EUR/USD is pointing higher on Wednesday, as the pair trades in the mid-1.38 range in the European session. In economic news, Eurozone and German PMIs beat the forecast, but French PMIs missed expectations. In the US, today’s highlight is New Home Sales. The markets are expecting the indicator to improve in March.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

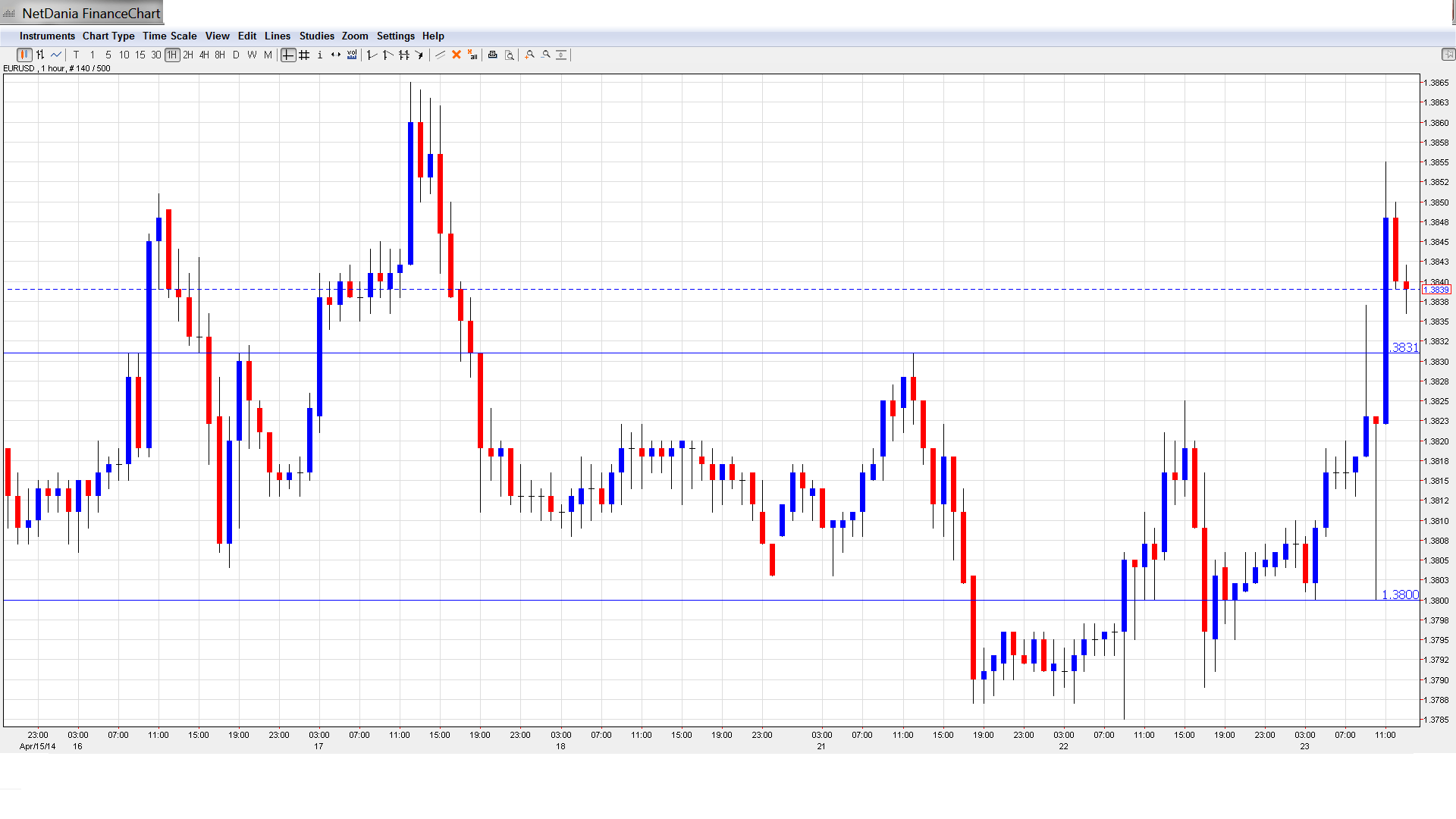

EUR/USD Technical

- EUR/USD edged higher in the Asian session, closing at 1.3820. The pair is moving higher in the European session.

Current range: 1.3800 to 1.3830.

Further levels in both directions:

- Below: 1.38, 1.3740, 1.37, 1.3650 and 1.3580.

- Above: 1.3830, 1.3895, 1.3964 and 1.40.

- 1.3830 has switched to a support role. The round number of 1.38 follows.

- 1.3895 is the next resistance line.

EUR/USD Fundamentals

- 7:00 French Flash Manufacturing PMI. Exp. 51.9, actual 50.9 points.

- 7:00 French Flash Services PMI. Exp. 51.5, actual 50.3 points.

- 7:30 German Flash Manufacturing PMI. Exp. 53.9, actual 54.2 points.

- 7:30 German Flash Services PMI. Exp. 53.5, actual 55.0 points.

- 8:00 Eurozone Flash Manufacturing PMI. Exp. 53.0, actual 53.0 points.

- 8:00 Eurozone Flash Services PMI. Exp. 52.7, actual 53.1 points.

- 13:45 US Flash Manufacturing PMI. Estimate 56.2 points.

- 14:00 US New Home Sales. Exp. 455K.

- 14:30 US Crude Oil Inventories. Exp. 2.6M.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- PMIs highlight French/German divide: After an extended Easter holiday, there was plenty of numbers to crunch out of the Eurozone. German and Eurozone PMIs beat their estimates, while the French releases missed their estimates and weakened in March. The data highlights the French Services and Manufacturing PMIs remain slightly above the 50-point level, indicative of expansion.

- Eurozone inflation a sore spot: Eurozone inflation indicators continue to point to weak inflation, with no end in sight. German PPI posted a decline of -0.3%, its worst showing since December 2012. Final inflation data for March came out slightly lower than expected. While headline inflation was confirmed at 0.5%, the lowest since 2009, core inflation was downgraded to 0.7%, matching the low level seen in late 2013, which was the post-crisis low. The ECB has downplayed the danger of deflation, but Mario Draghi may have to take some action to try and raise inflation in the hope of stimulating the lackluster Eurozone economy.

- No worries over US inflation: The Eurozone is having a tough time with a lack of inflation, but in the US, it’s a different story. US core inflation actually rose to 1.7%, exactly in Goldilocks territory: there is no deflation danger and quite far from heating inflation, despite a bloated balance sheet at the Federal Reserve. The House Price Index rose a respectable 0.6% in March, matching the forecast.

- Markets hopeful for spring thaw: After a harsh US winter which took a toll on the economy, April figures have been encouraging. Recent job figures have been solid and retail sales exceeded expectations. An outstanding reading from the Philly Fed Index, has added to the hopes of a serious spring bounce. Existing Home Sales beat the estimate, and the markets will be looking for more positive housing data from New Home Sales on Thursday.

- Ukraine crisis escalates: The markets haven’t reacted to events in Ukraine so far, but that could change if the violence in the east of the country worsens. Russian President Vladimir Putin has threatened to act on his “right” to invade Ukraine, and has also given the country an ultimatum regarding its gas debt. The gas supply from Russia to western Europe is in danger, and if the situation spills out of control, we could see a sharp response from the markets. US Vice-President Joe Biden is in Kiev for a symbolic visit. The West doesn’t have many cards to play against Russia, so every move by Putin will be scrutinized and could impact on the markets.