EUR/USD finally fell out of range and closed the week on lower ground. Is this the beginning of a fall to new lows? The ECB rate decision is the key event in a week that also consists of inflation and PMI data. Here is an outlook for the highlights of this week and an updated technical analysis for EUR/USD.

Greece moved further towards towards the back burner, with the approval of the Greek list of reforms, but the noise continues and it’s only a 4 month plan. Euro-zone data continued beating to the upside but business confidence in Germany missed. In the US, Yellen made it clear that a removal of forward guidance does not imply an imminent rate hike, and this triggered volatility. However, the solid inflation data coupled with bullish Fed comments gave a boost to the greenback.

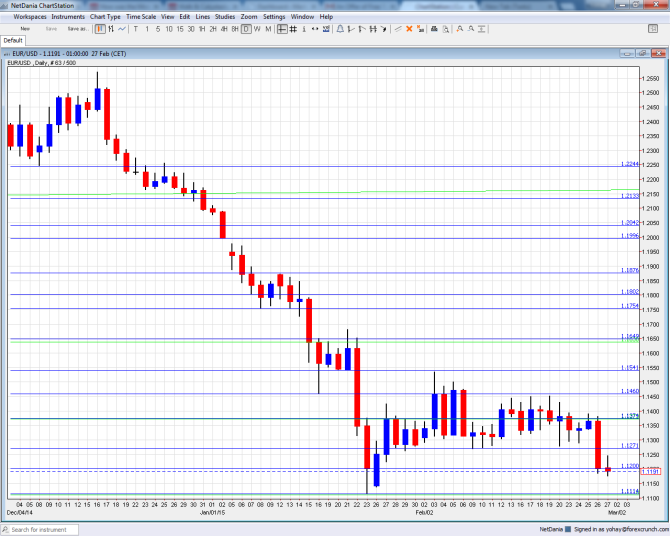

[do action=”autoupdate” tag=”EURUSDUpdate”/]EUR/USD daily chart with support and resistance lines on it. Click to enlarge:

- Manufacturing PMIs: Monday: Spain at 8:15, Italy at 9:$5 and the final EZ number at 9:00. In January, Spain enjoyed a solid growth rate according to Markit’s purchasing managers’ index: 54.7 points, above the 50 point mark separating growth and contraction. A rise to 55.2 is expected. On the other hand, Italy’s PMI was just under 50, at 49.9 points and is now predicted to edge up to 50.2.. The initial all-European read for February stood on 51.1 points, and will likely be confirmed now.

- Flash Inflation data: Monday, 10:00. The euro-zone deflation deepened in January, with -0.6% in headline inflation and only 0.6% in core inflation. These are year over year numbers. The initial numbers for February are expected to show a stabilization with a slightly higher y/y headline number of -0.5%. Core inflation will likely remain at 0.6%. Oil prices have stabilized.

- Unemployment Rate: Monday, 10:00. The high jobless rate in the euro-zone has finally begun going in the right direction, with a drop to 11.4%. The same number is expected this time.

- German Retail Sales: Tuesday, 7:00. The German consumer was relatively cautious in Christmas shopping: a gain of only 0.2% in December. A stronger growth rate is on the cards for January: +0.5%.

- Spanish Unemployment Change: Tuesday, 8:00. The euro-zone’s fourth largest economy has a sky high unemployment rate, but things are improving. After a rise of 78K in unemployment in January, another rise is likely for February: 10.5K. However, it is important to remember that employment is very seasonal in Spain.

- PPI: Tuesday, 10:00. Producer prices also enter the ECB’s calculation for future monetary policy. Prices have fallen by 1% in December and another slide is likely for January: -0.5%.

- Services PMIs: Wednesday: Spain at 8:15, Italy at 8:45 and the final EZ number at 9:00. The services sector is doing better in general. Spain enjoyed strong growth with 56.7 points in January and a tick up to 56.9 is on the cards now. Italy, the zone’s third largest economy had a positive 51.2 points here and is estimated to see 51.8 points. The initial number for the whole euro-zone was 53.9 in February and will likely be confirmed now.

- Retail Sales: Wednesday, 10:00. While released after the German data, the full publication still has a significant impact. After a rise of 0.3%, a similar number is predicted at this time: +0.2%.

- German Factory Orders: Thursday, 7:00. This indicator is quite volatile, but still has a significant impact. A jump of 4.2% followed a fall of 2.4%. The see-saw could continue with a drop now, of 0.8%.

- Retail PMI: Thursday, 9:10. This 1000 strong survey has shown contraction for long months. After printing a slide to 46.6 points in January, a rise in February could be seen.

- Rate decision: Thursday, 12:45, press conference at 13:30. In the previous decision, the ECB announced QE: a massive program to expand the balance sheet at a pace of €60 billion per month, with an intended end date of September 2016. No change in policy is expected now, but there are many things on the agenda: the ECB’s role in the Greek crisis, how Draghi sees inflation evolving after the stabilization in oil prices, hopes for growth and more. The president of the ECB usually moves markets.

- German Industrial Production: Friday, 7:00. Industrial output in the euro-zone’s locomotive has edged up only 0.1% in December, and probably expanded at a wider pace in January: 0.6%.

- French trade balance: Friday, 7:45. Contrary to Germany, France has a trade deficit that stood on 3.4 billion euros in December. Another squeeze is likely now.

- Final GDP: Friday, 10:00. The euro-zone economies grew by 0.3% according to the first release for Q4 2014, mostly thanks to strong German growth at +0.7%. This quarterly number will likely be confirmed now.

* All times are GMT

EUR/USD Technical Analysis

Euro/dollar started off the week with a slide from support at 1.1373 (mentioned last week) before trading in range. It then fell to 1.12.

Live chart of EUR/USD: [do action=”tradingviews” pair=”EURUSD” interval=”60″/]

Technical lines from top to bottom:

The post crisis low of 1.1867, should be watched. 1.1750 was a low point the pair reached in a breakdown in early January 2015. The round number of 1.17 was the launch value of the pair in 1999 and has a symbolic meaning.

Below, we have the post Swiss bounce of 1.1650 which worked as resistance. Lower, 1.1540 provided support in mid January.

Below the round number of 1.15 we have the pre-QE low of 1.1460 that could work as resistance.

1.1373 was the low line seen in November 2003 and proved to work as resistance and support lately. Below the initial low point of 1.1313 we have 1.1270, which provided support twice in February 2015.

The round number of 1.12 is now the pivotal line in the range. It is followed by the fresh low of 1.1113 which is nearly 0.90 on USD/EUR.

The next line is the round 1.10. It is followed by 1.0760, which was the low point in both July and August 2003.

Below this point we have the round numbers of 1.05 and 1 – EUR/USD parity, which is already eyed by some analysts.

I remain bearish on EUR/USD

Greece was gaining a lot of attention and it’s over over for now. This means that monetary policy divergence is back to the limelight and it doesn’t bode well for the pair. Draghi will remind us that euro-zone QE commences and is likely to weaken the euro, even if deflation doesn’t further deepen and even if there are some signs that the weak euro is already helping the economies. In the US, Yellen basically prepared us for the removal of forward guidance, and the NFP could boost the June rate expectations.

In this week’s podcast, we cover Yellen & the hike, AUD & CAD rate previews, Jobless claims vs. USD & Greek back burner

Subscribe to our iTunes page

Further reading:

- For a broad view of all the week’s major events worldwide, read the USD outlook.

- For the Japanese yen, read the USD/JPY forecast.

- For GBP/USD (cable), look into the British Pound forecast.

- For the Australian dollar (Aussie), check out the AUD to USD forecast.

- USD/CAD (loonie), check out the Canadian dollar forecast

- For the kiwi, see the NZDUSD forecast.