EUR/USD made an attempt to move higher, but never went too far A key German survey, fresh inflation figures and Draghi’s testimony stand out. Will we have a breakout to close September? Here is an outlook for the highlights of this week and an updated technical analysis for EUR/USD.

Worries about a hard Brexit and some weaker data weighed on the euro. PMIs were mostly positive but did not cheer up the common currency. The Fed was at the center of attention: the rates were left unchanged as expected, and the door is wide open to a hike in December. EUR/USD enjoyed the no-hike message, but this did not last too long.

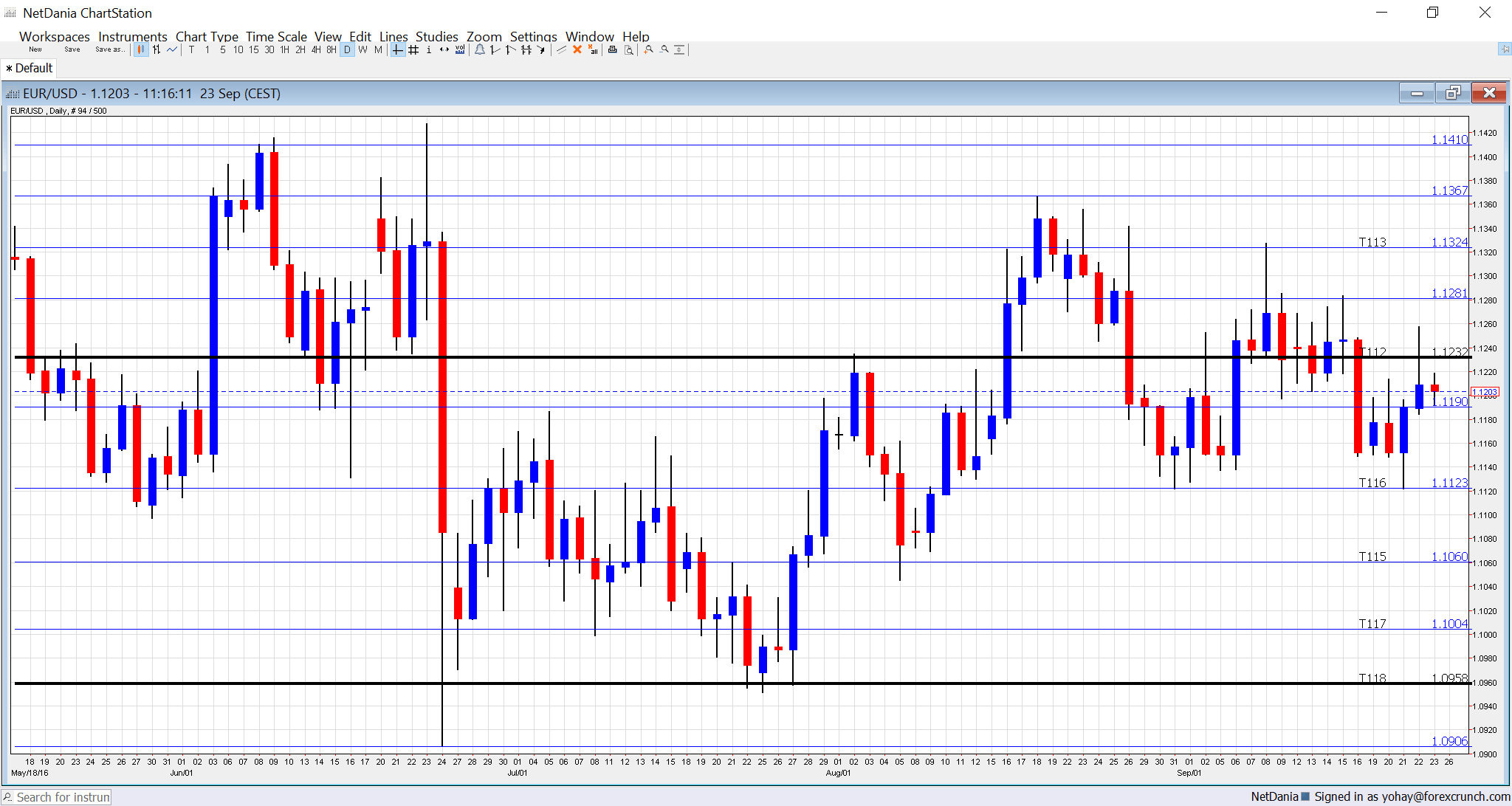

[do action=”autoupdate” tag=”EURUSDUpdate”/]EUR/USD daily graph with support and resistance lines on it. Click to enlarge:

- German Ifo Business Climate: Monday, 8:00. IFO is Germany’s No. 1 Think tank. In August, their business barometer disappointed with a drop to 106.2 points, a move that is only partially related to Brexit, as the indicator remained steady beforehand. A score of 106.3 is projected now.

- Mario Draghi testifies: Monday, 14:00. The president of the ECB had a public appearance last week, but dodged monetary policy topics. This time will probably be different: Draghi will provide a prepared statement as well as a long Q&A session. Far enough from the next ECB meeting, due in mid-October, he is limited by the “quiet period” and could hint about how QE should evolve. He hinted about changes to the program but did not provide details in the recent rate decision.

- German Import Prices: Tuesday, 6:00. Prices of imports eventually feed into wider inflation. Fluctuations in energy prices could be reflected here. A rise of 0.1% was seen last time. A drop of the same scale is on the cards now.

- Monetary data: Tuesday, 8:00. The ECB’s monetary stimulus, in all its forms, helped stir lending, but things have been stuck lately. The annual increase in money supply, M3, has slightly slowed down to 4.8%. On the other hand, private loans have been rising at a pace of 1.8% YoY in the past two months. Both figures are expected to tick up to 4.9% and 1.9% respectively.

- German GfK Consumer Climate: Wednesday, 6:00. According to this 2000 strong survey, consumers in the continent’s largest economy are now more confident than beforehand, with a score of 10.2 points in August. No change is expected now.

- German CPI: Thursday: the various German states publish their flash estimates during the morning, with the all-German number released at 12:00. In August, inflation fell short of expectations by remaining flat. This weighed on the whole euro-area. Another flat read MoM is predicted.

- Spanish CPI: Thursday, 7:00. The fourth largest economy in the euro-zone enjoys strong growth but also suffered from deep deflation. Prices have moved up of late, with an annual drop of only 0.1% in August, slightly better than expected. A return to positive ground is expected, with +0.1% y/y.

- German Unemployment Change: Thursday, 7:55. The consistent drop in German unemployment has been one of the stronger points in the old continent. A drop of 7K was recorded for July. A smaller drop of 5K is expected.

- German Retail Sales: Friday, 6:00 .The volume of sales in the continent’s locomotive surprised with a strong rise of 1.7% in July. We may see a slide in August. A slide of 0.2% is forecast now.

- French Consumer Spending: Friday, 6:45. In the continent’s second largest economy, consumers have been less buoyant. Spending has dropped by 0.2% in July. A rise of 0.4% is on the cards.

- French CPI: Friday, 6:45. The French figure provides the last opportunity to shape expectations ahead of the all-European number. Prices surprised with a +0.3% rise in August. We now get the early number for September. A slide of 0.3% expected.

- Flash CPI: Friday, 9:00. Despite coming after the German and French numbers, this publication can surprise, as it did last month, with a disappointing number. After prices advanced only 0.2% in. A significant rise in headline inflation is predicted: 0.4%, stemming from the base effects of oil prices. Core inflation is also expected to rise, to 0.9%.

- Unemployment Rate: Friday, 9:00. The unemployment rate did fall in the euro-zone but remains stubbornly high. It stood at 10.1% in July. A small slide to 10% is on the cards.

* All times are GMT

EUR/USD Technical Analysis

Euro/dollar kicked off the week above support at 1.1230 (mentioned last week). However, it never went too far. 1.1125 is strengthening as support, a double bottom now.

Technical lines from top to bottom:

1.1535 is a stepping stone as seen in May 2016 and also beforehand. It is followed by the very round level of 1.15.

1.1460 was a key resistance line in 2015 and 1000 above the multi-year lows. 1.1410 capped the pair in early June. 1.1375 worked as resistance in February and as support in May 2016.

1.1335 worked as the bottom bound of a higher range and then capped recovery attempts in May. 1.1230 capped the pair after the fall in May and worked as resistance.

1.1190 is the post-Brexit high seen in July. 1.1125 cushioned the pair in early September. 1.1070 served as a clear separator of ranges during February and also beforehand.

1.10 is a round number and significant resistance. 1.0905 is the swing low seen in June and serves as a weak support. 1.0825 worked as support in early March 2015 and should also be watched. This is now a triple bottom.

The post-Draghi low 1.0780 replaces 1.08 as support. 1.0710 is the next support line on the chart after temporarily capping the pair in April 2015.

Further below, the 2016 low of 1.0520 and the 2015 low of 1.0460 provide further support.

I remain bearish on EUR/USD

The Fed made sure it’s on the hawkish side and the ECB is going in the other direction. The greenback also has the safe-haven advantage, becoming more important as the US elections get closer and the race is tight.

Our latest podcast is titled Bold BOJ vs. Fearful Fed