GBP/USD dropped to the lowest levels since the flash crash, but the Donald Disappointment already helped it recover. What’s next?

Here is their view, courtesy of eFXnews:

We see the path for the British Pound as a function of two things.

First, there is the question of where GBP/$ would trade in the event of a “hard Brexit.” We have used several approaches to show that Sterling could fall between 20-40 percent relative to pre-referendum levels, with a low of 1.10 for GBP/$ quite possible.

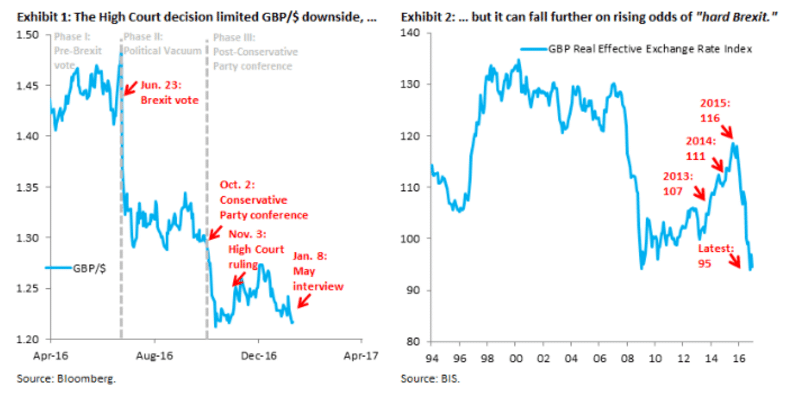

Second, what probability should markets assign to “hard Brexit.” In our minds, it has been this probability that has been moving the Pound around since June of last year. In particular, the political vacuum following the referendum meant that there was some probability that Article 50 might never be triggered. In the presence of large speculative shorts, this kept the Pound supported after its initial referendum fall. But the Conservative party conference changed that, with Prime Minster May committing to trigger Article 50 by March. We thought the market would price a greater probability of “hard Brexit” as a result, reiterating our near-term target of 1.20 for Cable in the days ahead of the ‘flash crash’. The November High Court decision was a move back in the opposite direction, reducing in the market’s eyes the odds that Article 50 could be triggered by March and, more fundamentally, limiting how aggressive the government could be in its negotiating position. This buoyed Cable, pushing it back up towards 1.28 and pre-‘flash crash’ levels in mid-December (Exhibit 1). However, our underlying conviction is that Sterling needs to weaken quite a bit more, given that the trade-weighted decline is only 13 percent so far (Exhibit 2), well shy of our 20-40 percent range.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.

We think the most recent decline, sparked by Prime Minister May’s latest speech re-affirming her Brexit vision, is the start of that process, with the FX market only beginning to re-engage in the idiosyncratic Sterling down story.

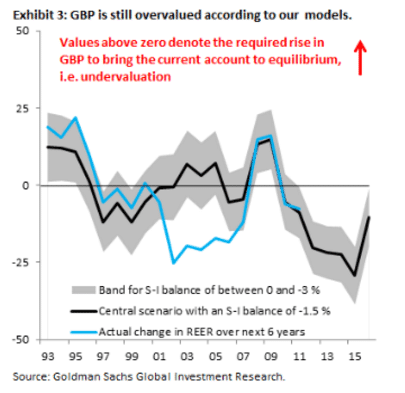

Our 3-, 6- and 12-month forecasts for GBP/$ now stand at 1.20, 1.18 and 1.14, respectively, with risks tilted in the direction of a sharper, more front-loaded decline. Our conviction for this forecast rests on the fact that the fall in GBP is still relatively small in trade-weighted terms, something that has been overlooked, while we also think the market continues to under-price Prime Minister May’s commitment to trigger Article 50 by March. Taking into account that the Pound has fallen 13 percent from pre-Brexit vote levels, this is still well short of the upper bound of our range between 20-40 percent that we derive using various approaches (Exhibit 3).

We continue to think that – even with the decline since June – the Pound is not yet cheap and that more declines are coming. We remain short Sterling also in our Top Trade for 2017, where we are short GBP and EUR equally weighted against the Dollar.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.