Idea of the Day

The dollar is only marginally firmer compared to the middle of December when the Fed announced the start of tapering. This is because it was done in a cautious manner, but also because the Fed chose to further soften its forward guidance, reassuring markets that rate hikes were not around the corner. This contrasts to the non-tapering of September last year, when the Fed did not taper in part because the market was becoming too nervous of potential rate hikes to come. Given this balance, the minutes to the December FOMC meeting released later today will be a key focus for markets to determine the conditions that will see the Fed continue with the tapering move. The data is suggesting that Q4 is going to be strong when initial numbers are released later this month, which could prompt further tapering at the end of January meeting.

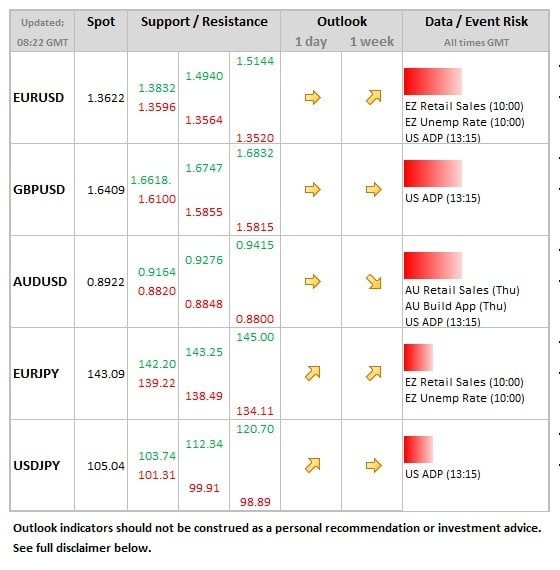

Data/Event Risks

USD: The minutes to the December Fed meeting will be scrutinised more than usual given that this was the meeting when tapering of asset purchases was started and the language on the unemployment threshold was softened. The dollar will be looking for hints on the triggers and pace of future tapering.

EUR: Retail sales and unemployment data are released for the Eurozone, but impact on the euro likely to be limited as it is the inflation backdrop that is the focus going into tomorrow’s policy meeting.

Latest FX News

EUR: Despite the fall in core inflation yesterday, the euro was on pretty good form. The overhang of liquidity in place over the year end fell thanks to the latest ECB operations, so putting some upward pressure on money market rates and also the single currency. This is counteracted by expectation of hints of further easing to come at tomorrow’s policy meeting.

AUD: Tight within the 0.8900 to 0.8950 range for the time being, with no key domestic data this week (retail sales and building approvals tomorrow) and no further noises from the RBA on their desire to see a weaker currency.

JPY: The yen breaking above the 105.00 level during Asia trade. The high seen in December of 105.44 will remain the initial focus for dollar bulls.

Gold: Taking a break after the strong start to the year, but only modestly so and the lows seen in mid-December look safe for the time being. The main challenge will remain a stronger dollar in the face of further Fed tapering.

Further reading: