EUR/USD continues to trade quietly, with the pair trading in the high-1.28 range in Friday’s European session. On Thursday, US key releases, notably Unemployment Claims, were disappointing, but the euro failed to take advantage and didn’t make up ground against the dollar. There are no Eurozone releases on Friday. In the US, there are just three releases, highlighted by UoM Consumer Sentiment. The markets are expecting substantial improvement from the key indicator, which came in well below expectations in April.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

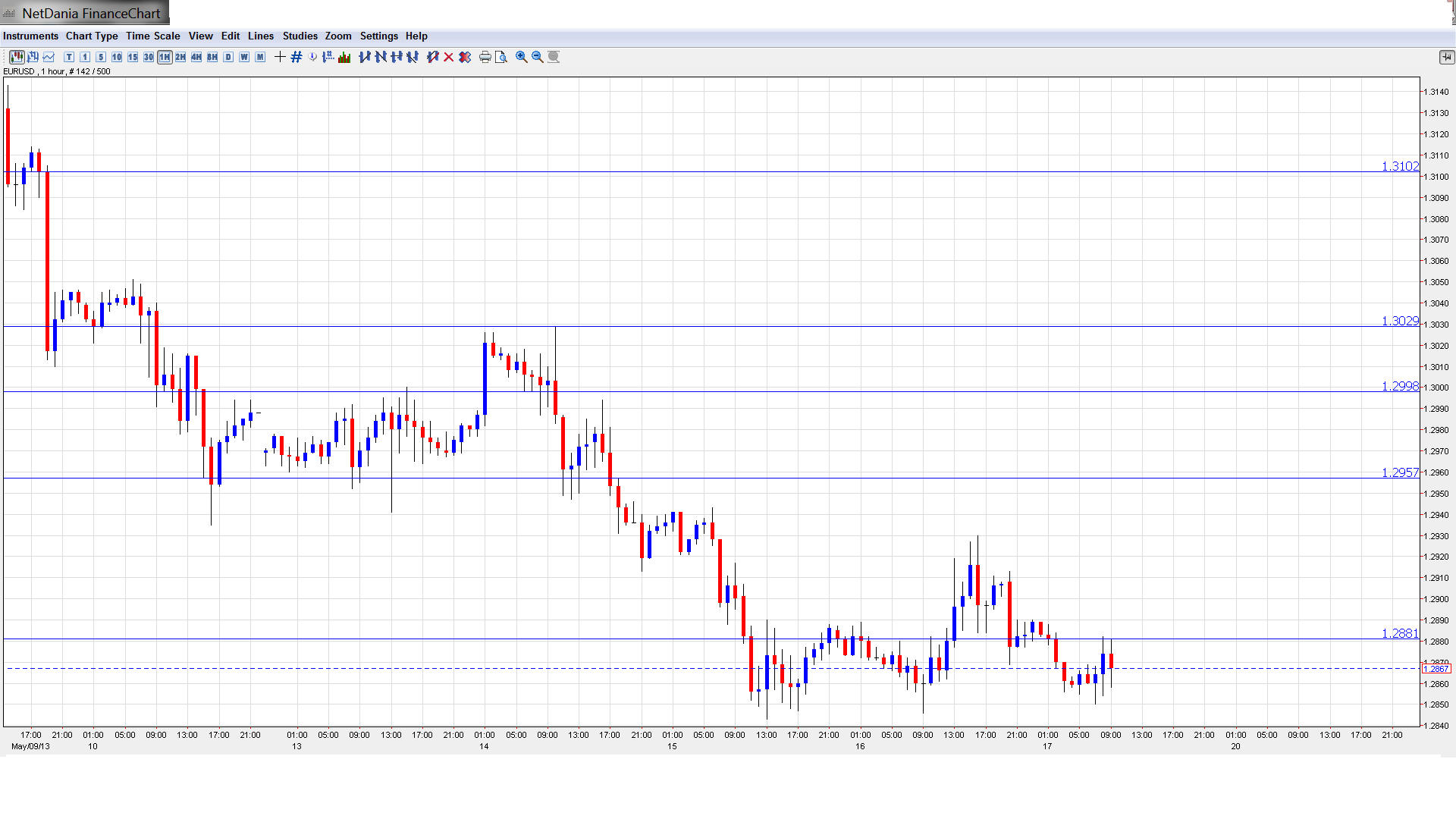

EUR/USD Technical

- Asian session: Euro/dollar lost ground, touching a low of 1.2851 and consolidating at 1.2858. The pair has edged higher in the European session.

- Current range: 1.28 – 1.2880.

Further levels in both directions:

- Below: 1.2805, 1.2750, 1.27, 1.2624 and 1.2587.

- Above: 1.2880, 1.2960, 1.30, 1.3030, 1.31, 1.3160 and 1.32.

- 1.2805 is the border of the long term 1.2805 – 1.3170 and is critical support.

- 1.2880 continues to provide resistance, but it is a weak line. 1.2960 is more significant.

Euro steady as US churns out weak key numbers – click on the graph to enlarge.

EUR/USD Fundamentals

- 13:55 US Preliminary UoM Consumer Sentiment. Exp. 77.9 points.

- 13:55 US Preliminary UoM Inflation Expectations.

- 14:00 US CB Leading Index. Exp. 0.3%.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- US data misses the mark: The markets were saturated with a host of key US releases on Thursday, but for the most part, the news was not encouraging. Core CPI posted a weak gain of 0.1%, shy of the estimate of a 0.2% gain. Unemployment Claims had looked impressive in recent readings, but this time the key indicator couldn’t keep pace this week as new claims jumped to 360 thousand, blowing past the estimate of 332 thousand. The Philly Fed Manufacturing Index dropped into negative territory, posting a reading of -5.2 points. The markets had expected a gain of 2.5 points. Housing Starts fell sharply, from 1.04 million to 0.85 million. This was well below the estimate of 0.98 million. There was some good news from Building Permits, which climbed up to 1.02 million. This beat the estimate of 0.94 million. The weak numbers will again bring into question the extent of the US recovery, which has not been able to demonstrate sustained growth and continuous positive releases.

- Euro-zone recession continues: Eurozone indicators did not have a good week, as economic releases pointed to contraction in the Eurozone for the third consecutive quarter. Output fell by 0.2%. At the time of the publication, this wasn’t totally unexpected, as Germany provided a big disappointment earlier: the economy grew by only 0.1% in Q1, short of 0.3% expected. Q4 was revised to a contraction of 0.7%. GDP numbers out of France and Italy continue to post declines, and both missed their estimates. The euro lost ground as a result, and dipped below the 1.29 level for the first time since early April.

- ECB considers negative deposit rates: The mention of negative deposit rates by ECB policymakers has not been accidental. ECB head Mario Draghi mentioned the idea when the ECB lowered interest rates a few weeks ago. Earlier in the week, ECB member Ignazio Visco reiterated that the ECB is considering the idea. The ECB would be the first major central bank to adopt negative deposit rates. Proponents of the idea argue that it would increase lending to businesses and help boost economic activity in the sluggish Eurozone, but it could also scare money away, as deposit holders look for more attractive locations to park their funds. The mere mention of the idea weighs on the euro. If the ECB takes steps to implement negative rates, we can expect the euro to react negatively.

- Will Fed scale back QE?: This is the vexing question facing the Federal Reserve. Has the US recovery gained a stronger footing? The Fed mentioned that fiscal policy is restraining the recovery, but at least tax revenue is up, and this defers the political issues regarding the debt ceiling. On Thursday, John Williams, president of the Federal Reserve Bank of San Francisco, stated that the Fed could begin reducing QE this summer and end bond buying late in 2013. Was this statement a trial balloon from Bernanke, intended to see how the markets would react? As the QE program is dollar negative, we can expect any statements from the Fed about scaling back QE to impact on EUR/USD.