EUR/USD continues to move higher, as the pair broke through the 1.35 level in late Asian trading on Wednesday. The markets continue to monitor the Federal Reserve policy meeting, which wraps up today. Spanish GDP was a disappointment, dropping to its lowest level since 2009. The Italian 10-year Bond Auction will be released later in the day. In the US, the markets will have their hands full, as there are three key releases – ADP Non-farm Employment Change, Advance GDP and the FOMC Statement.

EUR/USD Technical

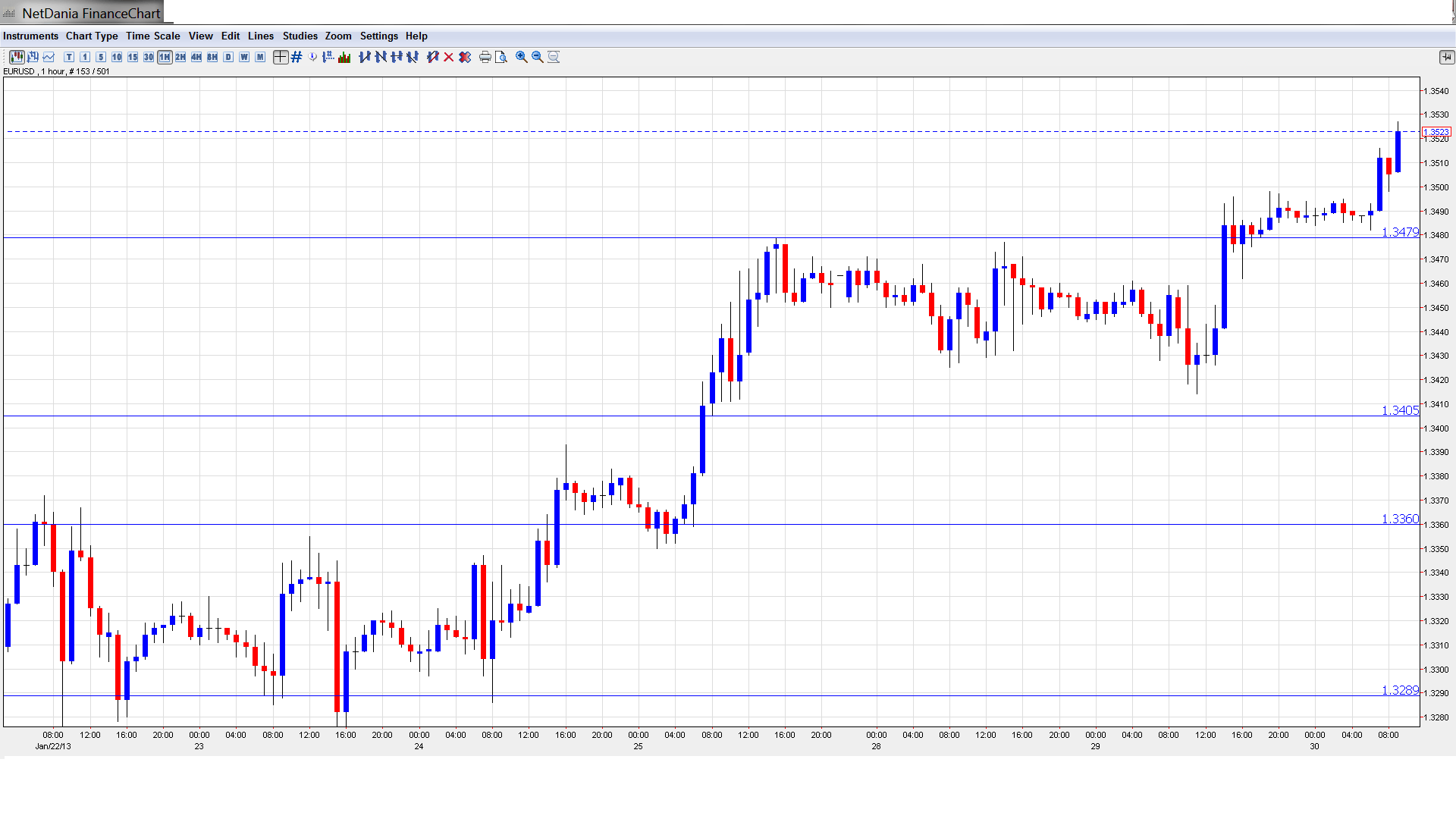

- Asian session: Euro/dollar was quiet, but pushed across 1.35 late in the session. The pair consolidated at 1.3506. The pair is unchanged in the European session.

- Current range: 1.3480 to 1.36.

Further levels in both directions:

- Below: 1.34, 1.3360, 1.3290, 1.3255, 1.3170, 1.3130, 1.3110, 1,3030, and 1.30.

- Above: 1.3480, 1.36, 1.3690, 1.3750 and 1.3838.

- 1.3480 is providing weak support. 1.34 has strengthened as the pair trades at higher levels.

- On the upside, 1.36 is providing strong resistance.

Euro/dollar pushes above 1.35 – click on the graph to enlarge.

EUR/USD Fundamentals

- 8:00 Spanish Flash GDP. Exp. -0.6%. Actual -0.7%.

- 9:10 Eurozone Retail PMI.

- Tentative: German 30-year Bond Auction.

- Tentative: Italian 10-year Bond Auction.

- 13:15 US ADP Non-Farm Employment Change. Exp. 164K.

- 13:30 US Advance GDP. Exp. 1.1%. See how to trade this event with USD/JPY.

- 13:30 US Advance GDP Price Index. Exp. 1.5%.

- 15:30 US Crude Oil Inventories. Exp. 2.9M.

- 18:00 German Deutsche Bundesbank President Jens Weidmann Speaks.

- 19:15 US FOMC Statement.

- 19:15 US Federal Funds Rate. Exp. <0.25%.

For more events and lines, see the Euro to dollar forecast

EUR/USD Sentiment

- Euro climbs ever higher: The euro continues to fly high, and has now climbed above the 1.35 line, its highest level since December 2011. EUR/USD has now jumped almost 500 points since early January. The continental currency has been bolstered by improving German data, as well as optimistic forecasts about the Eurozone economy from ECB President Mario Draghi and others. These officials acknowledge that the Eurozone is going through a tough time, but are confident that the economy will bounce back later in 2013. Although a range of indicators, notably employment and PMI numbers, point to a deepening recession and continuing fallout from the debt crisis, the euro continues to sparkle, at least for now.

- All Eyes on Federal Reserve: The markets are eagerly waiting for a statement from the Federal Reserve, as it wraps up an important two-day policy meeting. The Fed has not been in the headlines lately, but is busy at work, as it increased its purchases of securities in January from $40 billion to $85 billion. This has pushed the Fed’s balance sheet to a record $3 trillion. Despite these measures, the US recovery remains slow, and unemployment is still high at 7.8%. Minutes from the most recent FOMC pointed to members being divided between those in favor of ending QE in mid-2013, versus those who wish to continue it to a later date. When the Fed implemented the most recent round of QE, it stated that it would continue until unemployment fell to 6.5%. Most analysts are predicting that the Fed will reaffirm this stance.

- Is US Housing Market in Trouble? Although the US has posted been able to point to some strong releases recently, recent housing numbers have been in the tank. Last week, New Home Sales dipped to 369 thousand units, way below the estimate of 387 thousand. This shocked the markets, which had anticipated a modest gain of 0.5%. Pending Home Sales fared no better, plunging by 4.3%. This was the indicator’s worst showing since last May. The two key housing indicators points to weakness in the US housing industry, a critical component for economic growth. The bumpy US recovery will continue to limp along if these numbers don’t improve soon.

- US indicators all over the map: The extent of the US recovery is anyone’s guess, as US numbers continue to confound the markets. Employment and retail sales numbers have been very positive, but this has been offset by weak housing and consumer confidence data. We may get a better idea of the health of the US economy with the release of GDP on Wednesday. The markets are bracing for a relatively weak reading, with an estimate of a 1.1% gain. If the key indicator surprises the markets, we could see a reaction from EUR/USD.

- Fitch Gives Cyprus Thumbs Down: Cyprus saw its credit rating drop last week, as Fitch Ratings cut the island country’s rating by two levels to B. Fitch noted that that recapitalization costs for the Cypriot banking sector could be as high as 10 billion euros, higher than previously estimated. Cyprus officially requested a bailout last June, and is negotiating the terms with the ECB and the IMF. Fitch’s move follows a reduction by Moody’s, which downgraded the country’s forecast by three levels to Caa3. The downgrades underscore the weakness and vulnerability of the Cypriot economy and will increase pressure on all sides to reach an agreement on the terms of a rescue package.