EUR/USD is steady in Thursday trading, as the markets tread cautiously ahead of today’s US releases. The pair is trading in the mid-1.33 range in the European session as the euro continues the rally which began at the end of May. In the Eurozone, today’s only data was German WPI, which disappointed the markets with is third consecutive decline. The US will release a host of events later, including three key releases – Retail Sales, Core Retail Sales and Unemployment Claims. So it could be a busy day for EUR/USD.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

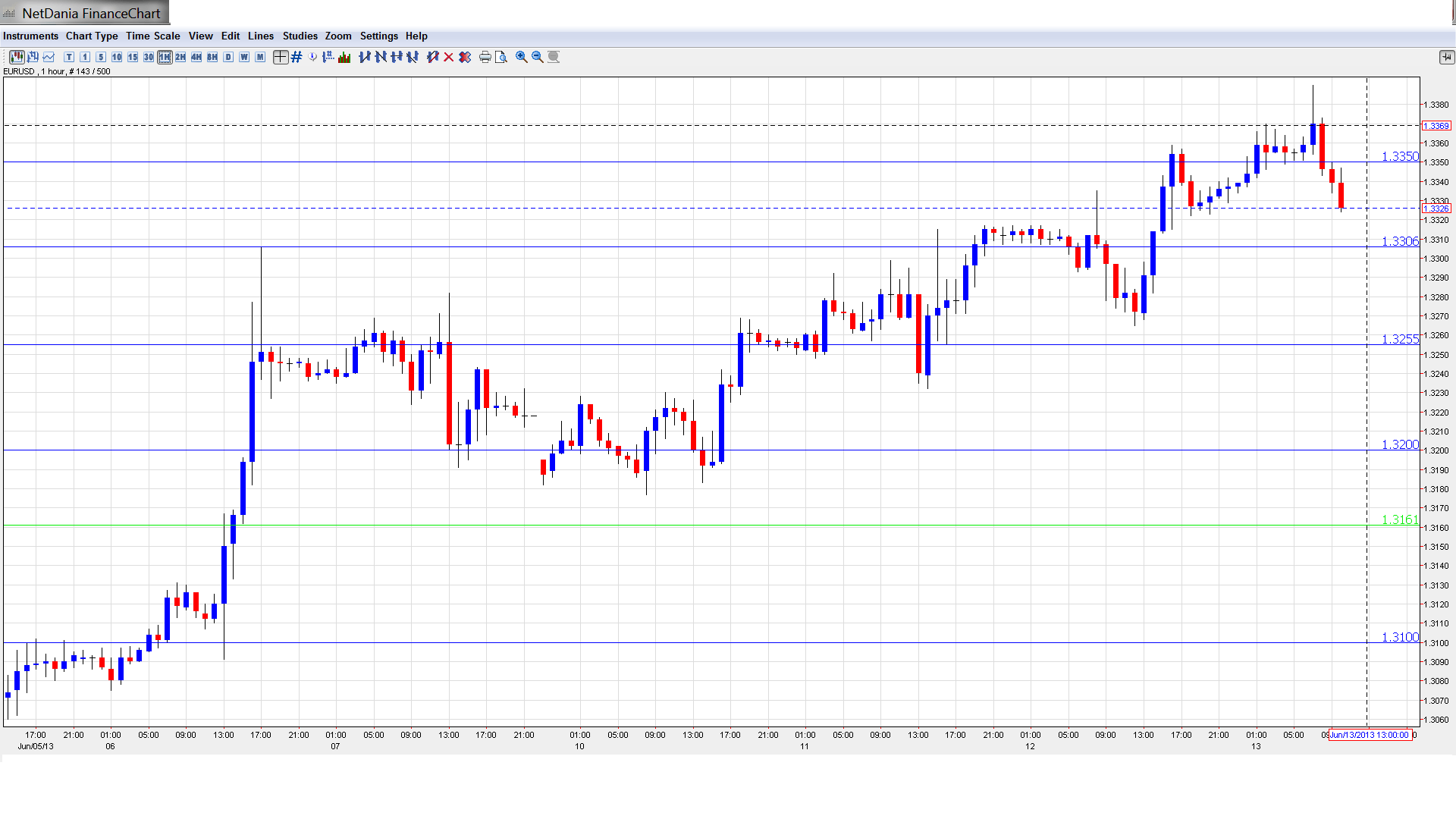

EUR/USD Technical

Asian session: Euro/dollar pushed higher, and touched a high of 1.3388. The pair then retracted and consolidated at 1.3359. Euro/dollar has edged lower in the European session.

Current range: 1.3306 – 1.3350.

Further levels in both directions:

<img alt=”EUR USD Daily Forecast June 11″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-11-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast June 10th” src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-10th-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast June 7″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-7-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast June 6″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-6-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast June 4″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/06/EUR-USD-Daily-Forecast-June-4-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May31″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May31-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May30″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May30-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May29″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May29-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May28″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May28-350×196.png” width=”350″ height=”196″ /> <img alt=”EUR USD Daily Forecast May27″ src=”https://www.forexcrunch.com/wp-content/uploads/2013/05/EUR-USD-Daily-Forecast-May271-350×196.png” width=”350″ height=”196″ />

Below: 1.3306, 1.3255, 1.32, 1.3160, 1.31, 1.3050, 1.30, 1.2940, 1.2890, 1.2840, 1.28, 1.2750 and 1.27.

Above: 1.3350, 1.34, 1.3480, 1.3580 and 1.3710.

1.3306 is providing weak support. This is followed by 1.3255. On the upside, the pair is testing 1.3350. The round number of 1.34 is next.

Euro edges higher ahead of US releases – click on the graph to enlarge.

EUR/USD Fundamentals

6:00 German WPI. Exp. -0.2%. Actual -0.4%.

8:00 ECB Monthly Bulletin.

12:30 US Core Retail Sales. Exp. 0.3%. 12:30 US Retail Sales. Exp. 0.4%. 12:30 US Unemployment Claims. Exp. 354K. 12:30 US Import Prices. Exp. 0.0%.

14:00 US Business Inventories. Exp. 0.3%.

14:30 US Natural Gas Storage. Exp. 96B.

17:00 US 30-year Bond Auction.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

Markets Await Major US releases: This week has been a bit of a yawner as far as US releases, but that will change on Thursday, as the US releases its first key numbers of the week. The markets will get a look at retail sales and unemployment data, so EUR/USD could see some action later today. If the releases meet or beat market expectations, we will likely see more speculation as to whether the Fed will taper with the current QE scheme, which stands at $85 billion in asset purchases each month.German Court Reviews OMT: On Wednesday, the German Constitutional Court wrapped up a hearing on the ECB’s OMT (Outright Monetary Transactions) program. OMT is a rescue program which enables the ECB to buy bonds from Eurozone members whose economies are struggling. It’s turned into a case between the ECB and the German Bundesbank, as the ECB board member Joerg Asmussen defended the program in front of the court, while Jens Weidmann, head of the Bundesbank, attacked the OMT. It should be noted that the ECB has never purchased any bonds under the scheme. What can we expect from the Court? In previous cases involving the legality of ECB rescue packages, the German court has given its approval, but has not hesitated to add conditions . So we can expect the court to give the nod to OMT, although there could some strings attached. A ruling in the matter is not expected until September, after German elections.IMF admits mistakes in Greek bailout: In an interesting development, the IMF admitted mishandling the Greek bailout program, in which Greece received 240 billion euros. The IMF said it failed to deal with private debt restructuring properly and overestimated the capacity of Greek governments to push through tough economic reforms. The IMF also pointed fingers at the EU for “notable mistakes”. For its part, Greece said that the IMF report would not lead to any changes as the country continues to work towards meeting its deficit reduction targets under the bailout program.US earns upgrade from S&P: The S&P ratings agency revised its US rating from negative to stable, which means that another downgrade in the next two years has less than a 33% chance of occurring . The agency said that a key factor in its decision was the agreement reached in Congress to avoid the fiscal cliff, which would have resulted in $600 billion in tax increases and spending cuts, and could have pushed the US economy into recession. Back in 2011, S&P cut the US credit rating from AAA to AA, and the threat of another downgrade has been hanging over the markets since then. So this development will improve market sentiment and could give a boost to the US dollar. The S&P decision could also affect the US Federal Reserve’s QE program. The Fed has said that it won’t wind up the program before it sees a stronger recovery and an improved labor market. Although US releases have been a mixed bag, speculation is rising that the Fed could take action in the next few months. With QE being dollar-negative, any tapering of QE could give a boost to the greenback against the other major currencies.