The price of oil continues recovering. WTI Crude Oil took another leg up in the wake of the new week, reaching $48.67, the highest in two weeks. Energy ministers from Saudi Arabia and Russia met and announced a planned extension.

Saudi Arabia is the largest producer in the world and the de-facto leader of OPEC. Russia is the largest producer in the group of non-OPEC that have signed up to a production cut in November 2016. The six-month deal reaches its end in the middle of the year. This announcement, while not finalized, extends the cuts by the same targets by nine months, a longer period of time.

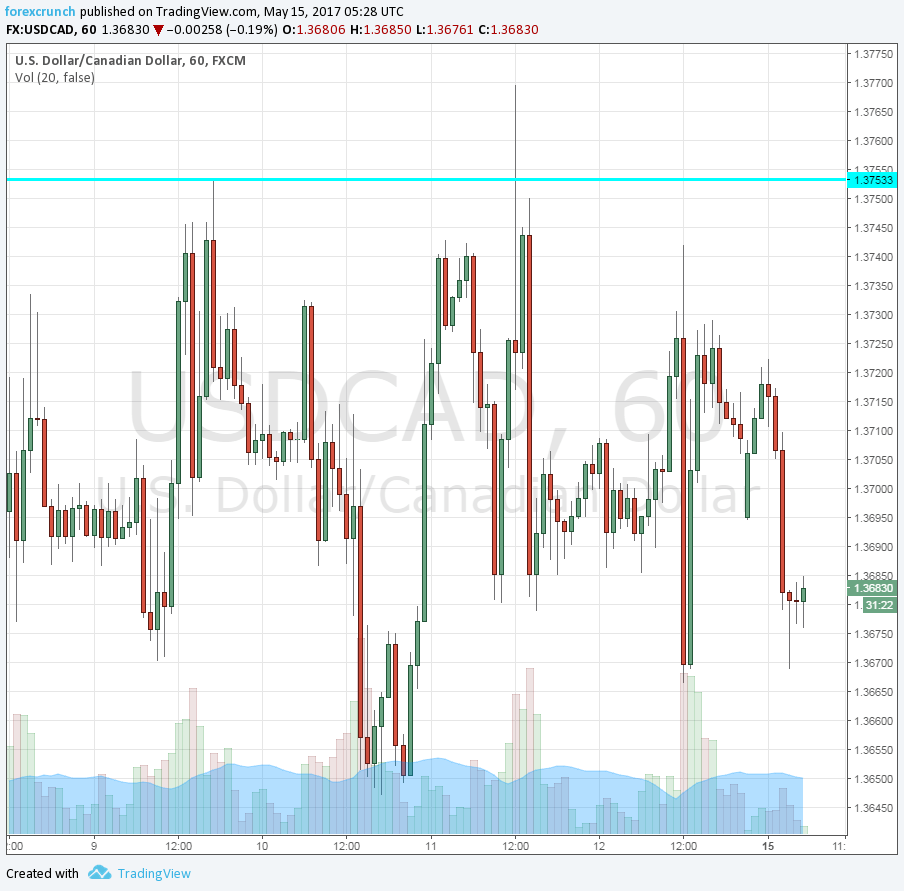

USD/CAD far from the highs

The Canadian dollar suffered when prices collapsed two weeks ago. WTI quickly fell below the triple-bottom level of $47 and dipped under $44. Dollar/CAD jumped and almost touched 1.38, the highest since early 2016.

And after oil prices stabilized, so did the loonie. USD/CAD is currently trading around 1.3677. All in all, the pair trades in a band ranging from 1.3638 and 1.3760. In any case, the pair is shy of the highs.

Will oil continue higher?

There are reasons to doubt the recent rises in oil prices, the same reasons that were always evident. When looking into OPEC, the vast majority of cuts come from Saudi Arabia. The rest are piggy-backing on the large exporter. Is this sustainable?

The bigger problem for oil bulls is as always the shale production in the US. New extracting technologies pushed prices lower in 2014 and continue to swing with the ebb and flow of prices. When prices collapsed, US production eventually dropped. But when the OPEC / non-OPEC deal kicked in, output was on the rise once again.

US petroleum output is around 9.3 million barrels per day, above the 8.7 trough but still below the 9.6 mbpd peak. So, there may be a way to go in output, resulting in lower prices for the black gold.

More: USD/CAD has many things going for it [Video]

Here is the Dollar/CAD hourly chart: