EUR/USD continues to trade at low levels on Wednesday, as the pair trades in the mid-1.32 range. The euro has lost over 100 points this week and finds itself at its lowest level since September 2013. On the release front, a host of Euro PMIs painted a mixed picture, with German figures beating their estimates. It’s a busy day in the US, with two major events on the calendar – Unemployment Claims and the Philly Fed Manufacturing Index.

Here is a quick update on what’s moving the pair.

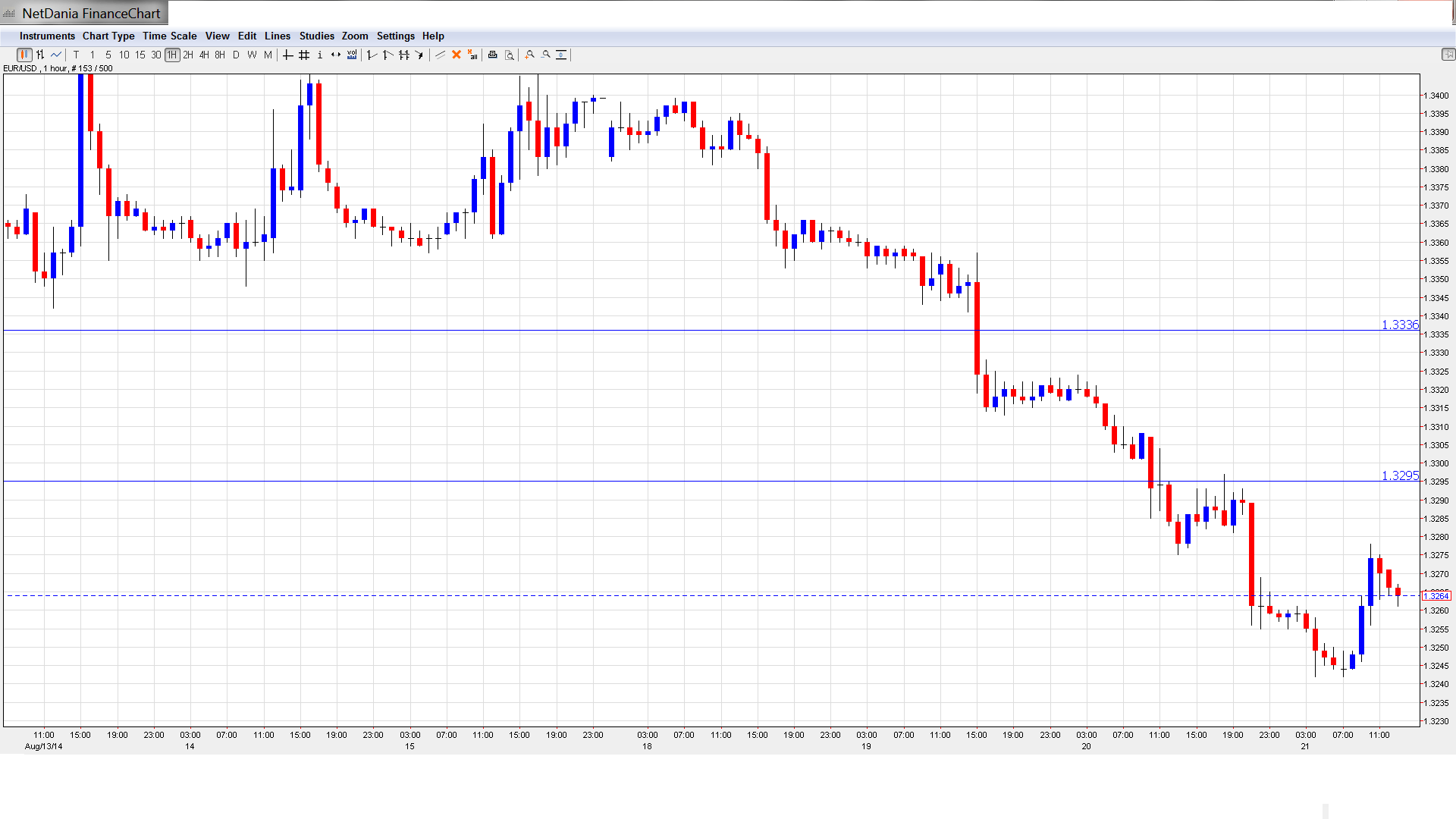

- EUR/USD edged lower in the Asian session but then reversed directions and continues to move upwards in European trade.

- Current range: 1.32 to 1.3295.

Further levels in both directions:

- Below: 1.32, 1.3104 and 1.2984

- Above: 1.3295, 1.3333, 1.3415, 1.3450 and 1.35

- The round number of 1.32 is providing support.

- 1.3333, a key line, has switched to resistance as the euro continues to lose ground. 1.3415 is next.

EUR/USD Fundamentals

- 7:00 French Flash Manufacturing PMI. Estimate 47.9, actual 46.5 points.

- 7:00 French Flash Services PMI. Estimate 50.3, actual 51.1 points.

- 7:30 German Flash Manufacturing PMI. Estimate 51.7, actual 52.0 points.

- 7:30 German Flash Services PMI. Estimate 55.5, actual 56.4 points.

- 8:00 Eurozone Flash Manufacturing PMI. Estimate 51.4, actual 50.8 points.

- 8:00 Eurozone Flash Services PMI. Estimate 53.6, actual 53.5 points.

- 12:30 US Unemployment Claims. Estimate 302K.

- 13:45 US Flash Manufacturing PMI. Estimate 55.7 points.

- 14:00 Eurozone Consumer Confidence. Estimate -9 points.

- 14:00 US Philly Fed Manufacturing Index. Estimate 19.7 points.

- 14:00 US Existing Home Sales. Estimate 5.01M.

- 14:00 US CB Leading Index. Estimate 0.6%.

- 14:30 US Natural Gas Storage. Estimate 83B.

- Day 1 – Jackson Hole Symposium.

*All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- Fed vague about interest rate hike: In a highly anticipated event, the Federal Reserve released its policy meeting minutes on Wednesday. The minutes were hawkish in tone, with the Fed saying that an interest rate hike could come sooner rather than later if employment numbers continue to improve. As expected, the Fed avoided being specific about the timing of an interest rate hike, which is expected before mid-2015. The Fed said that the economy continues to improve, but the QE program, which is scheduled to wind up in October, will not be accelerated. Once the asset purchase scheme is terminated, the guessing game regarding a rate hike will only intensify.

- Eurozone PMIs soften, but beat estimates: The Eurozone released Services and Manufacturing PMIs, and the results were mixed. French Manufacturing PMI came in at 46.5 points, the fourth straight reading below 50, which separates between contraction and expansion. French Flash Services PMI came in at 51.1, above the estimate. In Germany, the Service and Manufacturing PMIs both softened in July but beat the estimates. Eurozone Manufacturing and Services PMIs also weakened in July. There is cause for concern as most of the PMI readings were weaker compared to a month earlier, underscoring weak economic growth in the Eurozone.

- US inflation numbers remain low: The US recovery has been moving in the right direction, but inflation numbers in the US remain feeble. On Tuesday, CPI and Core CPI, the primary gauges of consumer inflation, both posted paltry gains of 0.1%. These weak readings followed PPI, a manufacturing inflation index, which also came in at 0.1% last month. Weak inflation is one reason why the Federal Reserve is in no rush to raise interest rates, as low inflation points to slack in the economy.

- German, French inflation remains sluggish: The ECB tried to increase inflation with broad interest rate cuts in June, but inflation levels have not risen. Eurozone Final CPI dipped to 0.4%, down from 0.5% a month earlier. Draghi did not seem worried about this, but did go to explain why EUR/USD should slide. Deflation remains a paramount concern and could cause havoc with the sputtering Eurozone economy.

- Geopolitical conflicts could rattle markets: Hotspots in Ukraine and the Middle East remain tense and could have dramatic effects on the markets. In eastern Ukraine, more fighting has been reported between Ukrainian forces and pro-Russian separatists, and large numbers of Russian forces remain close to the border. In Iraq, Kurdish forces, aided by US air strikes, are battling with Islamic State militants. As political turmoil continues in Iraq, the national government is becoming increasingly irrelevant. In Gaza, fighting has renewed between Israel and Hamas as the latest ceasefire broke down on Tuesday.