EUR/USD is almost unchanged in Thursday trading as the markets wait for a statement following the ECB policy meeting on Thursday. The pair is trading in the low-1.35 range in the European session. In economic news, German Industrial Production was well below the estimate. Over in the US, today’s key releases are Advance GDP and Unemployment Claims.

Here is a quick update on the technical situation, indicators, and market sentiment that moves euro/dollar.

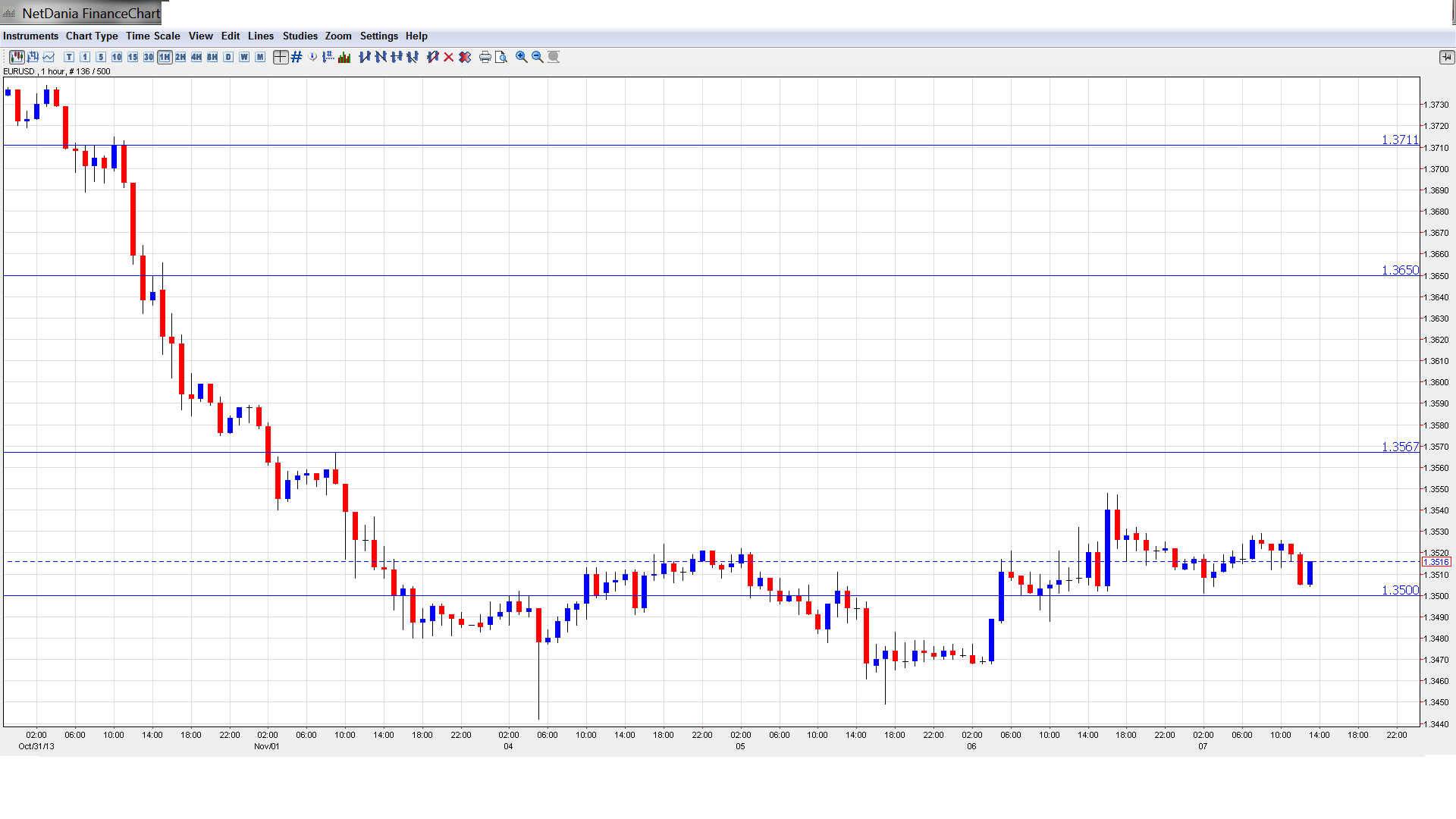

EUR/USD Technical

- In the Asian session, EUR/USD was steady. The pair touched a low of 1.3501 but then edged higher and consolidated at 1.3524. EUR/USD is unchanged in the European session.

- Current range: 1.3500 to 1.3570.

Further levels in both directions:

- Below: 1.3500, 1.3460, 1.3415, 1.3325 and 1.3240, 1.3175, 1.31, 1.3050 and 1.3000.

- Above: 1.3570, 1.3650, 1.3710, 1.3800, 1.3870 and 1.3940.

- On the downside, 1.3500 remains under pressure. 1.3460 is next.

- 1.3570 is the next resistance line. It is followed by 1.3650.

EUR/USD Fundamentals

- 9:43 Spanish 10-year Bond Auction. Actual. 4.16%.

- 9:58 French 10-year Bond Auction. Actual 2.41%.

- 11:00 German Industrial Production. Exp. 0.2%

- 12:45 ECB Minimum Bid Rate. Exp. 0.50%.

- 13:30 ECB Press Conference.

- 13:30 US Advance GDP. Exp. 2.0%.

- 13:30 US Unemployment Claims. Exp. 336K.

- 13:30 US Advance GDP Price Index. Exp. 1.5%.

- 15:30 US Natural Gas Storage. Exp. 40B.

- 18:30 FOMC Member William Dudley Speaks.

- 18:50 FOMC Member Jeremy Stein Speaks.

- 19:00 ECB President Mario Draghi Speaks. Draghi will address an economic forum in Hamburg.

- 20:00 US Consumer Credit. Exp. 13.0B.

* All times are GMT.

For more events and lines, see the Euro to dollar forecast.

EUR/USD Sentiment

- All eyes on ECB: The Eurozone continues to post weak inflation and low growth, and the markets are keeping a close eye on Thursday’s ECB policy meeting. There is a possibility that the ECB will reduce interest rates, something it hasn’t done since April. The argument against cutting interest rates is that with rates already at a record low of 0.50%, a cut of 0.25% might not have much impact. Other tools available to the ECB include a new LTRO or introducing a negative deposit rate.

- Mixed data out of Germany: Germany is the Eurozone’s largest economy, so German data has a strong impact on the Eurozone as well as the euro. This week’s data has been a mixed bag, making it difficult to predict in which direction the German economy is headed. Factory Orders jumped 3.3% in October, bouncing back from a decline of 0.3% in September. This was well above the estimate of 0.6%. However, Industrial Production failed to keep pace, posting a decline of 0.9%, compared to a strong 1.4% the month before. The estimate stood at 0.2%. We’ll get a look at Trade Balance on Friday.

- Eurozone inflation remains subdued: Inflation indicators in the Eurozone continue to point to very weak inflation, which in turn signals sluggish economic activity. Eurozone CPI dropped to 0.7% in October, its smallest gain in three years. Eurozone PPI posted a paltry gain of 0.1%, shy of the estimate of 0.3%. Germany, the region’s largest economy, is also producing inflation numbers well below the ECB’s inflation target of 2.0%. Speculation is growing that the ECB could cut interest rates in order to boost growth.

- US Services PMI improves: The first key release out of the US this week looked sharp. The ISM Non-Manufacturing PMI rose to 55.4 points in October, up from 54.4 the month before. This beat the estimate of 54.0 points. We’ll get a look at Unemployment Claims and Non-Farm Payrolls later in the week, and if these numbers are strong, there is sure to be talk of QE tapering in December, as the Fed has said on numerous occasions that the employment market must improve before QE tapering can occur.

- QE tapering unlikely before 2014: Last week’s Federal Reserve policy meeting was the first meeting since Congress hammered out an agreement on the debt ceiling and reopened the government. As expected, the Fed said that it would maintain QE at current levels of $85 billion each month. However, the policy statement was less dovish than expected, as the Fed said that the economy was expanding “at a moderate pace” and left the door open for tapering in December. However, most markets analysts are of the view that short of a sharp improvement in US data, QE tapering will be on hold until early 2014.