EUR/USD is screaming higher after stronger than expected inflation numbers. CPI is at 0.8% and core CPI at 1%. Strong German numbers gave the euro early support, but reports about a Russian invasion of the Crimea peninsula weigh. As implications for the ECB decision are digested, the focus moves again to the US with the second estimate of GDP and other important indicators. A strong end to the week and month are awaited.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

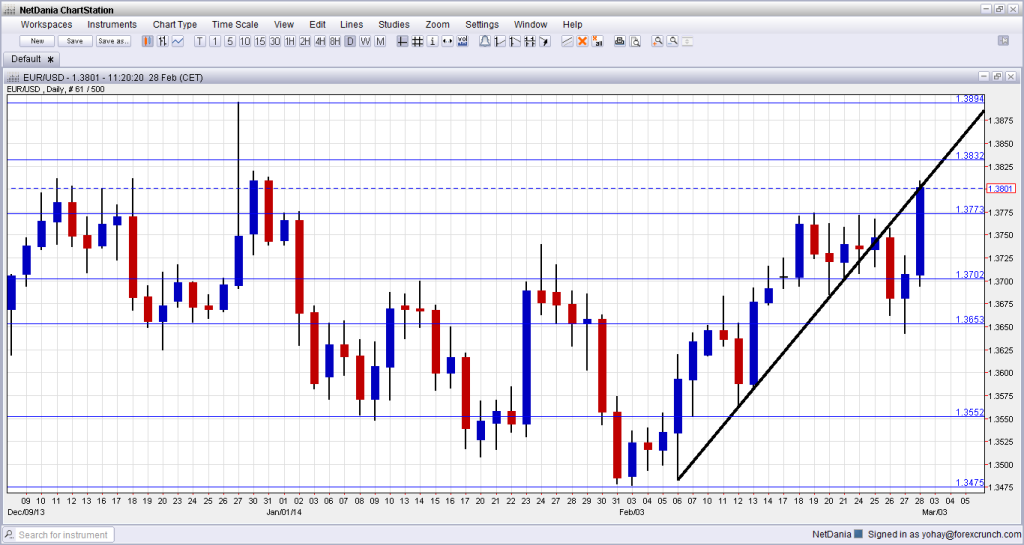

EUR/USD Technical

- EUR/USD remained stable on high ground after rising in the previous US session.

Current range: 1.38 to 1.3832.

Further levels in both directions:

- Below: 1.3773, 1.37, 1.3650, 1.3580, 1.3515, 1.3450 and 1.34

- Above: 1.3830, 1.3895, 13915 and 1.40 and 1.4214.

- 1,3830 is strong resistance.

- The previous double top of 1.3773 turns to support.

EUR/USD Fundamentals

- 7:00 German Retail Sales. Exp. +1.2%, actual +2.5%.

- 7:45 French Consumer Spending. Exp. -0.8%. Actual -2.1%.

- 9:00 Italian unemployment rate. Exp. 12.7%, actual 12.9%.

- 10:00 Euro-zone CPI Flash Estimate. Exp. +0.7%. Actual +0.8%. Core CPI +1%. Big euro rally.

- 10:00 Euro-zone unemployment rate. Exp. 12%.

- 10:00 Italian CPI. Exp. +0.5%.

- 10:00 FOMC member Richard Fisher talks.

- 13:30 US GDP (second estimate). Exp. +2.6%.

- 14:45 US Chicago PMI. Exp. 57.9 points.

- 14:55 US UoM Consumer Sentiment. Exp. 57.9 points.

- 15:00 US Pending home sales. Exp. 2.9%.

- 15:15 US FOMC members Narayana Kocherlakota and Jeremy Stein talk.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Breathing room for the ECB: The big surprise seems to have shelved plans for a negative deposit rate. With core inflation at 1%, Draghi can fend off criticism. ECB Governing Council member Ignazio Visco said that a negative deposit rate is on the agenda in the upcoming March meeting (currently the rate is at 0%). While the ECB may not take action, this comment certainly weighed on the euro. It joins similar sentiments out of the ECB and some complaints about the euro’s strength from the head of the Eurogroup.

- Russian invasion of the Ukraine?: There are reports that the Russian army captured airports in the Crimea peninsula. This lifts tensions once again, after things have already seemed to have calmed. There are reports of long lines to withdraw money in the Ukraine, and foreign reserves are running low. The Ukrainian Hryvna (UAH) has dropped in value, with USD/UAH almost reaching 10 and EUR/UAH around 13.60. The Ukraine has a lot of outstanding debt and a default could have serious contagion effects. Russian gas flows through the Ukraine to central Europe. So, events in this country are certainly relevant for the euro-zone and they already caused a loss of uptrend support.

- Germany leading the pack: German retail sales rose by 2.5%, calming fears seen in the previous months. The number of unemployed in the euro-zone’s locomotive also fell more than expected and this joins the strong German GfK Consumer Confidence that reached 8.5 points, its highest level since January 2007. and the upbeat German Ifo Business Climate, which also posted a multi-year high. Germany is certainly doing well, but others are lagging behind.

- US data improves: A nasty streak of weak US releases ended on Wednesday as New Home Sales jumped by 468 thousand much better than expected. Another positive figure came from durable goods orders, and especially the core numbers. The focus is now on GDP, which is expected to be revised to the downside, from 3.2% to 2.6%.

- Federal Reserve may adjust forward guidance: Janet Yellen acknowledged the slowdown in the US economy but did not hint about any change in QE tapering. However, forward guidance could certainly be adjusted if the unemployment rate continues falling. The meeting minutes indicated that interest rates are unlikely to rise, even if unemployment drops to 6.5%.

More: Euro-zone inflation: a look to February 2013 can explain the surprise