EUR/USD was hit hard on the British decision to leave the EU. This was certainly not priced in and many questions are left open. Will we see more falls? Apart from the Brexit fallout, we have elections in Spain,, inflation figures and more PMIs. Here is an outlook for the highlights of this week and an updated technical analysis for EUR/USD.

Contrary to the latest polls, Brits decided to leave the EU in a decisive 52% to 48% vote. The Brexit has implications not only on the UK economy and the collapsing pound, but also the euro-zone economies and the fate of the European Union. There are many uncertainties and scrambling continues. An economic slowdown or even a recession cannot be ruled out. Will the ECB provide more stimulus? President Draghi left the door open to the this before the referendum and we may hear more as events develop. Elsewhere, the German economy looks good with beats in the ZEW and IFO business sentiment measures. In the US, Yellen sounded quite dovish and figures were mixed, but the greenback enjoyed safe haven flows, second only to the yen.

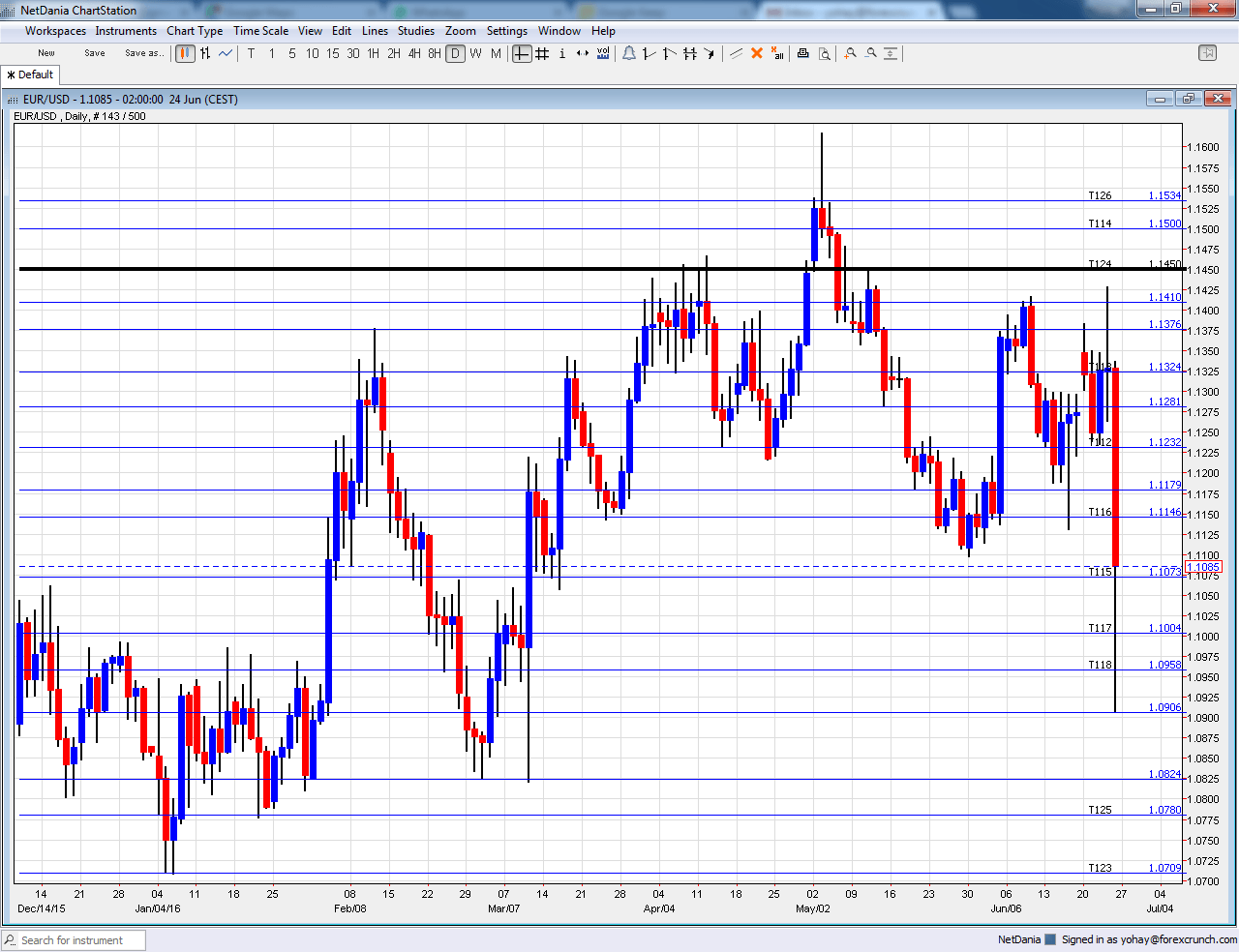

[do action=”autoupdate” tag=”EURUSDUpdate”/]EUR/USD daily chart with support and resistance lines on it. Click to enlarge:

- Elections in Spain: Sunday, exit polls at 18:00, full results expected after markets open. This is the second time Spaniards go to the polls in 6 months, after the previous elections yielded a hung parliament. The ruling center-right PP is expected to come out first once again, but well short of a majority. There is a good chance that the new left-wing Podemos will come out second, beating the center-left PSOE. Another new party, center-right Ciudadanos, is expected to maintain its fourth position. Another hung parliament is certainly a probability, but not the only one. The alliance of Podemos with a smaller radical left party, IU, could be advantageous, sending the united party to the first place. However, also in this scenario they would need the PSOE, and it is hard to see the veteran party play second fiddle to the new party. There is no love lost between the two. Another scenario is a German-style grand coalition led by the center-right PP, yet perhaps with a new leader. In any case, it is hard to see a decisive result and a new government emerging soon in the euro-zone’s fourth largest economy, a country which also suffers high unemployment.

- ECB Monetary data: Monday, 8:00. The ECB’s efforts to stimulate lending were somewhat successful with accelerated money supply and growth in private lending. However, the figures have been stuck in recent months. M3 Money Supply is expected to rise by 4.8% y/y after 4.6% beforehand. Loans are predicted to growth 1.6% after 1.5%.

- German Import Prices: Tuesday, 6:00. Prices of imported goods feed into consumer inflation. After a drop of 0.1%, a bounce back of 0.6% is expected for May in the zone’s largest economy.

- German GfK Consumer Climate: Wednesday, 6:00. This 2000 strong survey showed higher confidence in May with 9.8 points. The same score is expected now.

- German CPI: Wednesday during the morning, with the final figure at 12:00. Consumer prices rose 0.3% in May but this was probably a one off. A small advance of 0.1% is on the cards for June.

- Spanish CPI: Wednesday, 7:00. While Spain enjoys relatively high growth, it also suffers from deep deflation. Prices fell 1% y/y in May. The preliminary figure for June is expected to stand at -0.9%.

- German Retail Sales: Thursday, 8:00. Consumer spent less in April, with a disappointing drop of 0.9%. A rise is expected now: +0.6%.

- French CPI: Thursday, 6:45. Like Germany, also France saw a bump up in prices in May: 0.4%. And also here, a more moderate rise of 0.2% is predicted now.

- French Consumer Spending: Thursday, 6:45. Also in the second largest economy, consumers spent less. A drop of 0.1% was seen in April. Another such drop is on the cards now.

- German Unemployment Change: Thursday, 7:55. The number of unemployed dropped by 11K last time, in line with most months. Germany enjoys a robust labor market. A drop of 5K is on the cards now.

- CPI Flash Estimate: Thursday, 9:00. Despite publications from a few key countries, this publication can surprise. Headline inflation dropped by 0.1% in May and now, with higher oil prices, the y/y rate is expected to stand at a flat 0%. Core inflation is not expected to budge from 0.8% seen beforehand.

- ECB Meeting Minutes: Thursday, 11:30. The ECB releases minutes from its June meeting, when the ECB did not announce new measures but described the implementation of corporate bond buying and the new TLTROs. In that meeting, they also provided new forecasts which were not too optimistic. The minutes can show how worried members really are regarding their inflation mandate. It can also expose the internal debate. What could be more interesting is if we get details about the members’ view on the potential of Brexit.

- Manufacturing PMIs: Friday: Spain at 7:15, Italy at 7:45, the final French figure at 7:50, final German at 7:55 and all euro-zone at 8:00. In May, Spain’s manufacturing sector was growing slowly according to Markit, with 51.8 points. A rise to 52.1 points is expected now. Also Italy, the third largest economy, enjoyed growth with 52.4 points, above the 50 point threshold separating expansion from contraction. A score of 52.7 is expected now for June. According to the preliminary release for June, the French manufacturing sector remained in contraction with 47.9 points. Germany was growing with 54.5 and the whole euro-zone scored 52.6 points. These preliminary figures will likely be confirmed now.

- Unemployment Rate: Friday, 9:00. The unemployment rate is slowly sliding in the euro-area, with 10.2% in April. Another drop to 10.1% is on the cards now.

* All times are GMT

EUR/USD Technical Analysis

Euro/dollar started the week in range and found support at 1.1230 (mentioned last week). From there, it did managed to tackle resistance at 1.1410 but totally collapsed on the Brexit news, swing as low as 1.0905 before settling on higher ground on the erratic aftermath.

Technical lines from top to bottom:

1.1535 is a stepping stone as seen in May 2016 and also beforehand. It is followed by the very round level of 1.15.

1.1460 was a key resistance line in 2015 and 1000 above the multi-year lows. 1.1410 capped the pair in early June. 1.1375 worked as resistance in February and as support in May 2016.

1.1335 worked as the lower bound of a higher range and then capped recovery attempts in May. 1.1230 capped the pair after the fall in May and works as resistance.

1.1175 was the low point in the mid-May fall. 1.1140 cushioned the pair in October. 1.1070 served as a clear separator of ranges during February and also beforehand.

1.10 is a round number and significant resistance. 1.0905 is the swing low seen in June and serves as weak support. 1.0825 worked as support in early March 2015 and should also be watched. This is now a triple bottom.

The post-Draghi low 1.0780 replaces 1.08 as support. 1.0710 is the next support line on the chart after temporarily capping the pair in April 2015.

Further below, the 2016 low of 1.0520 and the 2015 low of 1.0460 provide further support.

I remain bearish on EUR/USD

Brexit is now reality and it is not good news. Even if we don’t hear about new stimulus from the ECB, the economic situation is likely to deteriorate. Further uncertainty from Spain could join the mix. Also in the US, the Fed is not likely to raise rates anytime soon. However, monetary policy divergence is maintained with the ECB continuing its QE program at full speed.

Our latest podcast is a Brexit Breakdown