EUR/USD continues to trade quietly, as the pair trades in the mid-1.32 range in Wednesday’s European session. On Tuesday, US JOLTS Jobs Openings disappointed, missing the estimate. There are no key releases out of the Eurozone or the US on Tuesday. In the Eurozone, French Final Non-Farm Payrolls and German Final CPI both matched the forecasts. In the US, President Obama addressed the nation about the Syrian crisis, saying that the US would not take military action if there was a possibility that a diplomatic solution could be reached.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

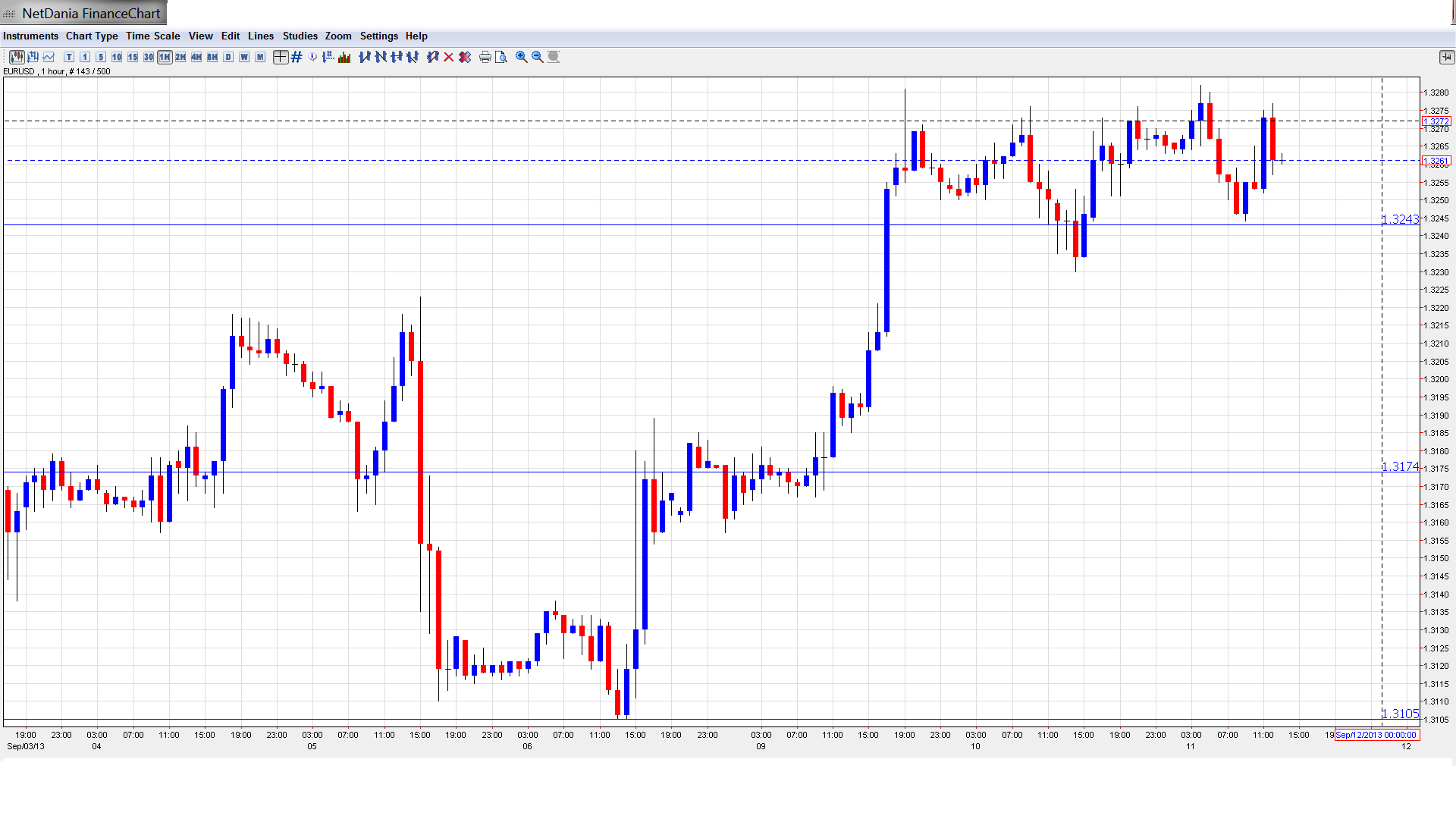

EUR/USD Technical

- In the Asian session, EUR/USD edged lower, touching a low of 1.3244 late in the session and consolidating at 1.3251. The pair has edged higher in the European session.

Current range: 1.3240 to 1.33.

Further levels in both directions:

- Below: 1.3240, 1.3175, 1.31, 1.3050 and 1.30.

- Above: 1.33, 1.3350, 1.3415, 1.3450, 1.3520, 1.3590 and 1.37.

- 1.33 is providing resistance. 1.3350 follows.

- 1.3240 is providing weak support. 1.3175 is stronger.

EUR/USD Fundamentals

- 1:00 President Obama Speaks. Obama says no military action for now.

- 5:30 French Final Non-Farm Payrolls. Exp. -0.2%, Actual -0.2%.

- 6:00 German Final CPI. Exp. 0.0%, Actual 0.0%.

- Tentative – German 10-year Bond Auction.

- 14:00 US Wholesale Inventories. Exp. 0.3%.

- 14:30 US Crude Oil Inventories. Exp. -2.2M.

- 17:00 US 10-year Bond Auction.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Weak US employment data may delay QE: The markets continue to speculate about QE tapering, but recent weak US employment numbers may cause a delay. Tuesday’s JOLTS Job Openings looked weak, coming in at 3.69 million, way off the estimate of 3.96 million. Last week’s Non-Farm Payrolls came in at 169 thousand, missing the estimate of 178 thousand. The Unemployment Rate dropped from 7.4% to 7.3%, but this improvement is not all that significant, given the low participation rate in the labor force. The Fed continues to keep mum about its plans, but we’re unlikely to see QE tapering without stronger employment numbers. Chicago Fed President Charles Evans hinted that we could see some action on this front from the Fed before the end of the year. Septapering still remains a credible possibility.

- Obama delays US strike on Syria: The Syrian crisis has taken on a new twist, as the US and Russia are looking for a diplomatic solution to the crisis. Under the proposed plan, Syria would destroy its entire arsenal of chemical weapons. President Obama spoke on US television on Monday and said that he would delay any military action as long as a diplomatic solution was possible, but that a strike against Syria was still on the table. If the diplomatic efforts gain momentum and the crisis eases, we could see the safe-haven dollar lose ground.

- Confidence on the rise in Eurozone: Confidence indicators out of the Eurozone have been looking up and the Eurozone Sentix Investor Confidence continued the positive trend earlier in the week. The indicator shot up from -4.9 points in July to a solid +6.5 points in August. Remarkably, this was the first reading above zero since August 2011, indicative of entrenched pessimism among investors over the past two years. If other confidence indicators follow suit with positive readings, the euro could gain ground.

- Only a green recovery in Europe: ECB president Mario Draghi said he is “not enthusiastic” about the return to growth and warned about money markets. In addition, the ECB lowered its growth forecast for 2014. A rate cut is still on the cards, and forward guidance is here to stay. On this background, the euro remains weak, and not only against the dollar.

Further reading:

- EURUSD Could Be Forming A Major Turning Point For The Year-Elliott Wave Analysis

- Forex Analysis: EUR/JPY Continues Consolidation within Clear Triangle Pattern