The markets welcomed in a new month on Monday, but so far the EUR/USD has picked up where it left off on Friday, showing little movement. The pair is trading in the low-1.32 range in the European session on Monday. On Friday, UoM Consumer Sentiment fell, but still beat the estimate. The markets have settled down as a US military strike against Syria has been put on hold. There are no US releases on Monday, as the US markets are closed for the Labor Day holiday. In the Eurozone, the new week started well as Manufacturing PMIs out of Spain, Italy and the Eurozone all beat the estimates.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

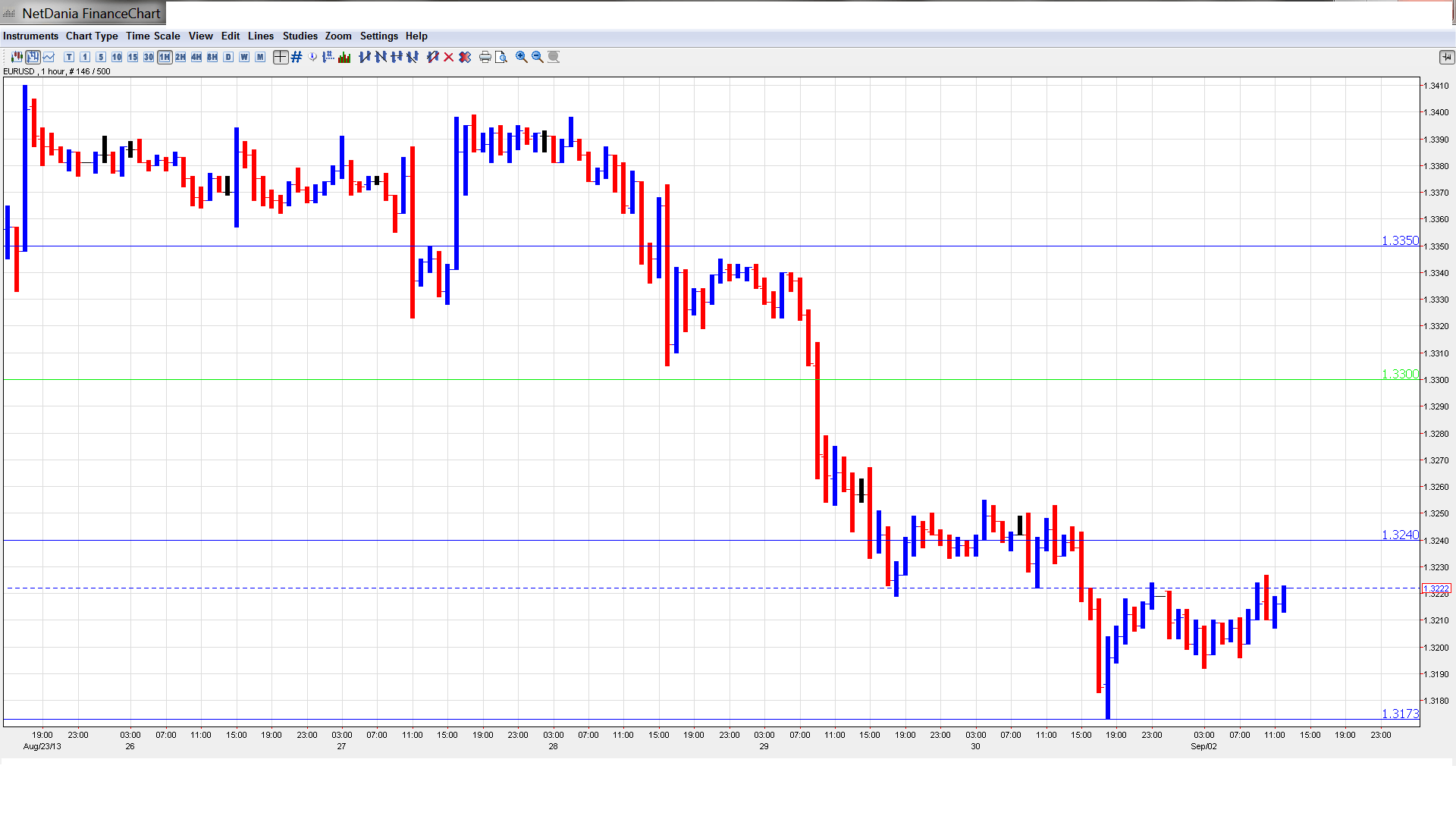

EUR/USD Technical

- In the Asian session, EUR/USD was very quiet, touching a high of 1.3222 line and consolidating at 1.3221. The pair is unchanged in the European session.

Current range: 1.3175 to 1.3240.

Further levels in both directions:

- Below: 1.3175, 1.31, 1.3050 and 1.30.

- Above: 1.3240, 1.33, 1.3350, 1.3415, 1.3450, 1.3520, 1.3590 and 1.37.

- 1.3240 has reverted to a resistance role. The round number of 1.33 is next.

- 1.3175 is providing weak support. 1.31 is stronger.

EUR/USD Fundamentals

- 7:15 Spanish Manufacturing PMI. Exp. 51.1, actual 50.1 points.

- 7:45 Italian Manufacturing PMI. Exp. 50.7, actual 51.3 points.

- 8:00 Eurozone Manufacturing PMI. Exp. 51.3, actual 51.4 points.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Euro steadies as Syrian tensions subsides: The markets were nervous last week in anticipation of an expected US military strike against Syria, after a chemical attack in the war-torn country killed hundreds of civilians. The euro dropped sharply, losing about 170 points on the week. However, the attempt by the US to secure a coalition ran into trouble, and President Obama said on the weekend that he will seek Congressional approval before taking any action against Syria. With Congress in recess until September 9th, a military strike could be delayed until mid-September or even later. As a result, the markets have settled down and the euro has started the week quietly.

- Solid PMIs out of Eurozone: With the US markets closed on Monday, the focus is on Eurozone releases. The news was all positive as Manufacturing PMIs from Italy, Spain and the Eurozone beat the estimates. All three PMIs posted readings above the 50-point level, which indicates expansion. Eurozone Manufacturing PMI had a long run of releases below the 50 level, but has now stayed above the 50 line for two consecutive readings. Further solid data out of the Eurozone is essential for the euro to recover after sustaining sharp losses against the dollar last week.

- German data a concern: German data continues to look weak. On Thursday, Unemployment Change jumped from -7 thousand in July to 7 thousand in August. The markets had expected another decline of -5K. Friday brought no relief as Retail Sales declined 1.4%, well off the estimate of a 0.5% gain. National elections are just a few weeks away, and domestic economic problems could hurt Chancellor Angela Merkel, who is seeking a third straight term in office.

- QE tapering in September?: The Federal Reserve has kept very quiet about when it might taper QE, and recent statements from Fed policymakers underscore divisions regarding the timing of such a dramatic move. What is clear is that stronger US numbers will increase the likelihood of the Fed acting sooner rather than later. This means that US releases, especially employment numbers, will be under the market microscope and traders should be prepared for QE tapering, which will likely boost the US dollar against other major currencies.