EUR/USD is steady in Wednesday trade, as the pair shows little movement for the second straight day. In the European session, the euro is trading in the mid-1.38 range. Eurozone Industrial Production declined in February but the euro did not lose ground as a result. In the US, JOLTS Job Openings dipped to a three-month low and fell short of the estimate. It’s a quiet day in the US, highlighted by Crude Oil Inventories.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

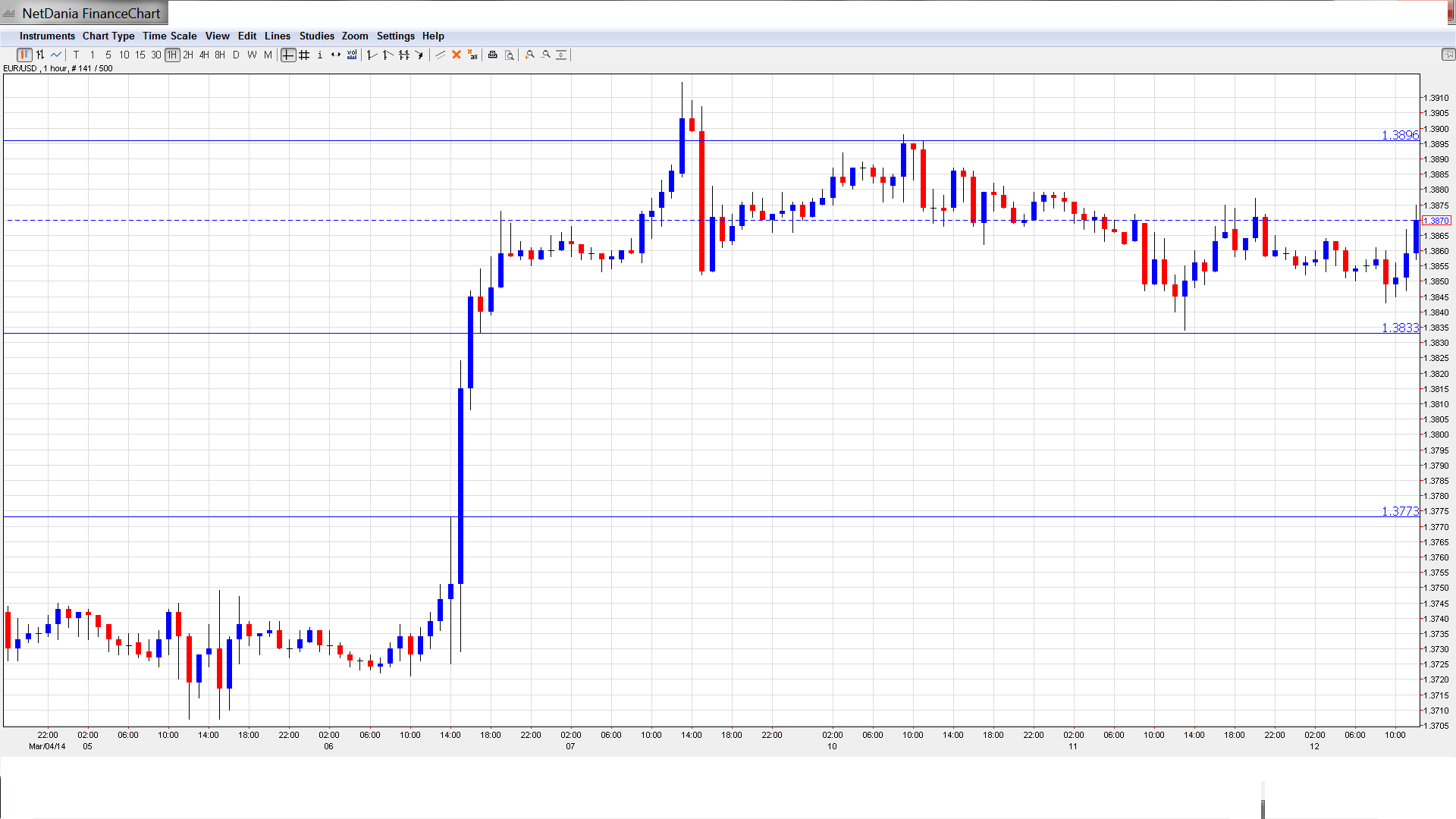

EUR/USD Technical

- EUR/USD showed little activity in the Asian session and closed at 1.3851. The pair has edged higher in the European session.

Current range: 1.3830 to 1.3895.

Further levels in both directions:

- Below: 1.3830, 1.3773, 1.37, 1.3650, 1.3560, 1.3515 and 1.3450.

- Above: 1.3895, 13940 and 1.40.

- 1.3895 is the next resistance line. 1.3940 follows. It is protecting the key 1.40 line.

- 1.3830 continues to provide support, but is a weak line. 1.3773 is stronger.

EUR/USD Fundamentals

- 6:30 French Final Nonfarm Payrolls. Exp. 0.1%. actual 0.1%.

- 10:00 Eurozone Industrial Production. Exp. 0.6%, actual -0.2%.

- 14:30 US Crude Oil Inventories. Exp. 2.1M.

- 17:01 US 10-year Bond Auction.

- 18:00 US Treasury Secretary Jack Lew Speaks.

*All times are GMT

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- US employment numbers fall short: Tuesday’s employment numbers were not a disaster, but could have been better. JOLTS Job Openings dipped to 3.97 million in February, missing the estimate of 4.02 million and slipping to a three-month low. On Friday, Nonfarm Payrolls jumped to 175 thousand in February, compared to just 113 thousand last month. This easily beat the estimate of 151 thousand. The Unemployment Rate edged up to 6.7%, up from 6.6% in the previous reading. With the markets expecting the Fed to trim QE next week, every employment release should be treated as a market-mover.

- QE taper likely: With the US posting solid Unemployment Claims and Nonfarm Payrolls late last week, the markets can breathe more comfortably as the Fed is likely to take its scissors and trim QE next week for the third time. New York Fed President William Dudley stated last week that the threshold to alter the Fed’s program to wind up QE was “pretty high”. In other words, short of a serious economic downturn in the US economy, we can expect the QE tapers to continue.

- Euro surges after ECB decision: The euro rose sharply after the ECB rate decision late last week, but this time it was due to a lack of action by the central bank, rather than a change in monetary policy or any dramatic comments by Draghi. There had been speculation that the ECB might lower deposit rates into negative territory or even commence a mini-QE scheme. In the end, the Bank held the course, with Draghi reiterating his well-worn script that the ECB’s high degree of accommodative monetary policy would continue for as long as needed. He also noted that the Eurozone economy was recovering at a moderate pace, and shrugged concerns about inflation levels well below the ECB’s target of 2%. Draghi may be able to point to encouraging data out of Germany to bolster his case that the region is headed in the right direction, but Eurozone data as well as numbers from major economies, such as France and Italy, raise questions about the health of the Eurozone.

- France in trouble?: French releases continue to struggle, as Industrial Production fell by 0.2% last month, its fourth decline in five readings. The markets had expected a gain of 0.6%. Trade Balance lost ground in February and the most recent Consumer Spending posted a sharp decline, pointing to weak consumer confidence in the economy. France is the Eurozone’s second largest economy after Germany, and continuing weak French data could hurt the euro.