two consecutive bad releases will certainly not comfort the markets. There was more bad news to follow. Existing Home Sales posted its third consecutive decline, dropping to 4.90 million compared to 5.12 million in the previous release. The Philly Fed Manufacturing Index rose from 6.5 to 7.0 points, but this was way off the estimate of 10.3 points.

- Fed announces $10 billion taper to QE: There was plenty of drama preceding the Federal Reserve statement on Wednesday, and anyone hoping for exciting news was not left disappointed. The Fed announced that it was tapering its QE program by $10 billion a month, commencing in January. This will reduce the Fed’s asset purchases to $75 billion, comprised of $40 billion in Treasuries and $35 billion in mortgage bonds. The announcement came as somewhat of a surprise, as most analysts had not expected the Fed to take action until early next year. The currency markets reacted sharply to the news, and EUR/USD dropped over one cent.

- Tapering yes, rate hike no: The Federal Reserve was careful to separate tapering expectations from rate hike expectations. Fed chairman Bernard Bernanke stated that interest rates are likely to remain low even after the unemployment rate drops below 6.5%. Previously, the Fed had stated that it would start to consider rate increases when unemployment fell below this level. Bottom line? With the unemployment rate at 7.0%, it could be a while before we see higher rates in the US.

- Senate passes budget agreement: A two-year, bipartisan budget agreement is moving quickly through Congress. The deal was overwhelmingly approved in the House of Representatives last week and the Senate followed suit on Wednesday, passing the measure by a vote of 64-36. The bill will now go the President Obama for his signature, before becoming law. The agreement sets limits on government spending for two years and reduces the deficit by a modest $23 billion. Democrats and Republicans both had criticism of the proposal, but there is general agreement in Washington that the compromise reached is a positive step which removes the threat of a shutdown which paralyzed the government in October for 16 days.