EUR/USD is firm on Thursday, as the pair trades in the high-1.33 range. On the release front, the Eurozone released GDP and inflation data earlier in the day. GDP numbers Germany, France and the Eurozone missed the estimates, while Eurozone inflation indicators matched the forecast. In the US, today’s key event is Unemployment Claims. The markets are expecting the indicator to rise back above the 300 thousand level, with an estimate of 307 thousand.

Here is a quick update on what’s moving the pair.

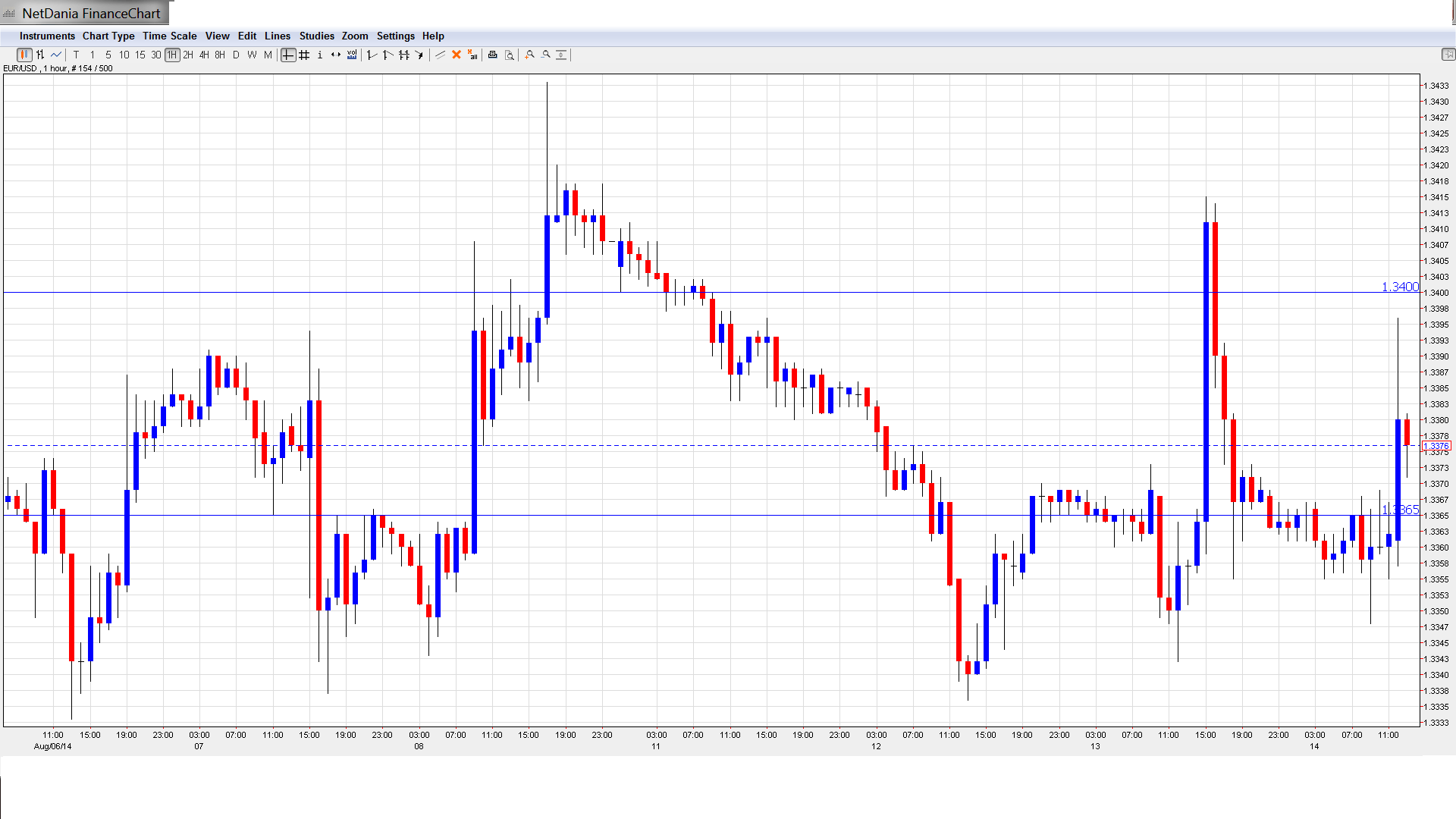

- EUR/USD was uneventful in the Asian session. The pair has posted gains in the European session.

- Current range: 1.3365 to 1.34.

Further levels in both directions:

- Below: 1.3365, 1.3325, 1.3295 and 1.32.

- Above: 1.34, 1.3450, 1.35, 1.3550, 1.3585 and 1.3610.

- 1.3365 has switched to a support role as the euro has gained ground. 1.3295 follows.

- On the upside, 1.34 is under strong pressure. Will the pair break above this barrier? 1.3450 follows.

EUR/USD Fundamentals

- 5:30 French Preliminary GDP. Estimate 0.1%, actual 0.0%.

- 6:00 German Preliminary GDP. Estimate -0.1%. actual -0.2%.

- 6:45 French Preliminary Non-Farm Payrolls. Estimate -0.1%, actual +0.1%.

- 8:00 ECB Monthly Bulletin.

- 9:00 Eurozone Final CPI. Estimate 0.4%., actual 0.4%.

- 9:00 Eurozone Flash GDP. Estimate 0.1%, actual 0.0%.

- 9:00 Eurozone Final Core CPI. Estimate 0.8%, actual 0.8%.

- 12:30 US Unemployment Claims. Estimate 307K.

- 12:30 US Import Prices. Estimate -0.2%.

- 14:30 US Natural Gas Storage. Estimate 81B.

- 17:01 US 30-year Bond Auction.

*All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Eurozone economies unable to generate growth: Despite broad interest rate cuts by the ECB in June, growth and inflation levels have not risen. Economic growth in Germany and France, the two largest economies in the Eurozone, remains listless. French Preliminary GDP remained flat at 0.0%, unchanged from a month earlier. German Preliminary GDP slipped to -0.2%, the first contraction in the German economy since Q4 of 2012. Eurozone Flash GDP also weakened to -0.2%, down from 0.0% in the previous release. All three GDP releases missed their estimates, but surprisingly, the euro moved higher after the GDP releases.

- German, French inflation remains sluggish: The ECB has tried to stave off deflation concerns with interest rate cuts, but inflation levels have not risen. Eurozone Final CPI dipped to 0.4%, down from 0.5% a month earlier. Eurozone Final Core CPI, a minor event, remained unchanged at 0.8%. Both indicators matched the forecast. On Wednesday, German inflation numbers remained weak, while French CPI posted its first decline since January. Deflation could wreak havoc with the limping Eurozone, so the low levels of inflation remain a serious concern.

- Confidence indicators plunge: With the Eurozone in trouble, it shouldn’t come as a surprise that confidence indicators tumbled in July. German ZEW Economic Sentiment plunged to just 8.6 points, down from 27.1 points a month earlier, and its lowest level since November 2012. The estimate stood at 18.2 points. Germany, the largest economy in the Eurozone, continues to sputter. Last week, the country’s trade surplus narrowed and manufacturing numbers missed expectations. With economic indicators pointing downward and confidence in the German economy ebbing, we could see a decline in German GDP on Thursday, which would likely have a chilling effect on the shaky euro. Eurozone ZEW Economic Sentiment followed a similar path to the German release, slipping to 23.7 points, compared to 48.1 points in the previous release. The markets had expected a reading of 41.3 points.

- US jobs data continues to shine: US unemployment indicators are under close scrutiny, as the strength of the labor market is one of the most important factors influencing the Federal Reserve regarding the timing of an interest rate hike. A rate hike is expected by mid-2015, but stronger economic data, especially on the employment front, could hasten a rate move. There was positive news on Tuesday, as JOLTS Job Openings continued to improve in July, although the indicator missed the estimate. The US releases additional job data on Thursday, with the release of Unemployment Claims.

- Geopolitics stable for now: Hotspots in Ukraine and the Middle East remain tense and could have dramatic effects on the markets. The US has accused Russia of massing troops on its border with Ukraine, and tensions are high as the EU has slapped stronger sanctions on Russia, while Moscow has retaliated by banning many food imports from the West. The euro-zone could see food prices going down due to excessive supply. In addition, US president Obama has ordered airstrikes in a remote area of Iraq to prevent ISIL extremists from murdering Yazdi civilians, yet this hasn’t disrupted oil production so far. Things are a bit quieter in Gaza, as a ceasefire between Hamas and Israel has been extended for another five days.