EUR/USD is steady, as the pair was trading in the mid-1.35 range. In the US, the GDP release looked awful, posting its first decline since 2009. The Federal Reserve wrapped up its policy meeting, and said that QE3 would continue. Thursday is another busy day, with a host of economic releases. In Germany, Retail Sales declined, but the Unemployment Change was very sharp. Today’s key release is US Unemployment Claims.

EUR/USD Technical

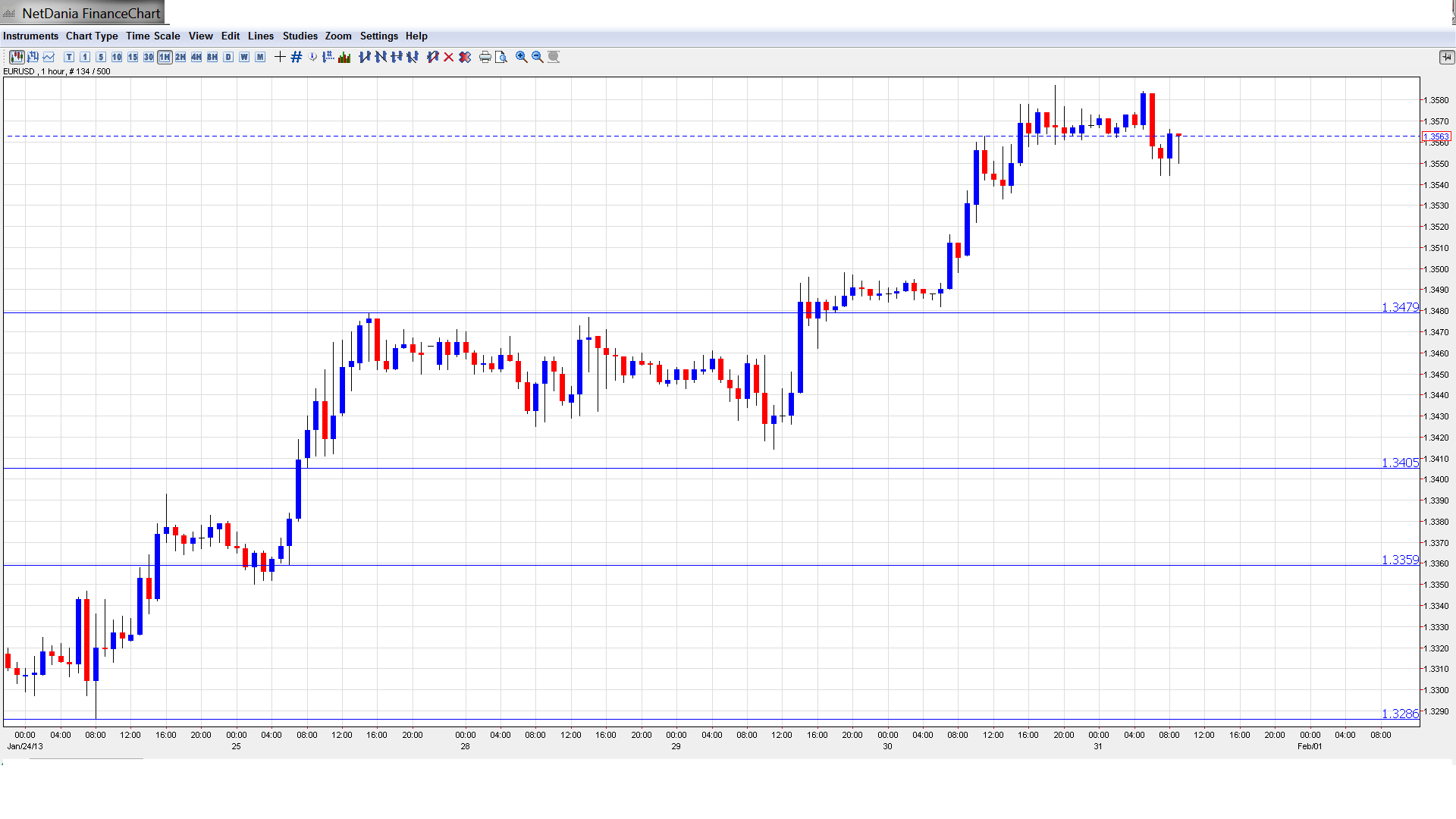

- Asian session: Euro/dollar was quiet, reaching a high of 1.3585. The pair consolidated at 1.3555. The pair is unchanged in the European session.

- Current range: 1.3480 to 1.36.

Further levels in both directions:

- Below: 1.3480, 1.34, 1.3360, 1.3290, 1.3255, 1.3170, 1.3130, 1.3110, 1,3030, and 1.30.

- Above: 1.36, 1.3690, 1.3750 and 1.3838.

- 1.3480 has strengthened in support.

- On the upside, 1.36 is providing resistance.

Euro/dollar steady after weak US data – click on the graph to enlarge.

EUR/USD Fundamentals

- 7:00 German Retail Sales. Exp. 0.1%. Actual -1.7%.

- All Day: German Preliminary CPI. Exp. -0.5%

- 7:45 French Consumer Spending. Exp. 0.3%. Actual 0.0%.

- 8:55 German Unemployment Change. Exp. 9K. Actual -16K.

- 12:30 US Challenger Job Cuts.

- 13:30 US Unemployment Claims. Exp. 362K.

- 13:30 US Core PCE Price Index. Exp. 0.1%.

- 13:30 US Employment Cost Index. Exp. 0.6%.

- 13:30 US Personal Spending. Exp. 0.4%.

- 13:30 US Personal Income. Exp. 0.7%.

- 14:45 US Chicago PMI. Exp. 51.1 points.

- 15:30 US Natural Gas Storage. Exp. -202B.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- No surprises from Fed: All eyes were on the Federal Reserve this week, as the powerful US central bank met for a two-day policy meeting. There were no surprise developments, as the Fed stated it would continue its open-ended QE3 program until the outlook for the labor market “improves substantially”. This put to rest any doubts that the current round of QE, under which the Fed is purchasing $85 billion a month in securities, might be terminated anytime soon. The Fed maintained its ultra-low benchmark interest rate, saying there would be no change until unemployment drops below 6.5%. With US unemployment close to 8%, we will likely be hearing this refrain for the foreseeable future.

- Euro sparkles: The euro continues to fly high, and has climbed above the 1.35 line, its highest level since December 2011. EUR/USD has now jumped almost 500 points since early January. The continental currency has been bolstered by improving German data, as well as optimistic forecasts about the Eurozone economy from ECB President Mario Draghi and others. These officials acknowledge that the Eurozone is going through a tough time, but are confident that the economy will bounce back later in 2013. Although a range of indicators, notably employment and PMI numbers, point to a deepening recession and continuing fallout from the debt crisis, the euro is enjoying the ride, at least for now.

- German Data Mixed: The German locomotive will have to get back on track if the Eurozone is to get back on its feet in 2013. So how is the German economy doing? The answer seems to be lukewarm, based on recent data. Business Sentiment has improved, and unemployment numbers were excellent. At the same time, inflation indicators have been in negative territory, pointing to subdued economic activity. The manufacturing sector is struggling, and Retail Sales fell by 1.7%, well below the estimate. The markets are well aware that as goes Germany, so goes Europe, and will be hoping for better news from the bloc’s largest economy.

- Markets fret over weak US housing numbers Although the US has posted been able to point to some strong releases recently, recent housing numbers have been in the tank. New Home Sales was a disappointment, falling well below the estimate. Pending Home Sales fared no better, plunging by 4.3%. This was the key indicator’s worst showing since last May. These dismal readings points to weakness in the US housing industry, a critical component for economic growth. The bumpy US recovery will continue to limp along if these numbers don’t improve soon.

- US recovery continues to hit bumps: The extent of the US recovery is anyone’s guess, as US numbers continue to keep the markets guessing. Employment and retail sales numbers have been very positive, but this has been offset by weak housing and consumer confidence data. This week’s GDP reading was abysmal, as the US economy declined by 0.1%. Although a very modest loss, there is bound to be negative market reaction, as this was the first decline since 2009, and the markets had anticipated a 1.1% gain. The US will be releasing key employment numbers on Thursday and Friday, and the markets will be hoping that the US employment picture continues to brighten.