GBP/USD dropped sharply last week, losing 250 points. The pair closed at 1.2318. This week’s key event is Second Estimate GDP. Here is an outlook for the highlights of this week and an updated technical analysis for GBP/USD.

In the UK, CPI came in at 0.9%, short of the forecast of 1.1%. Retail Sales sparkled at 1.9%, but this wasn’t enough to prevent the pound from posting sharp losses on Friday. The US dollar continues to post broad gains after Trump’s stunning electoral victory. US inflation numbers were mixed, while unemployment claims dropped to a 43-year low.

[do action=”autoupdate” tag=”GBPUSDUpdate”/]The BoE revised upwards its forecast for economic growth, essentially acknowledging that its earlier forecasts of Brexit were far too pessimistic. The BoE also held interest rates at 0.25%, helping fuel the pound’s surge. US Non-Farm Payrolls were upbeat and wage growth improving to 0.3%, above the estimate of 0.2%. The Fed refrained from raising rates last week, but the policy statement was slightly hawkish, as the Fed gave the economy a solid report card.

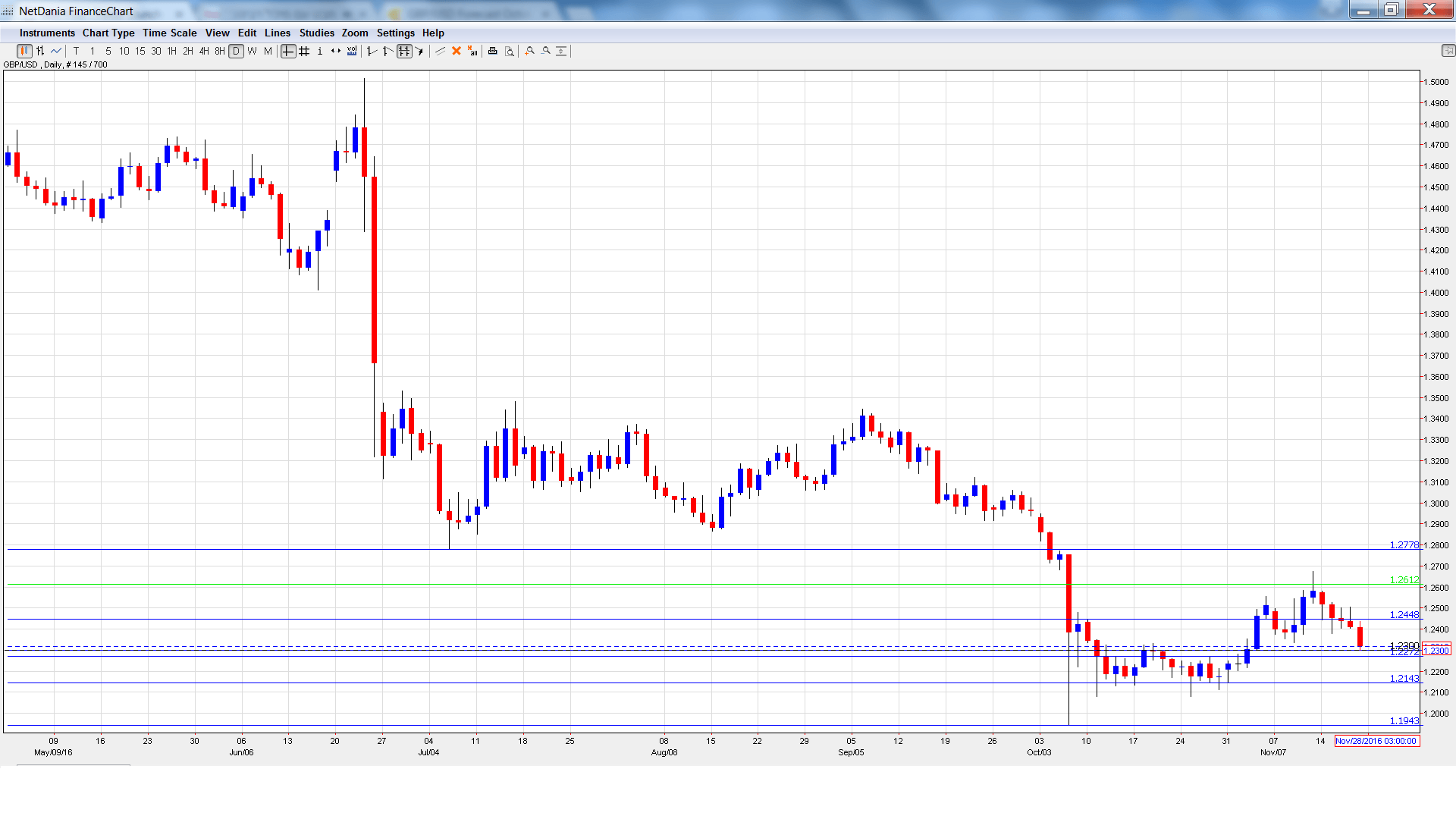

GBP/USD graph with support and resistance lines on it. Click to enlarge:

- Public Sector Net Borrowing: Tuesday, 9:30. The UK surplus remained unchanged at GBP 10.1 billion in September, beating the estimate of GBP 8.6 billion. The markets are expecting the estimate to narrow to GBP 5.9 billion in October.

- 10-year Bond Auction: Tuesday, Tentative. The 10-year bond yield climbed to 1.08% in October, marking a 3-month high. Will the upswing continue in the November auction?

- CBI Industrial Order Expectations: Tuesday, 11:00. This manufacturing index plunged to -17 points in October, much weaker than the forecast of -2 points. The estimate for November stands at -8 points.

- Autumn Forecast Statement: Wednesday, 12:30. This annual statement previews the government’s budget, including spending and financial objectives. It should be treated as a market-mover.

- BBA Mortgage Approvals: Thursday, 9:30. The indicator provides a snapshot of the level of activity in the British housing sector. The indicator rose to 38.3 points in September, beating expectations. The upward trend is expected to continue, with an estimate of 38.8 points.

- Nationwide HPI: Friday, 25th-29th. The housing inflation indicator dropped to a flat 0.0% in October, shy of the estimate of 0.2%. Will we see a rebound in the November reading?

- Second Estimate GDP: Friday, 9:30. An unexpected reading can have a sharp impact on the movement of GBP/USD. Preliminary GDP for Q3 gained 0.5%, above the forecast of 0.3%. The estimate for Second Estimate GDP for Q3 stands at 0.5%.

- Preliminary Business Investment: Friday, 9:30. This quarterly release rebounded in Q2 with a gain of 0.9%. The markets had anticipated a decline of 0.9%. The estimate for Q3 stands at -0.2%.

* All times are GMT

GBP/USD Technical Analysis

GBP/USD opened the week at 1.2574 and quickly touched a high of 1.2579. The pair then reversed directions and dropped to the round number of 1.2300, as support held at 1.2272 (discussed last week). GBP/USD closed the week at 1.2579.

Live chart of GBP/USD:

Technical lines from top to bottom

With the pair posting sharp losses last week, we begin at lower levels:

1.2778 is a strong resistance line.

1.2612 was a cushion back in 1985.

1.2448 has switched to a support role after sharp losses by GBP/USD.

1.2272 is an immediate support level.

1.2143 has been a cushion since late November.

1.1943 is the final support line for now.

I am bearish on GBP/USD.

The US dollar continues to roll since the US election and with the Fed expected to raise rates in December, sentiment towards the greenback is very favorable. At the same time, the markets remain jittery about the effects that Brexit will have on the British economy, as politicians on both sides of the Channel seemed resigned to difficult negotiations ahead over the UK’s exit from the EU.

Our latest podcast is titled Not all financial assets are Trump-ed equally

Follow us on Sticher or iTunes

Further reading:

- For a broad view of all the week’s major events worldwide, read the USD outlook.

- For EUR/USD, check out the Euro to Dollar forecast.

- For the Japanese yen, read the USD/JPY forecast.

- For the kiwi, see the NZD/USD forecast.

- For the Australian dollar (Aussie), check out the AUD to USD forecast.

- For the Canadian dollar (loonie), check out the USD to CAD forecast.