EUR/USD is steady on Thursday, as the pair continues to trade close to nine-month lows. Late in the European session, the pair is trading in the mid-1.33 range. Today’s major event is the ECB rate statement, with the ECB expected to maintain rates at their current level of 0.15%. Elsewhere, German Industrial Production posted a small gain of 0.3%, well below expectations. In the US, the day’s highlight is Unemployment Claims. The markets are expecting a similar reading to the previous release.

Here is a quick update on what’s moving the pair.

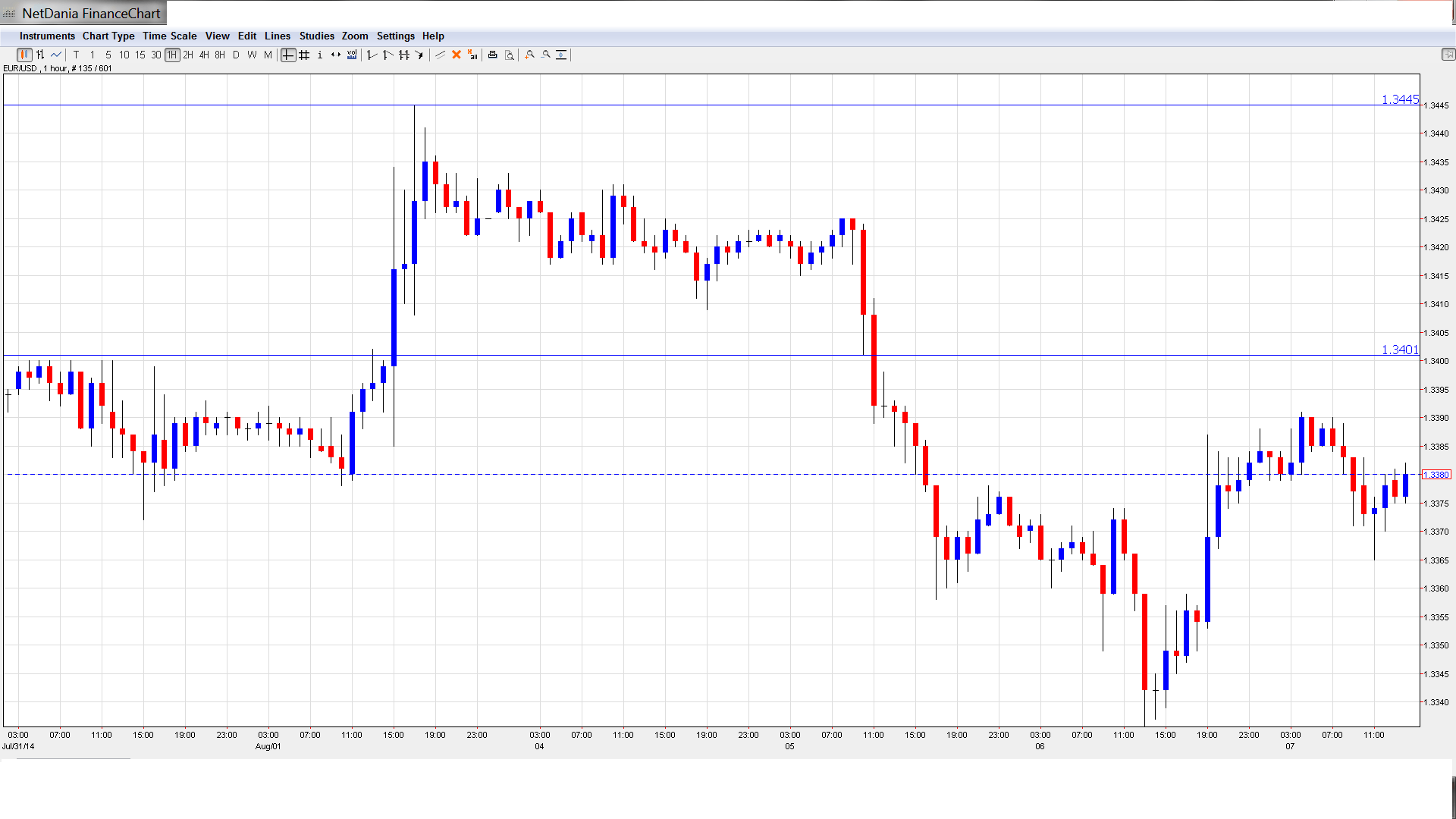

- EUR/USD has showed little movement in the Asian or European sessions.

- Current range: 1.3325 to 1.3400.

Further levels in both directions:

- Below: 1.3325, 1.3295 and 1.32.

- Above: 1.34, 1.3450, 1.35, 1.3550, 1.3585, 1.3610, 1.3650 and 1.3677.

- 1.3325 remains an immediate support line. 1.3295 is next.

- On the upside, 1.34 is under strong pressure. Will the pair break above this key level? 1.3450 follows.

EUR/USD Fundamentals

- 6:00 German Industrial Production. Estimate 1.4%. Actual 0.3%.

- 6:45 French Trade Balance. Estimate -5.0B. Actual -5.4B.

- 8:40 Spanish 10-year Bond Auction. Estimate 2.69%.

- 11:45 ECB Minimum Bid Rate. Estimate 0.15%.

- 12:30 ECB Press Conference.

- 12:30 US Unemployment Claims. Estimate 305K.

- 14:30 US Natural Gas Storage. Estimate 89B.

- 19:00 US Consumer Credit. Estimate 18.3B.

*All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- ECB under pressure as Eurozone sputters: The ECB will be in the spotlight later on Thursday, but the markets are not expecting any dramatic announcements. In June, the ECB cut rates to a record low of 0.15% in order to boost growth and stave off deflation. However, inflation levels have not risen, and continuing tension with Russia over Ukraine has had a negative impact on growth. German numbers have softened and Italy is officially in recession, having posted a decline in GDP for two consecutive quarters. This leaves ECB President Mario Draghi in a difficult position, with few tools in his arsenal to boost the struggling Eurozone economy.

- German manufacturing numbers soften: German data continues to point to trouble in the Eurozone’s largest economy. Industrial Production posted a gain of 0.3%, but this was nowhere close to the forecast of 1.4%. On Tuesday, Factory Production declined by 3.2%, the steepest drop since October 2012. The Bundesbank is blaming tensions with Russia and stronger EU sanctions against Moscow for the weak economic numbers, as Germany is Russia’s number one trading partner in Europe. With key indicators pointing downward and confidence in the German economy ebbing, we could see a decline in GDP in the second quarter, which could have a chilling effect on the shaky euro.

- US Services PMI jumps: On Tuesday, ISM Non-manufacturing PMI looked sharp, rising to 58.7 points last month. This easily beat the estimate of 56.6, and was the index’s best showing since February 2011. This follows a strong Manufacturing PMI reading last week, with the index climbing to 57.1 points, a three-year high. There was more positive news on Tuesday, as Factory Orders had an impressive July, gaining 1.1%. These solid numbers point to healthy expansion in the US manufacturing and services sectors, helping the US dollar post inroads against the euro.

- Low inflation puts pressure on the ECB: Inflation in the euro-zone scratches the bottom, with 0.4% y/y in July. Core inflation is at 0.8%. Despite a weaker euro, prices are not rising in the euro-zone. Will Draghi respond to this? The wide measures introduced in June are still fresh, so action is unlikely, but Draghi could certainly try to talk down the euro to even lower levels.

- US inflation levels remain subdued: Both the Fed favorite Core PCE Price Index as well as Average Hourly Earnings remained low, indicating the Americans don’t have too much money in the their pockets so raising rates to curb demand is not that urgent. The latest FOMC statement did acknowledge that inflation could be closer to target, but expressed concern about the “underutilized” job market.

More: the latest podcast, discussing the ECB: