EUR/USD has been trading quietly around the Christmas holiday, but that has changed in dramatic fashion in Friday trading, as low liquidity has led to strong upward movement from the euro. The pair has added about one cent on the day and is poised to cross above the 1.38 level in Friday’s European session. On Thursday, US Unemployment Claims posted sharp drops and beat the estimate. The week wraps up with two releases, both from the US. There are no Eurozone releases on Friday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

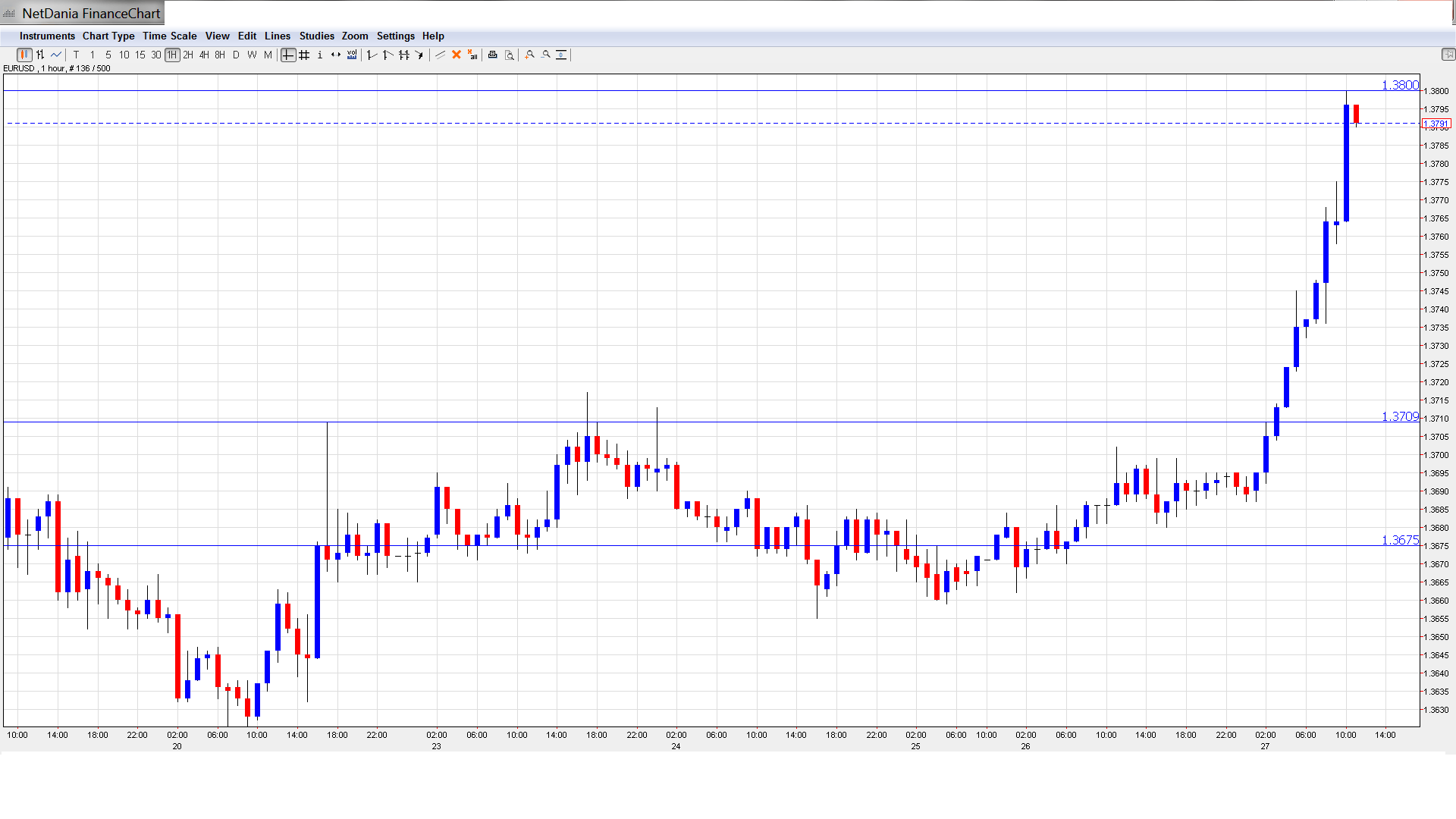

EUR/USD Technical

- EUR/USD was on the move upwards throughout the Asian session, barreling above the 1.37 early in the session. The pair consolidated at 1.3764. The pair continues to push higher in the European session and is testing the 1.38 line.

- Current range: 1.3675 to 1.3710.

Further levels in both directions:

- Below: 1.3710, 1.3675, 1.3615, 1.3525, 1.3440, 1.34, 1.3320, 1.3240, 1.3175 and 1.31.

- Above: 1.3800, 1.3832, 1.3940 and 1.4036.

- On the upside, 1.3800 is under strong pressure. 1.3832 follows.

- On the downside, 1.3710 has strengthened as the euro has moved higher. 1.3615 is next.

EUR/USD Fundamentals

- 15:30 US Natural Gas Storage. Exp. -177B.

- 16:00 US Crude Oil Inventories. Exp. 0.5%.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Unemployment Claims Shine: US Unemployment Claims bounced back nicely on Thursday, following two disappointing releases. The key employment indicator fell to 338 thousand, compared to 379 thousand in the previous release. The estimate stood at 346 thousand. With the Federal Reserve poised to begin its long-awaited QE taper next month, employment releases have taken on added significance. If the US labor market continues to improve, the Fed could decide on another taper as early as January, which would give a boost to the US dollar against its major rivals.

- US manufacturing, housing numbers point up: There was some early holiday cheer from US releases on Tuesday, as manufacturing and housing data pointed upwards. Core Durable Goods Orders posted a strong gain of 1.2%, its best showing since April. The key manufacturing indicator had posted four consecutive declines, so the sharp gain was welcome news. Durable Goods Orders bounced back from a sharp decline in October with a gain of 3.5%, well above the estimate of 1.7%. New Homes Sales also impressed with a five-month high, climbing to 464 thousand. The estimate stood at 449 thousand.

- French Consumer Spending climbs: The markets are not used to seeing strong numbers out of France, so Tuesday’s Consumer Spending data was unexpected good news. The indicator posted a gain of 1.4%, its strongest gain since September 2010.Four of the five past releases have been declines, and the November estimate stood at 0.3%. The solid reading comes after a string of poor releases from the Eurozone’s second largest economy. Services and Manufacturing PMIs pointed to contraction, while Industrial Production continues to post declines.

- Eurozone inflation continues to lag: The ECB has an inflation target of about 2%, but Eurozone inflation indicators are pointing to numbers well off that mark. Eurozone CPI improved to 0.9% in November, less than half of the ECB’s inflation target. German PPI posted a decline of 0.1%, the fourth decline in five releases. Germany is the Eurozone’s largest economy, and if the region is to shake off weak economic growth and high unemployment, it will need the German locomotive to lead the way.