EUR/USD continues to lose ground on Thursday, as the pair trades in the mid-1.37 range in the European session. The euro has now lost close to a cent since the beginning of the week. In economic news, US manufacturing numbers were a mix on Wednesday. In Thursday action, Eurozone M3 Money Supply and Private Loans met expectations. In the US, there are two key events, Unemployment Claims and Pending Home Sales. As well, we’ll get a look at US Final GDP.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

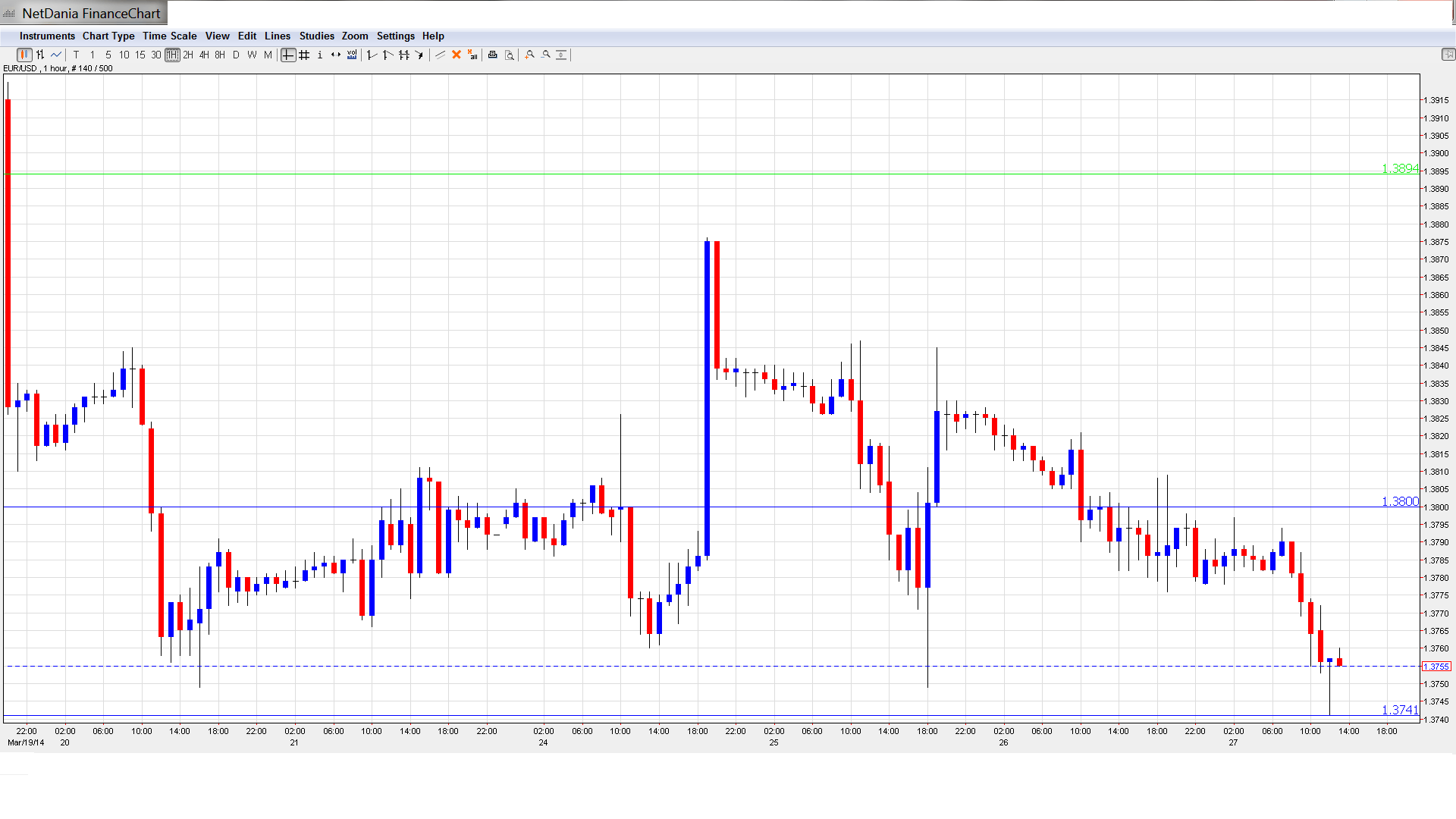

EUR/USD Technical

- EUR/USD edged lower in the Asian session, closing at 1.3765. The pair continues to point downwards in European trading.

Current range: 1.3740 to 1.38.

Further levels in both directions:

- Below: 1.3740, 1.37, 1.3650 and 1.3560, 1.3515 and 13450.

- Above: 1.38, 1.3895, 1.3940, and 1.40

- 1.3740, the new important support line, is under strong pressure. The round number of 1.37 follows.

- 1.38 is the next resistance line. 1.3895 is stronger.

EUR/USD Fundamentals

- 9:00 Eurozone M3 Money Supply. Exp. 1.3%, Actual 1.3%.

- 9:00 Eurozone Private Loans. Exp. -2.1%, Actual -2.2%.

- 12:30 US Unemployment Claims. Exp. 326K.

- 12:30 US FOMC Member Sandra Pianalto Speaks.

- 12:30 US Final GDP. Exp. 2.7%.

- 12:30 US Final GDP Price Index. Exp. 1.6%.

- 14:00 US Pending Home Sales. Exp. 0.1%. See how to trade this event with EUR/USD.

- 14:30 US Natural Gas Storage. Exp. -49B.

*All times are GMT For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- ECB mulls negative rates, QE: German Bundesbank head Jens Weidmann gave support to a negative deposit rate in order to respond to the strong euro. He also raised the possibility of a QE scheme for the ECB, whereby the central bank would purchase loans or other assets in order to fight deflation, which continues to suffer from low inflation. Mario Draghi also spoke on the issue, saying that the ECB is ready to act if inflation slips further.

- US manufacturing data a mix: US readings continue to paint a mixed picture, thanks to releases which have been pointing in both directions. Core Durable Goods Orders posted a weak gain of 0.2%, shy of the estimate of 0.3%. Durable Goods Orders looked sharper, jumping 2.2% last month. This broke a mini-streak of two straight declines, and easily surpassed the estimate of 1.1%. On Tuesday, New Home Sales missed the forecast but CB Consumer Confidence climbed to a six-year high.

- German consumer confidence firm: German Consumer Climate remains at high levels, posting a second straight reading of 8.5 points, matching the forecast. The indicator has steadily risen, and the last time we saw a stronger reading was back in 2007, before the global economic crisis. German Business Climate also looked sharp in February. Increasing consumer confidence usually translates into more consumer spending, which is a critical component of economic growth. We’ll get a look at German Preliminary CPI on Friday.

- The Mario cap: With the recent fall, EUR/USD is far from the round 1.40 line. As we’ve seen, ECB president did not hesitate to talk the euro down once it got close to these levels. This “verbal resistance line” counters Chinese flows into the Eurozone.

- Ukraine gets critical cash: Ukraine’s economy is in shambles as a result of the four-month political crisis. Prime Minister Arseniy Yatsenyuk acknowledged that the country is on the edge of bankruptcy, and GDP could drop by 3% this year. However, help is on the way. The IMF is set to sign a two-year loan of up to $18 billion, and the EU has offered a package of EUR 11 billion. Ukraine has already received two bailouts from the IMF since 2008, and will have to implement budget cuts and other measures in order to receive the new package from the IMF.