EUR/USD dropped sharply in Monday’s Asian session, following the announcement that a 10 billion euro bailout for Cyprus would include a one-time tax on bank deposits. The euro plunged almost two cents on the news, and dipped below the 1.29 line. The pair has recovered some of these losses in European session, and was trading in the mid-1.29 range. On Friday, US manufacturing and consumer confidence numbers fell well below expectations. There are just three releases out of Europe and the US to kick off the trading week. Italy posted a Trade Deficit for the first time in five months, disappointing the markets. The Eurozone Trade Surplus narrowed, and came in well below the forecast.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

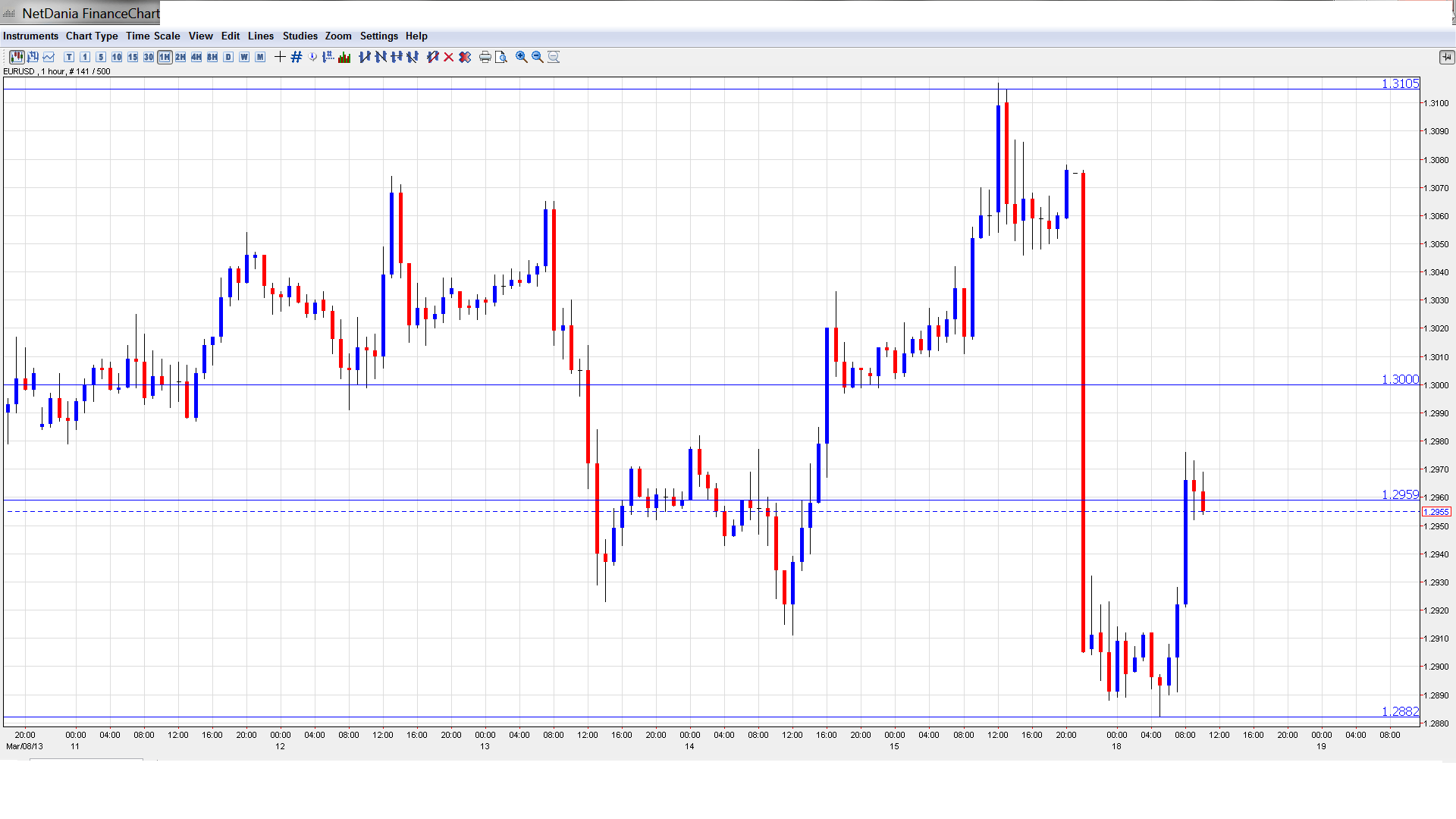

EUR/USD Technical

- Asian session: Euro/dollar fell sharply, touching a low of 1.2882. The pair consolidated at 1.2904. In the European session, the pair has rebounded, and was trading in the mid-1.29 range.

- Current range: 1.2960 to 1.3000.

Further levels in both directions:

- Below: 1.2960, 1.2880, 1.2805, 1.2746, 1.27, 1.2660 and 1.2587.

- Above: 1.3000, 1.3100, 1.3130, 1.3170, 1.3255, 1.3290, 1.3350, 1.34, 1.3486 and 1.3588.

- The pair is testing 1.30 on the downside. 12.2960 is stronger.

- 1.3030 is now providing weak resistance. The next resistance line is at the round number of 1.31.

Euro/dollar volatile after Cyprus bailout announcement – click on the graph to enlarge.

EUR/USD Fundamentals

- 9:00 Italian Trade Balance. Exp. 2.11B. Actual -1.62B

- 10:00 Eurozone Trade Balance. Exp. 10.4B. Actual 9.0B

- 14:00 US NAHB Housing Market Index. Exp. 48 points

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Euro slumps on Cyprus bailout news: The euro took a hit after the announcement of the Cyprus bailout. The agreement was reached over the weekend between the EU, IMF and the Cypriot government. Under the terms of the bailout package, deposit holders in Cypriot banks would be levied with a one-time tax, between 6.7% and 9.9%, depending on the size of the deposit. This tax will raise 5.8 billion euros, covering more than half of the 10 billion euro bailout. Taxing bank deposits is unusual ,and could result in depositors in other Eurozone countries with high debts to move their funds to countries such as Germany. The markets reacted negatively to the news, which also created a run on banks in Cyprus.

- US ends week on a whimper: A solid week for US releases ended on a sour note, as Friday’s numbers were a big disappointment. Earlier last week, employment and retail sales data looked sharp, but Friday was a different story. UoM Consumer Sentiment dropped to 71.8 points, and was way below the estimate of 78.2 points. The Empire State Manufacturing Index also lost ground, falling to 9.2 points, and missed the estimate of 9.8 points. There was some good news, as Industrial Production was higher, rising 0.7%. This beat the estimate of 0.4%. The markets will be keeping a close eye on this week’s Federal Reserve policy meeting, which could impact on the direction of EUR/USD.

- Italian Political Impasse Continues: The political stalemate which has paralyzed Italy for several weeks continues. Even by Italian standards, the political puzzle is bewildering, and the only solution may mean yet another election. Most Italians oppose going back to the polls, but so far, the political leaders have not made any headway as far as forming a new government. The financial markets are increasingly concerned that the ongoing political impasse will lead to economic instability. Last week, Italy’s three-year borrowing costs rose to their highest level since December. This comes on the heels of a recent credit downgrade to Italy’s debt by the Fitch rating agency. Italy is struggling with a massive debt of 1.9 trillion euros and weak growth, and needs to quickly from a government to deal with the country’s pressing economic troubles.

- Draghi optimistic, markets less so: ECB head Mario Draghi has all but guaranteed that the Eurozone economy will turn around later this year, but the markets are skeptical. Eurozone numbers continue to look sluggish, with Germany one of the few bright spots. Speculation continues that the ECB may pull the trigger and reduce interest rates if things don’t start to improve shortly. Meanwhile the Fitch ratings agency recently downgraded the debts of Italy and Spain, as well as Belgium, Cyprus, and Slovenia. The euro will have a tough time trying to gain ground if market sentiment on the Eurozone economy does not improve.