EUR/USD has edged lower in Tuesday trading, as the pair trades in the low 1.35 range. The euro remains under pressure after German ZEW Economic Sentiment fell short of the estimate. Eurozone ZEW Economic Sentiment looked sharp, posting a strong gain in December. In the US, it’s an unusually quiet week, with no releases until Thursday.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

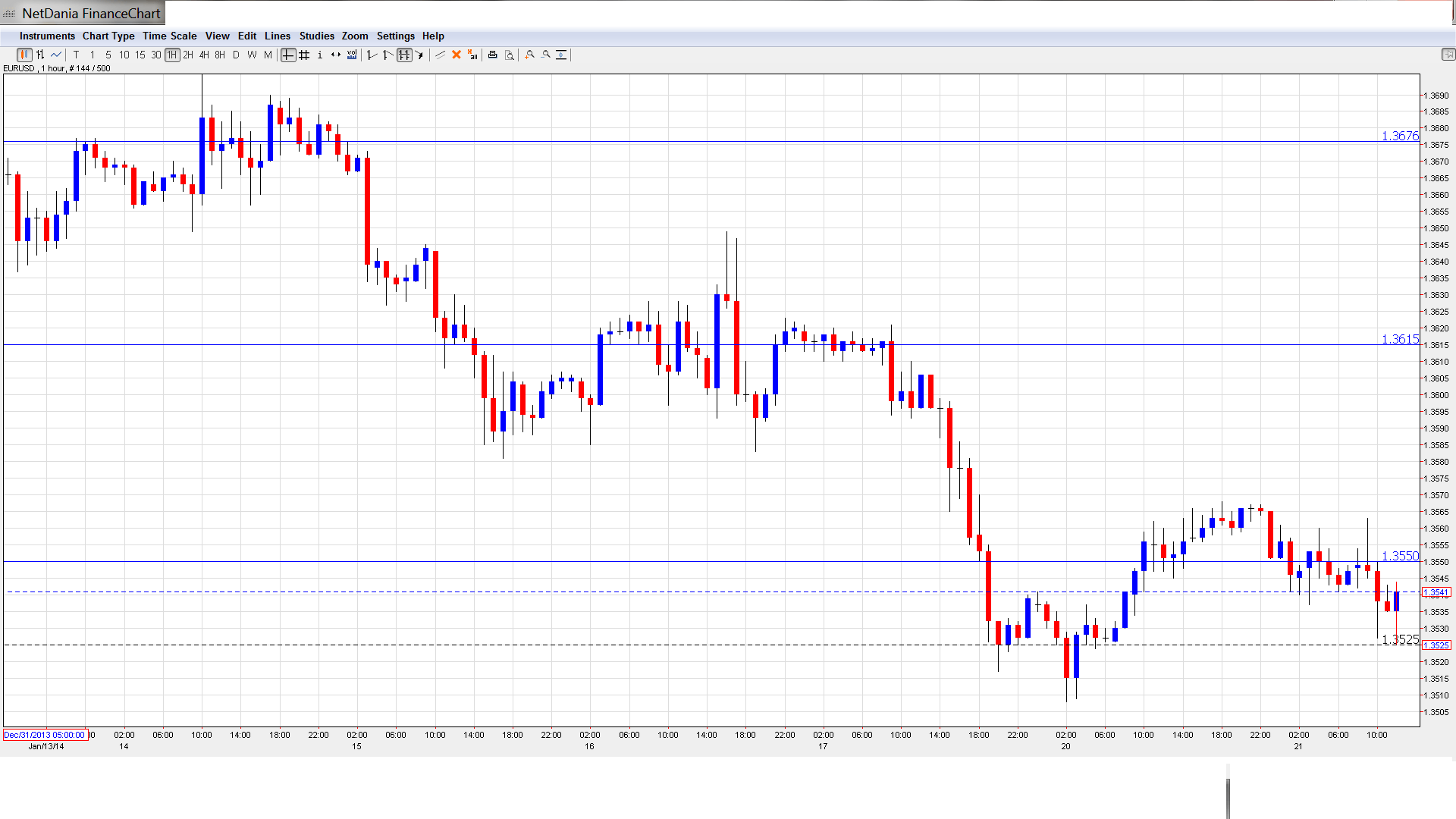

EUR/USD Technical

- EUR/USD traded close to 1.3550 for most of the Asian session. It has edged lower early in the European session.

Current range: 1.3450 to 1.3550.

Further levels in both directions:

- Below: 1.3450, 1.34, 1.3320, 1.3240 and 1.3175.

- Above: 1.3550, 1.3615, 1.3675, 1.3710, 1.3800, 1.3832, 1.3940 and 1.4036.

- 1.3450 is providing strong support.

- 1.3550 has reverted back to resistance. 1.3615 is stronger.

EUR/USD Fundamentals

- 10:00 German ZEW Economic Sentiment. Exp. 63.4, actual 61.7 points.

- 10:00 Eurozone ZEW Economic Sentiment. Exp. 70.2, actual 73.3 points.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- German Consumer Sentiment misses mark: German ZEW Consumer Sentiment didn’t show much change in December, coming in at 61.7 points, compared to 62.0 points a month earlier. However, the key indicator fell well short of the estimate of 63.4 points. The all-European release surprised with a sharp rise, climbing to 73.3 points, up from 68.3 a month earlier. This easily beat the estimate of 70.2 points. The euro responded with a slight drop against the dollar.

- Deflation Concerns Continue in Europe: Eurozone indicators continue to point to weak inflation, and this was underscored on Monday, as German PPI posted another weak reading, posting a gain of just 0.1%. While the ECB seems concerned with low inflation and not outright deflation, any further deterioration could push the ECB to set a negative deposit rate as soon as March 2014. This is a primary source of euro vulnerability.

- German strength: German growth seems solid as we start 2014. PMIs are upbeat and business sentiment is strong in the bloc’s largest economy. The ZEW Economic Sentiment did fall short of the estimate, but posted another strong reading.

- French recession?: We’ll get a look at French PMI numbers on Thursday, and these key readings could show once again that the economic situation in France is worsening. While the German economy seems solid and Spain has surprised the markets with some strong numbers, it will be hard for the Eurozone to enjoy stability while Italy is struggling and core France is squeezing.

- US consumer still buying: US retail sales numbers painted a mixed picture. Retail sales rose by only 0.2%, meeting forecasts. The up side came from core sales, which jumped by 0.7%, compared to 0.4% the month before. This easily beat the estimate of 0.4%. Also consumer confidence remains on high ground. December is a key month in US shopping, so January’s consumer spending numbers could taper off.

- Will Fed taper again in January?: The dismal Non-Farm Payrolls report may have created some concern about the US employment picture, but it seems to be totally forgotten, after quite a few positive figures, such as the Philly Fed Index and the surging Empire State Mfg. indicator. The Federal Reserve’s path of tapering QE, which it started just this month, is predicted to be followed with another $10 billion taper on January 29th. In December, outgoing Fed chair Bernard Bernanke strong hinted that the Fed planned to wind up QE by the end of 2014, reducing the asset-purchase program by increments of $10 billion at each meeting. The Fed next meets for a policy meeting next week, and the question is will the Fed reduce QE by another $10 billion, lowering it to $65 billion each month. Most analysts feel that one bad employment report will not affect the taper schedule and we will see another reduction in QE at the next meeting. This would mark a strong vote of confidence by the Federal Reserve in the US economy, and could give the US dollar a lift.