EUR/USD has lost ground on Tuesday, as the pair trades below the 1.35 line in the European session. The euro remains under pressure, as there is increasing speculation that the ECB could lower interest rates at its meeting on Thursday in order to boost the struggling Eurozone. Taking a look at economic releases, Spanish Unemployment soared in September and Eurozone PPI missed the estimate. Over in the US, today’s highlight is ISM Non-Manufacturing PMI.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

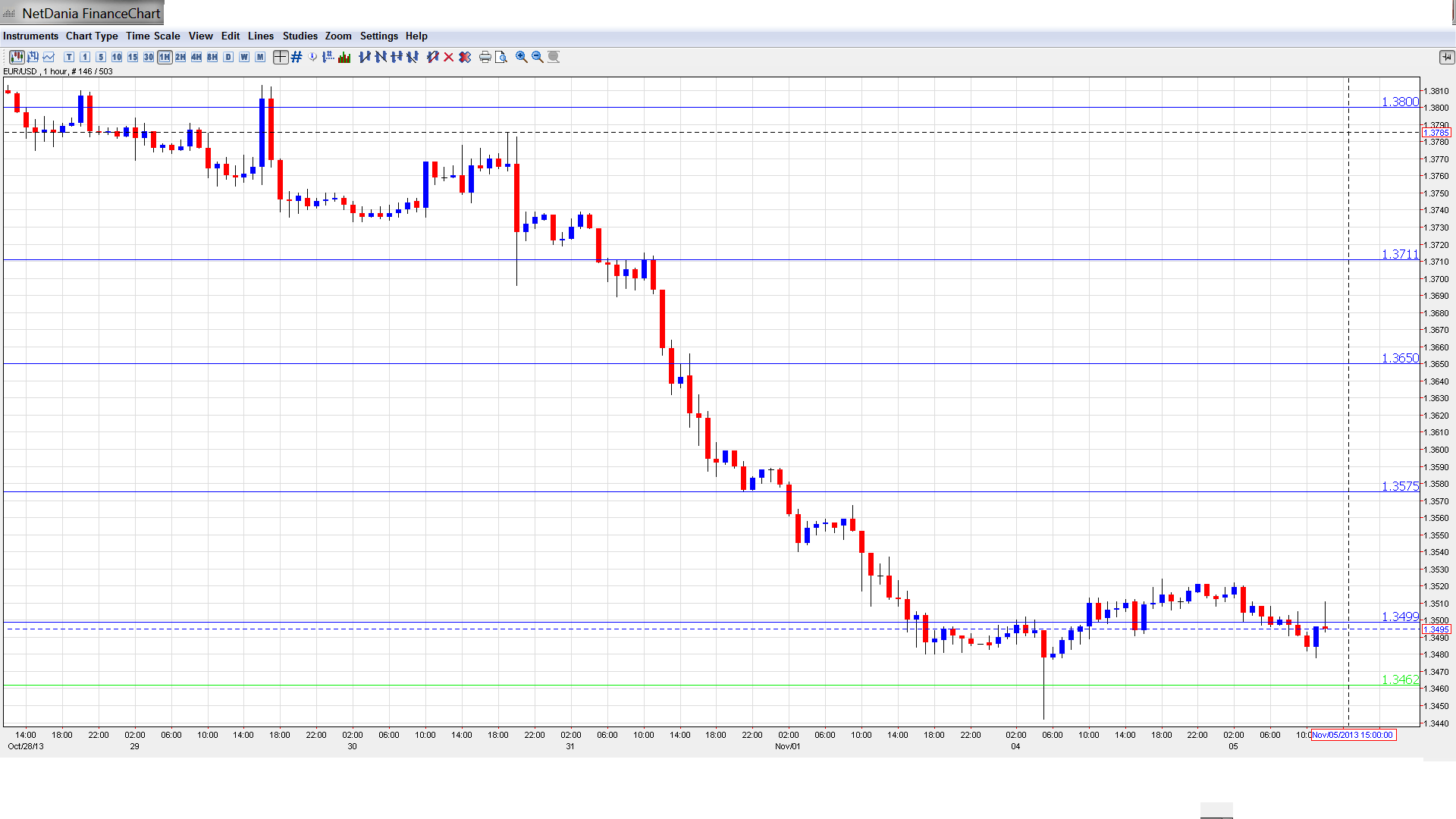

EUR/USD Technical

- In the Asian session, EUR/USD traded close to the 1.35 line, dipping to a low of 1.3491 late in the session, before consolidating at 1.3492. The pair has edged higher in the European session, crossing above the 1.35 line.

- Current range: 1.3500 to 1.3570.

Further levels in both directions:

- Below: 1.3500, 1.3460, 1.3415, 1.3325 and 1.3240, 1.3175, 1.31, 1.3050 and 1.3000.

- Above: 1.3570, 1.3650, 1.3710, 1.3800, 1.3870 and 1.3940.

- On the downside, 1.3500 remains fluid. 1.3460 is next.

- 1.3570 is the next resistance line. It is followed by 1.3650.

EUR/USD Fundamentals

- 8:00 Spanish Unemployment Change. Exp. 31.3K, Actual 87.0K.

- 9:30 EU Economic Forecasts.

- 10:00 Eurozone PPI. Exp. 0.3%, Actual 0.1%.

- 15:00 US ISM Non-Manufacturing PMI. Exp. 54.2 points. See

how to trade this event with USD/JPY. - 15:00 US IBD/TIPP Economic Optimism. Exp. 41.1 points.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Eurozone inflation remains subdued: Inflation indicators in the Eurozone continue to point to very weak inflation, which in turn signals sluggish economic activity. Eurozone CPI dropped to 0.7% in October, compared to 1.1% the month before. Eurozone PPI posted a paltry gain of 0.1%, shy of the estimate of 0.3%. These figures are well below the ECB’s inflation target of 2.0%. Speculation is growing that the ECB could cut rates in order to boost growth, perhaps as early as this week, when the ECB holds a policy meeting . The argument against cutting interest rates is that with rates already at a record low of 0.50%, a cut of 0.25% might not have much impact. Other tools available to the ECB include a new LTRO or introducing a negative deposit rate. With all this uncertainty in the air, we could see some volatility from the euro during the week.

- US numbers improve late in the week: After a host of weak numbers early in the week, US numbers showed some improvement. Unemployment Claims practically matched the forecast, and ISM Manufacturing PMI beat the estimate. With the Fed unlikely to taper QE before 2014, the QE uncertainty which was has been weighing on the dollar has eased, and the dollar could continue to hammer away at the retreating euro.

- Fed keeps QE tap open: Last week’s Federal Reserve policy meeting was the first meeting since Congress hammered out an agreement on the debt ceiling and reopened the government. As expected, the Fed said that it would maintain QE at current levels of $85 billion each month. However, the policy statement was less dovish than expected, as the Fed said that the economy was expanding “at a moderate pace” and left the door open for tapering in December. However, most markets analysts are of the view that short of a sharp improvement in US data, QE tapering will be on hold until early 2014.

- Weak German numbers point to slowdown: German releases did not look sharp last week. On Thursday, Retail Sales posted its third decline in four releases, and Consumer Climate and Import Prices both fell short of their estimates. Earlier this week, German Unemployment Change came in at 2 thousand in September, just above the estimate of 1 thousand. Although this was a respectable reading, it was the indicator’s third consecutive increase, raising concerns that the German economy is slowing down. The jobless rate was unchanged at 6.9 percent. If the Eurozone is to remain out of recession, it can ill afford for Germany, the region’s number one economy, to slow down.