The US dollar gained close to one cent on Wednesday, following the release of the minutes of the FOMC’s most recent policy meeting. Although there wasn’t any dramatic news, EUR/USD dropped close to one cent on the day. The pair was trading in the mid-1.33 range in European trading on Thursday. In economic releases, US Existing Home Sales jumped to its highest level in more than four years. On Thursday, French PMIs looked weak, while German and Eurozone PMIs beat their estimates. Over in the US, today’s major event is Unemployment Claims. As well, the Jackson Hole Symposium kicks off on Thursday. Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

EUR/USD Technical

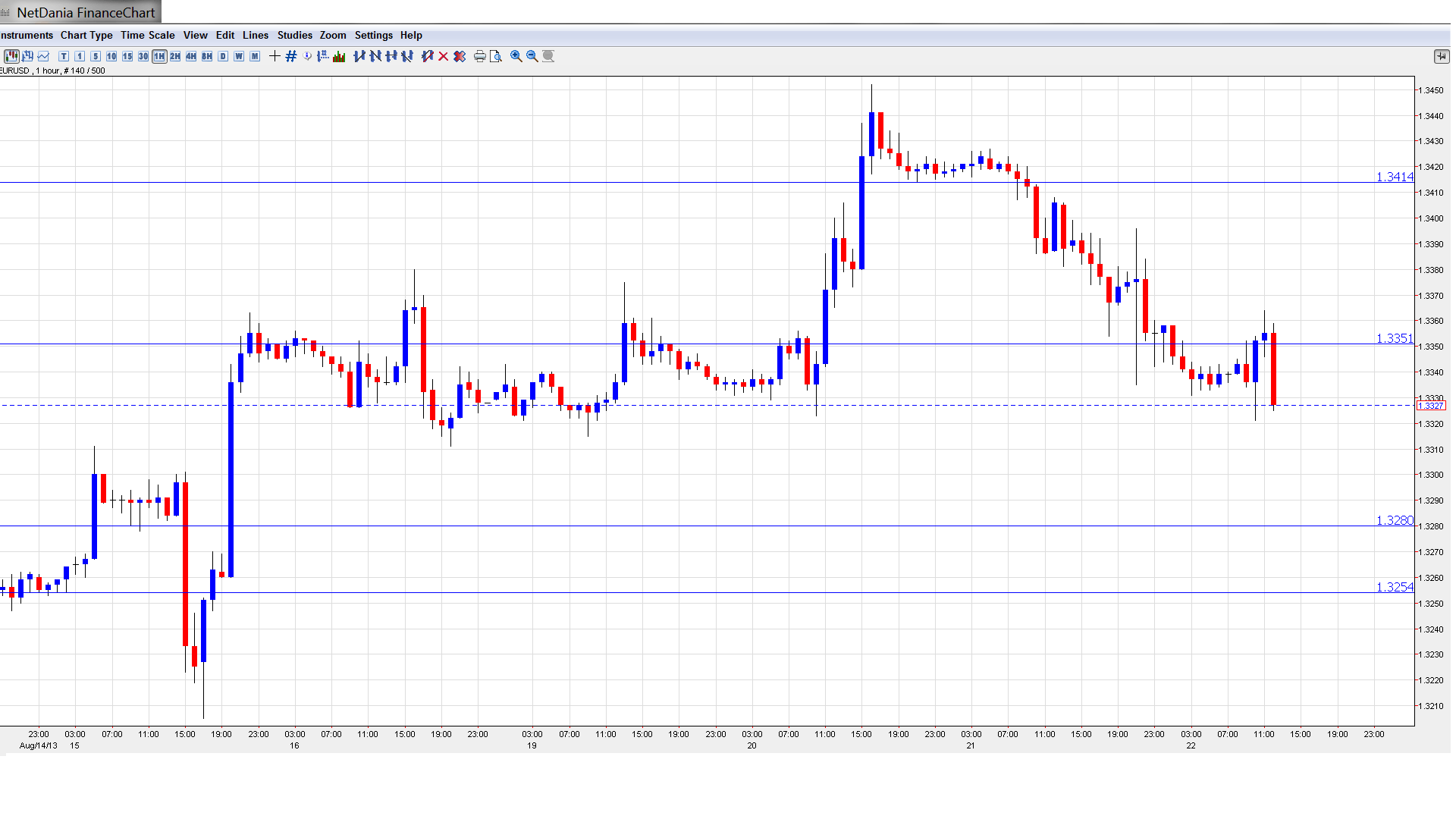

- In the Asian session, EUR/USD edged lower, dropping to 1.3332 before consolidating at 1.3347. The pair is unchanged in the European session.

Current range: 1.3350 to 1.3415.

Further levels in both directions:

- Below: 1.3350, 1.3280, 1.3255, 1.3175, 1.31, 1.3050 and 1.30.

- Above: 1.3415, 1.3480 and 1.3520.

- 1.3350 is under strong pressure on the downside.

- 1.3415 was providing support, but has switched back to resistance with the euro dropping into 1.33 territory.

EUR/USD Fundamentals

- 7:00 French Flash Manufacturing PMI. Exp. 50.4, actual 49.7 points.

- 7:00 French Flash Services PMI. Exp. 49.3, actual 47.7 points.

- 7:30 German Flash Manufacturing PMI. Exp. 52.0, actual 51.1 points.

- 7:30 German Flash Services PMI. Exp. 51.7, actual 52.4 points.

- 8:00 Eurozone Flash Manufacturing PMI. Exp. 50.9, actual 51.3 points.

- 8:00 Eurozone Flash Services PMI. Exp. 50.2, actual 51.0 points.

- 12:30 US Unemployment Claims. Exp. 329K.

- 13:00 US Flash Manufacturing PMI. Exp. 54.1 points.

- 13:00 US HPI. Exp. 0.6%.

- 14:00 US CB Leading Index. Exp. 0.5%.

- 14:30 US Natural Gas Storage. Exp. 68B.

- Day 1 – Jackson Hole Symposium.

- 19:15 Treasury Secretary Jack Lew Speaks.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Fed Split on QE Tapering: The markets eagerly waited for the release of the FOMC minutes of its most recent policy meeting, but the minutes didn’t contain any dramatic revelations. Despite this, the US dollar still gained almost one cent against the euro. Fed officials were described as “broadly comfortable” with plans to taper QE, but remain split on the timing of such a move. The policymakers stated that recent US economic data was “mixed”, and all members agreed that it was still too early to scale back the current bond-buying levels of $85 billion each month. However, a September taper still remains a realistic possibility.

- Another Greek Bailout in the works?: Greece has already received two bailouts, but the economy is in difficult straits, so a third bailout appears likely. The latest officials to acknowledge this are EU Commissioner Olli Rehn and German finance minister Wolfgang Schaeuble. Greece doesn’t reject more money, but says it may require less than beforehand. Tourism is on the rise, but unemployment, especially among youngsters is extremely high. Such a move promises to be unpopular in Germany, and could hurt Chancellor Angela Merkel in the polls, with just 4 weeks to go before national elections in Germany. Another rescue package could damage Merkel’s credibility, as she recently said she didn’t see a need for more aid to Greece. Greece has already received some EUR 240 billion in bailout aid, but another bailout would be on a much smaller scale.

- Increased Likelihood of Summers taking over Fed: Media reports in the US continue talking about Larry Summers as the leading candidate to lead the Federal Reserve after Bernanke. An announcement is expected during the autumn. Opinion: Fed Chair impact on USD: Summers up, Yellen down.

- Important data Septaper supportive: Inflation figures came out as expected and pointed to 2% YoY in CPI and 1.7% in core CPI. This should be enough for the Fed. In addition, jobless claims fell to a new multi-year low of 320K. Excellent pro-dollar news. However, tapering remains a close call for both the Fed and the markets and the follow up after the Philly number was totally different.

- Recession ends in the euro-zone, but doubts remain: Germany and France lead the euro-zone together once again. After some strong data out of France, French Service and Manufacturing PMIs were a disappointment, as both fell short of the estimates. German and Eurozone PMIs were stronger, as all releases were above the 50-point-level, indicating expansion. Here are 4 reasons why the euro-zone is out of recession, but not out of the woods.

- The Netherlands to miss deficit target: Dutch finance minister Jeroen Dijsselbloem, who also leads the Eurogroup, said that his country will not meet the EU deficit target for 2014. The weakness in the rich northern shadow casts a shadow over the zone.

More:

- Opinion: Euro strength – how long will it last?

- Forex Analysis: EUR/USD Advances Sharply to Six-Month High