EUR/USD is lower in Friday trading, as the pair has again dropped below the 1.31 line. The euro lost ground as US Employment Claims looked very sharp on Thursday. After a quiet week, the markets will have plenty of US numbers to chew on, including four key releases – Core Retail Sales, Retail Sales, PPI and UoM Consumer Sentiment. As well, Fed Chairman Bernanke will address a conference in Washington. In the Eurozone, German WPI was well below the estimate, and the markets are keeping an eye on Eurozone Industrial Production, which will be released later today. Also, both the Eurogroup and ECOFIN are holding meetings today.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

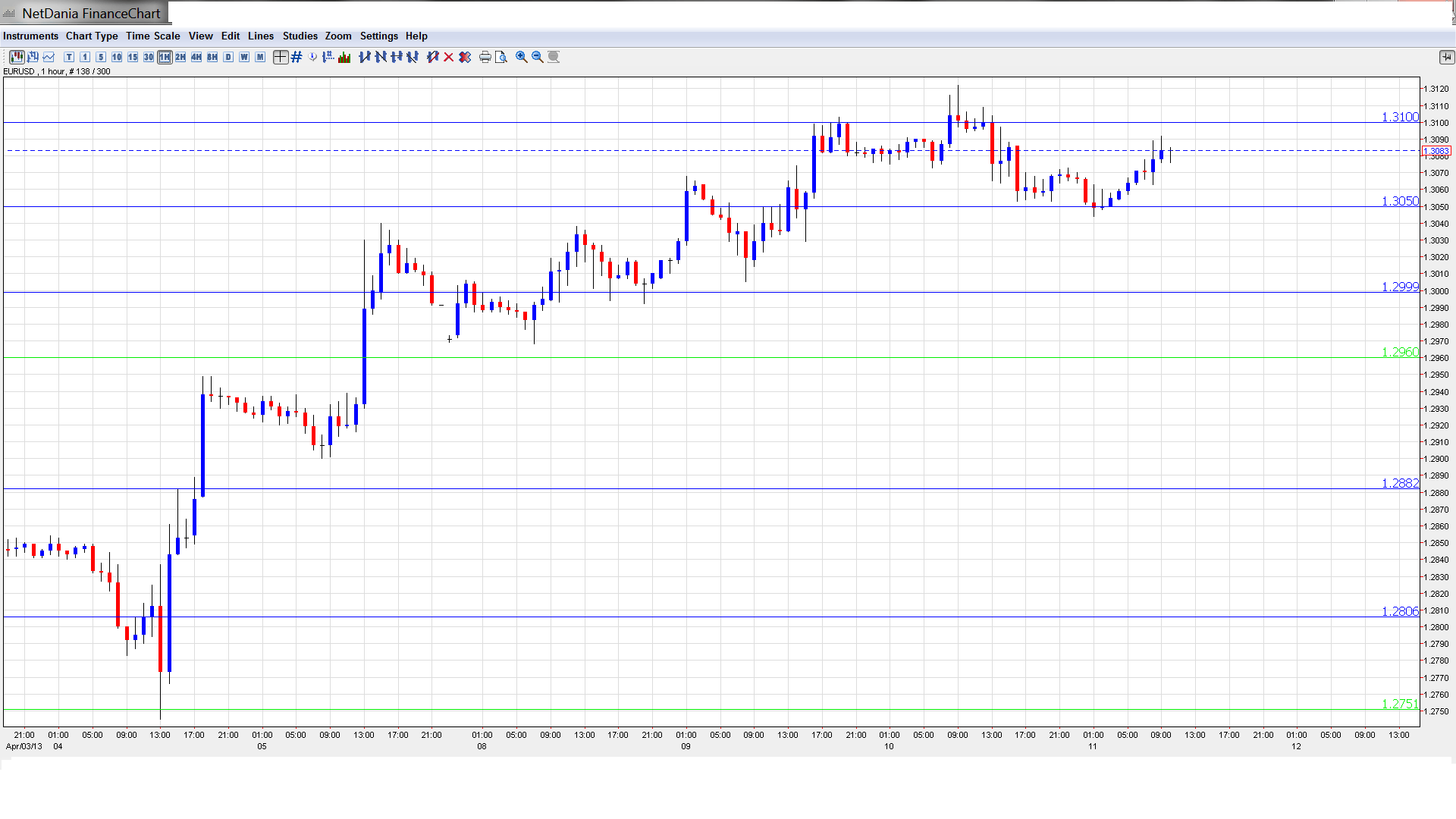

EUR/USD Technical

- Asian session: Euro/dollar was steady, touching a high of 1.3127, and consolidating at 1.3107. In the European session, the pair has lost ground, dropping below the 1.31 line.

- Current range: 1.3050 to 1.3100.

Further levels in both directions:

- Below: 1.3050, 1.30, 1.2960, 1.2880, 1.2805, 1.2750, 1.2660, 1.2624 and 1.2587.

- Above: 1.3100, 1.3130, 1.3170, 1.3290, 1.3350 and 1.34.

- 1.31 is a weak resistance line. 1.3170 is a key level.

- On the downside, 1.3050 is under pressure as the pair loses ground. 1.3000 is stronger.

Euro drops below 1.31 level as US employment numbers improve – click on the graph to enlarge.

EUR/USD Fundamentals

- 6:00 German WPI. Exp. 0.3%. Actual -0.2%.

- 9:00 Eurozone Industrial Protection. Exp. 0.3%.

- All Day: ECOFIN Meetings.

- All Day Eurogroup Meetings.

- 12:30 US Core Retail Sales. Exp. -0.1%.

- 12:30 US PPI. Exp. -0.2%.

- 12:30 US Retail Sales. Exp. 0.0%.

- 12:30 US Core PPI. Exp. 0.2%.

- 12:45 US FOMC Member Eric Rosengren Speaks.

- 13:55 US Preliminary UoM Consumer Sentiment. Exp. 79.1 points.

- 13:55 US Preliminary UoM Inflation Expectations.

- 14:00 US Business Inventories. Exp. 0.4%.

- 16:30 Fed Chairman Bernard Bernanke Speaks.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- US breaks ugly streak: After two straight weeks of key releases which missed their estimates, US numbers finally got on track on Thursday. Unemployment Claims dropped from 385 thousand to 346 thousand. This easily beat the estimate of 354 thousand. The weak numbers had affected a wide range of sectors in the economy, and the markets are hoping that the worst is now behind us. Friday will be a good test, as the US releases four key events. Strong numbers will reassure the markets, but more weak data is sure to raise red flags about the extent of the recovery.

- Eurogroup meeting to discuss bailouts: The markets will be keeping an eye on the Eurogroup finance ministers, who are meeting in Dublin on Friday. Although the Cyprus bailout has grabbed the headlines in recent weeks, other bailouts have been provided to Eurozone members and must be monitored. These include Ireland and Portugal, and the Eurogroup will be discussing whether these two countries should be granted an extension on their loan repayments under their respective bailout agreements. The Cyprus bailout will also be on the agenda, as the Cypriot government has confirmed that the cost of that bailout has ballooned to EUR 23 billion.

- Minutes show Fed split over QE: The FOMC meeting minutes were released earlier in the week, with the most interesting item being the fact that that they were leaked earlier than scheduled on Wednesday. The Federal Reserve has ordered an investigation into the matter. The minutes themselves turned out to be a non-event, with policymakers divided as to the extent and duration of the current round of QE. Some members wanted to wind down the program in mid-2013, while others felt it was more appropriate to wait until the end of the year. There was also discussion about whether to decrease the amount of purchases immediately, or continue the present levels until the end of the year. The division in opinion reflects uncertainty over the extent of the US recovery and the health of the economy. With the US reeling off a host of poor releases throughout April, FOMC members might have had a different take on the QE program had the meeting taken place in April rather than March. Meanwhile QE continues at its present levels of about $85 billion in asset purchases each month.

- German numbers improve: With Eurozone numbers continuing to look weak for the most part, there is a ray of sunshine, as German releases are showing better numbers. Last week, German Factory Orders jumped 2.3%, after a decline the previous month. This easily beating the forecast of 1.2%. The good news continued this week, as German Industrial Production improved by 0.5%, edging past the forecast of 0.4%. On Tuesday, German Trade Balance hit a six month high, posting a surplus of 17.1 billion euros. This was well above the estimate of 16.2 billion euros. If the Eurozone is to turn the corner, it will need Germany, the largest economy in the zone, to lead the way to recovery. Stronger German numbers should lead to better Eurozone readings, which have been anything but impressive so far in 2013.

- Problems in Europe? Tell that to the euro: The Cyprus bailout crisis is not yet behind us, the Eurozone is suffering from a sputtering economy and high unemployment, and even ECB head Mario Draghi toned down his usual optimism at last week’s ECB press conference. Sounds like a recipe for a weaker euro? Evidently not, as the euro continues to look strong against the dollar, having gained about three cents since the beginning of April. The euro received a boost from a long string of weak US numbers, as well as some positive data out of Germany this week. However, the severe problems in the Eurozone will not disappear anytime soon, and a US turnaround would likely put a damper on the euro’s recent rally.